Tuesday, July 31, 2018

Housing Market in Singapore

The IMF’s latest report on Singapore says that:

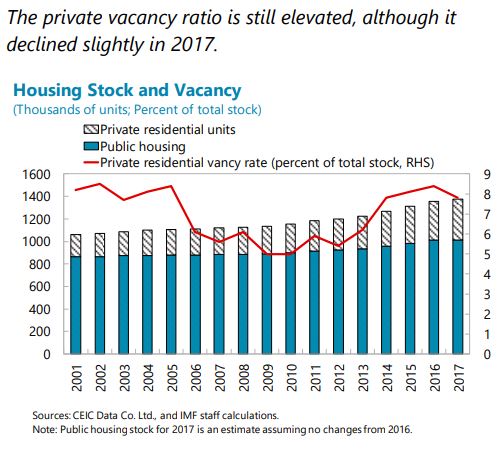

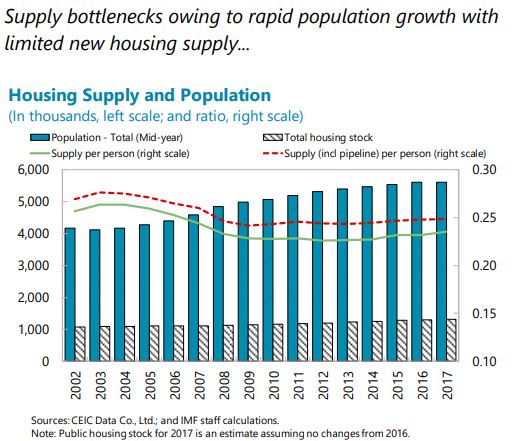

“In the housing market, prices of private residential properties staged a steady recovery in 2017, for the first time since 2013, and were up by 5.4 percent y/y in 2018Q1. The share of foreign transactions has remained stable over the past six years (close to 7 percent) but is significantly below the 2011 peak (19.5 percent). Vacancy rates have come down slightly but

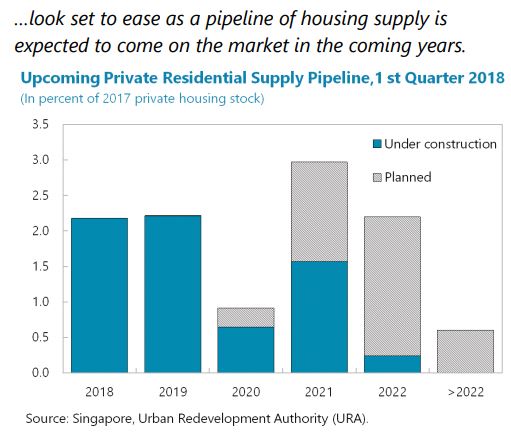

are still elevated. In recent quarters, supply in the pipeline (i.e., new and redevelopment projects of private residential units with planning approvals that are expected to be on the market within a few years) has also increased after a few years of falling.”

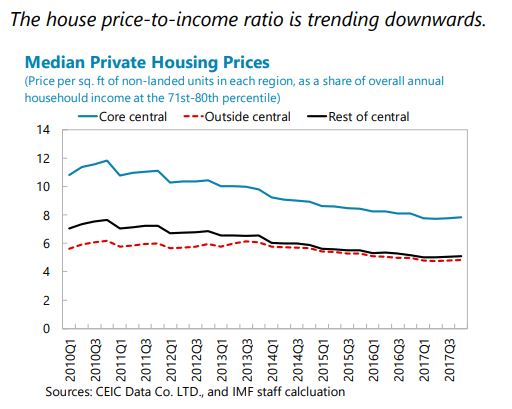

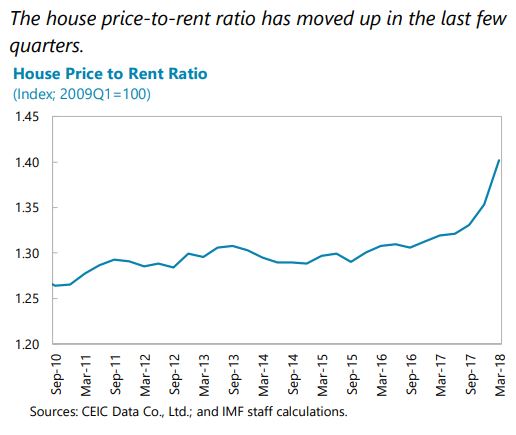

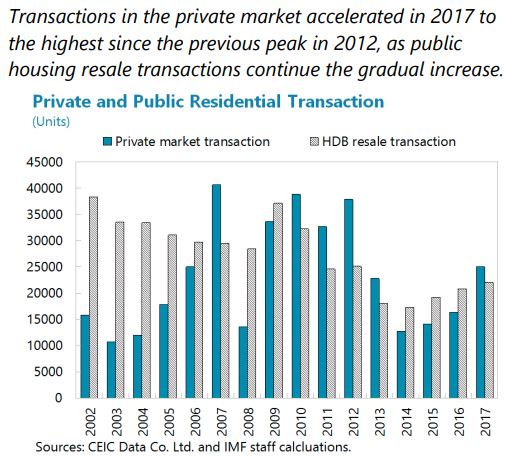

Singapore’s property market policies are comprehensive, aiming to manage demand and supply with active monitoring and periodic adjustments. Staff’s empirical analysis suggests that the prices of private housing in Singapore are affected by a host of factors, including incomes, rents and interest rates, and by supply and cost determinants. Moreover, while housing prices in major Asian cities are increasingly synchronized, Singapore’s property prices appear to have decoupled and are now relatively attractive to international investors (…). Singapore’s comprehensive set of property market cooling measures, including Additional Buyer’s Stamp Duty (ABSD) and limits on Total Debt Servicing Ratio (TDSR) and Loan to Value (LTV) caps, have been critical to stabilizing the property market. Property prices picked up in the last three quarters and are expected to increase further in the near term. Staff analysis also suggests that prices are now moderately above levels consistent with long-term fundamentals. Higher private property prices have been accompanied by increased transaction volumes amid a stronger economy, improved market sentiments, and the recent increase in collective sales for redevelopment projects. The Seller’s Stamp Duty was relaxed in March 2017. In the 2018 Budget, the Buyer’s Stamp Duty was raised by one percentage point for residential properties valued over S$1 million, justified by the need to make property

taxation more progressive.Against this background, staff’s views on property market measures are as follows:

- On the demand side, property market cooling measures should be maintained, including structural macroprudential policies (TDSR and LTV caps) and cyclical measures, such as ABSD, given the elevated financial risks. However, ABSD is a residency-based capital flow management/macro-prudential measure, and staff recommends eliminating residency-based differentiation by unifying rates (lowering rates charged foreigners to the level charged Singaporeans and foreign residents), and then phasing out the measure once systemic risks from the housing market dissipate.

- On the supply side, housing supply in the pipeline has continued to rise in 2018Q1. A large part of those will be on the market for sale in later this year or the next year, adding significant new supplies of housing stock. Staff encourages the authorities to continue to monitor the supply side to ensure that sufficient land is reserved and released in a timely manner through the government land sales program. In addition, other supply-side measures such as the process of building approval could be targeted to meet housing demand.”

Posted by at 10:01 AM

Labels: Global Housing Watch

Subscribe to: Posts