Showing posts with label Global Housing Watch. Show all posts

Tuesday, December 4, 2018

Are Housing Price Cycles Asymmetric? Evidence from the US States and Metropolitan Areas

From a new paper by Christophe André, Rangan Gupta, and John Weirstrasd Muteba Mwamba:

“This paper investigates asymmetry in US housing price cycles at the state and metropolitan statistical area (MSA) level, using the Triples test (Randles et al., 1980). Several reasons may account for asymmetry in housing prices, including non-linearity in their determinants and in behavioural responses, in particular linked to equity constraints and loss aversion. However, few studies have formally tested the symmetry of housing price cycles. Evidence of asymmetry at the 5% confidence level is found in nearly half of the states, 37% of the MSAs and in the aggregate national series. Geographical patterns and comparisons with results obtained by Cook (2006) for the United Kingdom suggest that asymmetric cycles tend to prevail in areas where housing supply elasticity is low. In addition, asymmetric cycles with steep downturns are found in several states of the Midwest, where the decline in traditional industries has severely hit the economy. These results call for considering potential non-linearity when analysing, modelling and forecasting housing prices.”

From a new paper by Christophe André, Rangan Gupta, and John Weirstrasd Muteba Mwamba:

“This paper investigates asymmetry in US housing price cycles at the state and metropolitan statistical area (MSA) level, using the Triples test (Randles et al., 1980). Several reasons may account for asymmetry in housing prices, including non-linearity in their determinants and in behavioural responses, in particular linked to equity constraints and loss aversion. However, few studies have formally tested the symmetry of housing price cycles.

Posted by at 10:19 AM

Labels: Global Housing Watch

Friday, November 30, 2018

House Price Synchronicity, Banking Integration, and Global Financial Conditions

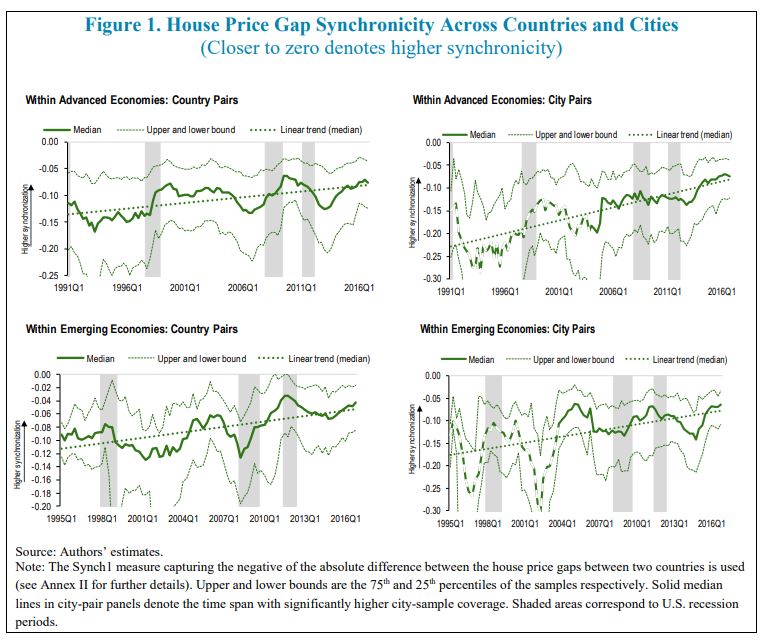

From a new IMF working paper by Adrian Alter, Jane Dokko, and Dulani Seneviratne:

“We examine the relationship between house price synchronicity and global financial conditions across 40 countries and about 70 cities over the past three decades. The role played by cross-border banking flows in residential property markets is examined as well. Looser global financial conditions are associated with greater house price synchronicity, even after controlling for bilateral financial integration. Moreover, we find that synchronicity across major cities may differ from that of their respective countries’, perhaps due to the influence of global investors on local house price dynamics. Policy choices such as macroprudential tools and exchange rate flexibility appear to be relevant for mitigating the sensitivity of domestic housing markets to the rest of the world.”

From a new IMF working paper by Adrian Alter, Jane Dokko, and Dulani Seneviratne:

“We examine the relationship between house price synchronicity and global financial conditions across 40 countries and about 70 cities over the past three decades. The role played by cross-border banking flows in residential property markets is examined as well. Looser global financial conditions are associated with greater house price synchronicity, even after controlling for bilateral financial integration.

