Sunday, February 25, 2018

The UK’s Housing Problem…

Global Housing Watch Newsletter: February 2018

This post is written by David Miles. He is a Professor of Financial Economics at Imperial College Business School. Please bear in mind that these are the views of Professor Miles, and should not be attributed to the IMF.

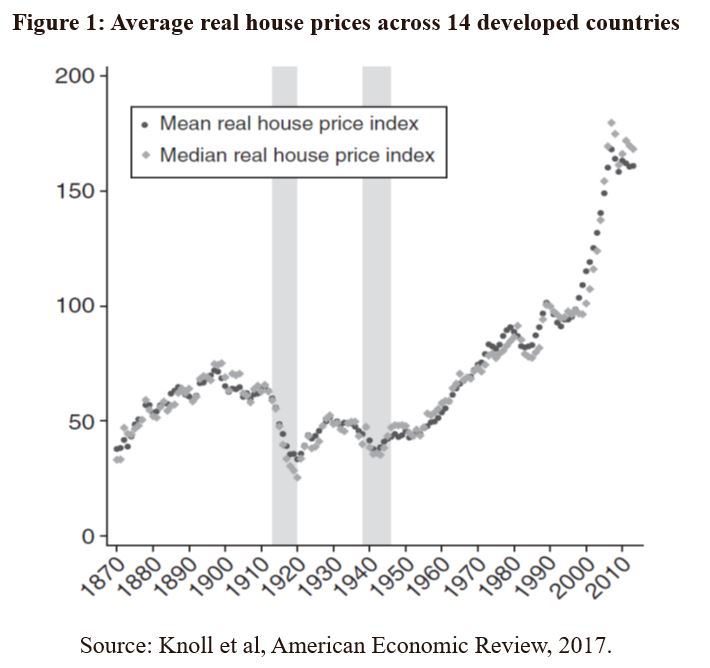

Average house prices in the UK have risen dramatically faster than average incomes over the past 30 years. Relative to average disposable incomes houses are almost three times as expensive now as they were in the mid-1980s. But this is not something specific to the UK and neither is it uniform across the UK. Recent evidence on house prices across a large sample of developed economies back to the mid nineteenth century reveals two things[1]. First, that on average house prices moved roughly in line with the price of other things between about 1870 and 1970 in most countries; and second that over the past fifty years house prices have – again on average across developed countries – roughly tripled relative to the price of other things (see figure 1 below).

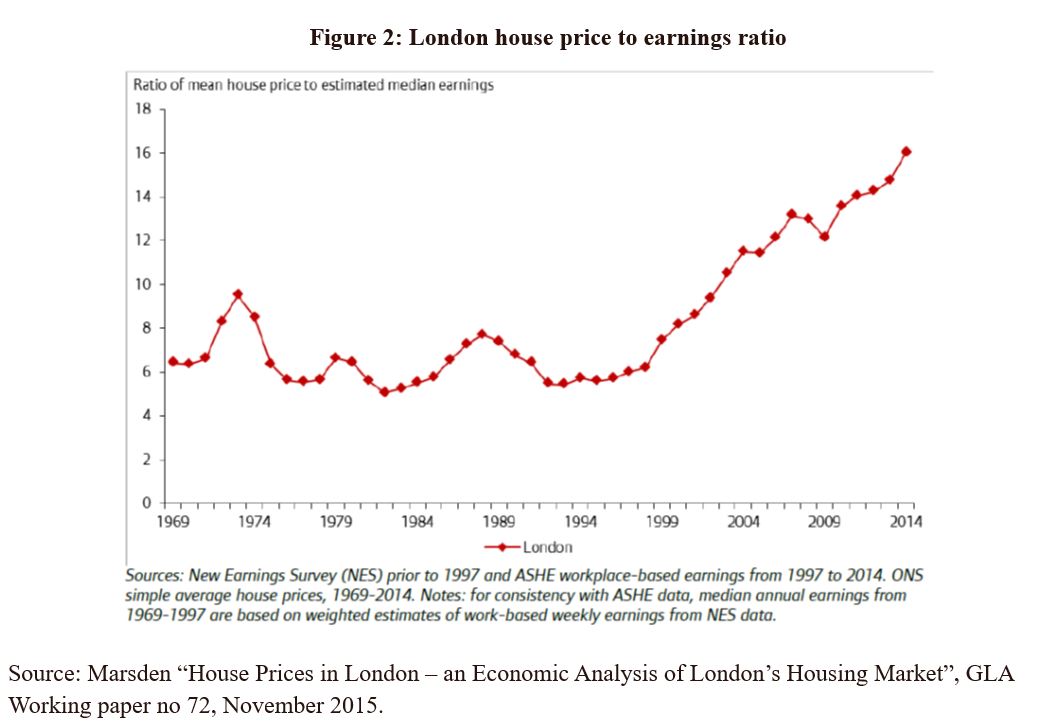

So there is nothing unique about the fact that in the UK house prices have in recent decades risen very much faster than the price of most other things and that houses have become dramatically much more expensive than cars, food, clothes, electrical goods, energy and travel. And the degree to which that has happened is very different across the UK. In London – the centre of the most densely populated South-East corner of the country – average house prices have risen far faster than in most other parts of the country (figure 2).

Why has this happened? We can start by dismissing one theory – which is that the rising cost of constructing houses has driven up prices. In fact, the cost of building houses can account for only a tiny part of the huge rise in the relative price of houses. Increases in the price of land on which houses can be built, in contrast, have risen enormously and account for most of the increase in the value of houses. But “account for” does not mean “explain” – one has not explained why house values have risen so fast by noting the enormous increase in the price of land on which houses can be built in the places where people want to live. You just push the question back to why land values have risen so much.

Part of that answer is connected to panning restrictions – and some people are satisfied to leave that as the answer. But those restrictions are not just arbitrary and they do reflect real effects upon quality of life or more building in already densely populated parts of a country. Such restrictions exist in most countries and are typically most binding in parts of countries where population densities and house prices are high. This suggests that more fundamental forces are at work than just the much-quoted inefficiencies of arbitrary UK planning rules.

In recent work with James Sefton I have tried to assess the extent to which these more fundamental forces might account for the relentless upward movements in house prices[2]. Our focus is on the long run. We consider the housing sector within a model of the overall economy that aims to explain overall economic growth, saving and asset prices. Any long run analysis has to model the changing supply of housing taking into account the fixity of land mass and the way in which shifts in the cost of land relative to structures changes the way in which houses are constructed. Land is obviously not homogenous and the impact of the most important way in which it differs (that is by location) varies over time as technological change means that distance may have a varying effect on value. One obvious way in which this happens is if transportation costs change.

We find that there is great sensitivity over time in the pattern of development, the types of houses built and the values of structures to even small changes in two key parameters: the degree of substitutability of land and structure in creating houses; the degree to which households substitute between housing and non-housing goods. But the great sensitivity of the equilibrium (or fundamental) housing cost trajectory to small changes in these two key elasticities means it is hard to know whether house prices relative to incomes rising to levels not seen before is the start of a bubble or just the natural path we should expect in an economy with a rising population, growing incomes and with a population density higher than in the past. Using a simple metric like the house price to income ratio relative to its history is unlikely to be a very reliable guide to whether prices are out of line with fundamentals. Having a system of rules (e.g. on acceptable loan to value ratios for mortgages) that would tend to bind ever tighter as house price to income ratios rise will be problematic if the fundamental equilibrium is that this ratio should be rising for many decades.

We find that it is not difficult to find sets of assumptions about elasticities which are plausible in the light of existing evidence and which imply that house prices can rise faster than incomes for periods spanning generations. This has nothing to do with planning restrictions.

Ultimately housing over the long term could become increasingly expensive and perhaps increasingly rented. That would be more likely if:

A. population and productivity both grow steadily

B. people are increasingly unwilling to live high in the sky or even underground, which will limit the scope to economise on land use.

C. people do not substitute much away from spending money on houses and divert it to other consumption as house prices rise.

D. there is no improvement in transport infrastructure and travel times. That would limit how far from the most densely populated and popular urban centres people can live.

These four conditions probably all hold in the UK. That sounds like bad news. But major investment in transport infrastructure that reduce commuting times could mean future house price rises can still be limited.

[1]Katharina Knoll, Moritz Schularick, and Thomas Steger. No price like home: global house prices, 1870.2012. The American Economic Review, 107(2):331.353, 2017.

[2] “Houses Across Time and Space”, David Miles and James Sefton, CEPR Discussion 12103.

Posted by at 7:30 PM

Labels: Global Housing Watch

Subscribe to: Posts