Posted by at 4:13 PM

Labels: Global Housing Watch

Housing View – November 30, 2018

On cross-country:

- There is more to high house prices than constrained supply – Economist

- Pockets of risk in European housing markets – VoxEU

- The real cost of international real estate – Savills

- Rising residential costs help push Hong Kong to the top of the Savills Live/Work Index – Savills

On the US:

- Drivers of the Great Housing Boom-Bust: Credit Conditions, Beliefs, or Both? – NBER

- What The 1990s Tell Us About The Next Housing Bust – Real Estate Decoded

- Ruling mostly clears plan to upzone Seattle neighborhoods for affordable housing – Seattle Times

- A tax break to hasten gentrification? Housing market’s Opportunity Zones may miss their target – Market Watch

- US: Signs of a slowdown? – ING

- Ahead of Amazon’s move to Queens, could buying an apartment count as insider trading? – Quartz

- 81 Percent of Homes in the San Francisco Metro Area Are Worth More Than $1 Million. That’s Not Normal. – Reason

- The U.S. Housing Boom Is Coming to an End, Starting in Dallas – Wall Street Journal

- What Accounts for Recent Growth in Homeowner Households? – Harvard Joint Center for Housing Studies

- 6 ways Washington could make housing more affordable – Politico

- Why a housing project is building hope for the US working poor – Financial Times

- Rent Control Is Making a Comeback. But Is That a Good Idea? – The Pew Charitable Trusts

- House prices have surged, and so will the government’s mortgage obligations – Market Watch

- Why 2019 won’t lead to a home buyer’s market – Market Watch

- Black Homeowners Saw Greater Home Price Appreciation Than Whites in Some Areas – CityLab

- Secret luxury homes: how the ultra-rich hide their properties – Financial Times

On other countries:

- [Australia] Securitisation and the Housing Market – Reserve Bank of Australia

- [Australia] Why Australia may not be the next “big short” – MacroBusiness

- [China] China’s Real Estate Market – NBER

- [Ireland] Why are job numbers soaring despite the housing crisis? – The Irish Times

- [New Zealand] NZ cenbank to ease mortgage curbs but lift bank capital norms – Reuters

- [Puerto Rico] Generadores de 3700 dólares y lavabos de 666 dólares: los sobreprecios de las reparaciones en Puerto Rico – New York Times

- [Singapore] Financial Stability Review 2018 – Monetary Authority of Singapore

- [Sweden] Financial Stability Report 2018:02 – Sveriges Riksbank

- [Sweden] Swedish housing market starting to crumble – Variant Perception

- [United Kingdom] The case for scrapping stamp duty – Economist

- [United Kingdom] Lending relationships and the collateral channel – Bank of England

- [United Kingdom] Brexit effect ‘limited’ on UK house prices – Financial Times

- [United Kingdom] BOE Warns Disorderly Brexit May Halve Commercial-Property Prices – Bloomberg

Photo by Aliis Sinisalu

On cross-country:

- There is more to high house prices than constrained supply – Economist

- Pockets of risk in European housing markets – VoxEU

- The real cost of international real estate – Savills

- Rising residential costs help push Hong Kong to the top of the Savills Live/Work Index – Savills

On the US:

- Drivers of the Great Housing Boom-Bust: Credit Conditions,

Posted by at 5:00 AM

Labels: Global Housing Watch

Tuesday, November 27, 2018

A Look Back At the Housing Stories of 2018

Below is a brief recap of the topics that the Global Housing Watch newsletter covered this year:

— Specific topics: affordable housing; housing policy; house prices and homeownership; surge in second home investments; understanding behavior of homebuyers; and urban revitalization.

— Summary of conferences and workshops: commercial and house price measurement; housing affordability; infrastructure and real estate; Housing, Household Debt and Policy; Housing, Urban Development, and the Macroeconomy; and Housing and Macroeconomics.

— Reading suggestions: summer reading list.

— Experts views on specific countries and regions: Africa, Latin America, Singapore, and United Kingdom.

— IMF assessments of housing markets. Regions: advanced economies, Europe, and cities. Countries: Australia, Austria, Belgium, Canada, Chile, China, Colombia, Czech Republic, Denmark, Estonia, Germany, Georgia, Hong Kong, Hungary, Iceland, Indonesia, Ireland, Israel, Korea, Latvia, Lithuania, Luxembourg, Malaysia, Malta, Mongolia, Namibia, Netherlands, New Zealand, Norway, Peru, Philippines, Portugal, Qatar, Romania, Singapore, Slovak Republic, Spain, Sri Lanka, Switzerland, Thailand, Tonga, United Kingdom, United States, and Vietnam.

Below is a brief recap of the topics that the Global Housing Watch newsletter covered this year:

— Specific topics: affordable housing; housing policy; house prices and homeownership; surge in second home investments; understanding behavior of homebuyers; and urban revitalization.

— Summary of conferences and workshops: commercial and house price measurement; housing affordability;

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts