Monday, January 31, 2022

Creative destruction during crises: An opportunity for a cleaner energy mix

Published on Voxeu.org by Pragyan Deb, Davide Furceri, Jonathan D. Ostry, Nour Tawk on 31 January 2022.

“Lockdowns resulting from the COVID-19 pandemic reduced overall energy demand in 2020. However, electricity generation from renewable sources was surprisingly resilient and, as a result, the share of renewables in electricity demand increased in many regions (International Energy Agency 2020). What remains an open question is whether recessions of themselves tend to spur investments in more efficient, greener, energy sources, or instead to continue investing in old coal-based plants. On one hand, the disruption in financing engendered by the crisis may reduce innovation through lower research and development, which is highly procyclical (De Haas et al. 2021). On the other, lower energy demand and associated plant closures brought about by the recession may provide energy producers with an opportunity to improve their efficiency by replacing older environmentally unfriendly plants with renewable sources of energy when demand recovers. The idea that outdated units are destroyed and replaced by newer technological innovations goes back to Joseph A. Schumpeter’s thesis on ‘creative destruction’ (Schumpeter 1939, 1942), with economic disruptions such as the one brought about by the pandemic acting as a time of cleansing (Caballero and Hammour 1994).”

Read more by clicking here.

Published on Voxeu.org by Pragyan Deb, Davide Furceri, Jonathan D. Ostry, Nour Tawk on 31 January 2022.

“Lockdowns resulting from the COVID-19 pandemic reduced overall energy demand in 2020. However, electricity generation from renewable sources was surprisingly resilient and, as a result, the share of renewables in electricity demand increased in many regions (International Energy Agency 2020). What remains an open question is whether recessions of themselves tend to spur investments in more efficient,

Posted by at 2:25 PM

Labels: Energy & Climate Change

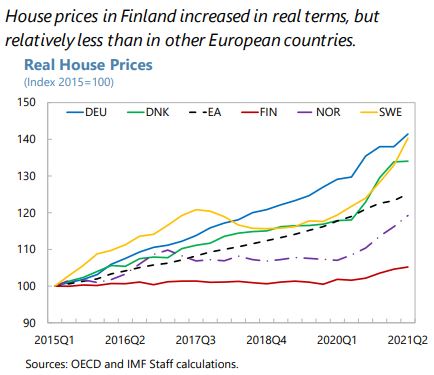

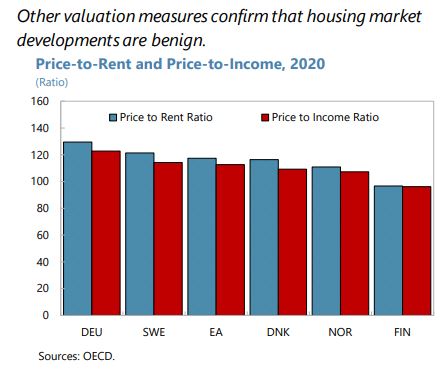

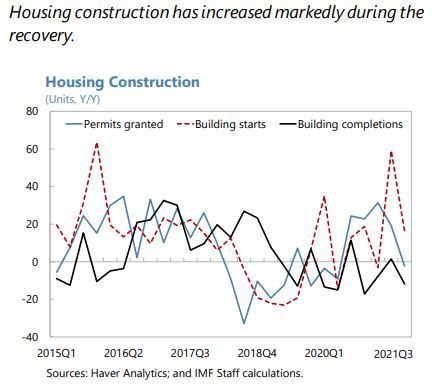

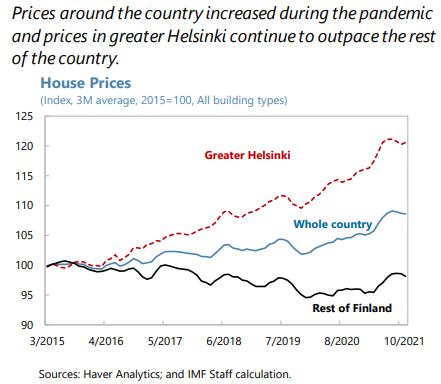

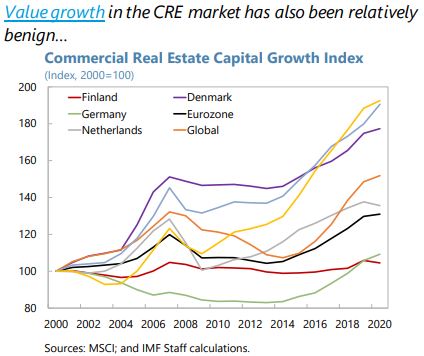

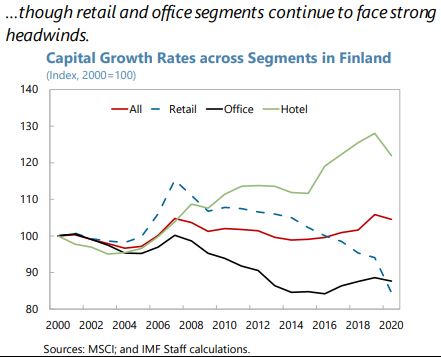

Housing Market in Finland

From the IMF’s latest report on Finland:

“The increase and changing composition of household debt continues to pose borrower-side vulnerabilities. Pre-pandemic, real estate prices were not overvalued, but household debt was increasing (although still low relative to Nordic peers). Much of this new debt was in the form of housing company loans—loans that finance buying shares of a housing company that may be connected to a specific apartment instead of purchasing it directly—which mask risk exposures for households. Unsecured consumer credit was also on the rise. As the pandemic struck, the authorities relaxed loan-to-collateral (LTC) requirements for housing loans. This was accompanied by an increase in highly leveraged borrowing, and housing valuations rose throughout Finland. Housing price growth has begun to moderate somewhat in the second half of 2021.

(…)

The authorities are taking steps to mitigate vulnerabilities in household finances. Following the recent increase in highly leveraged mortgage borrowing, the authorities tightened the LTC limit to pre-pandemic levels. Parliament will discuss in the spring of 2022 a draft bill on borrower-based macroprudential tools including maturity limits for housing and housing company loans, and loan-to-value (LTV) limits for housing company loans (a debt-to-income (DTI) cap was removed from the draft bill due to strong industry and political opposition). Additionally, an electronic registry of housing company shares should be operational by end-2022, making it easier to assess risks of investing in housing companies. But implementation of the planned comprehensive credit registry has been delayed to 2024 due to technical constraints.

Staff recommend that more steps be taken to enhance the macroprudential toolkit and strengthen macrofinancial resilience. The macroprudential toolkit could be enhanced further to include: (i) a DTI cap in line with recommendations from the government-appointed working group and reflecting growing household debt vulnerabilities; and (ii) supplementing the DTI cap with a debt-service-to-income cap once the new comprehensive credit registry is operational. Features of the tax code that create incentives for investors to favor housing company loans should be addressed so as to mitigate compositional changes in household debt (the recent MOF review concluded that separating the treatment of housing company shareholders’ loans’ amortization costs from interest and other expenses could help balance incentives). In this context, data relating to consumer credit and housing companies should be improved.”

From the IMF’s latest report on Finland:

“The increase and changing composition of household debt continues to pose borrower-side vulnerabilities. Pre-pandemic, real estate prices were not overvalued, but household debt was increasing (although still low relative to Nordic peers). Much of this new debt was in the form of housing company loans—loans that finance buying shares of a housing company that may be connected to a specific apartment instead of purchasing it directly—which mask risk exposures for households.

Posted by at 12:16 PM

Labels: Global Housing Watch

Economic inequality in Germany: A long-run view

The ongoing Covid-19 crisis, which is likely to exacerbate economic inequality within countries in the West and probably among countries worldwide (Furceri, Loungani, Ostry, Pizzuto, 2021), has reinstated the need for a thorough investigation into the causes and consequences of inequality. In a recent column for VoxEU CEPR, economists Guido Alfani, Victoria Gierok, and Felix Schaff discuss inequality in the context of Germany over the years.

This column reconstructs wealth inequality in Germany over five centuries and demonstrates potential leveling effects of catastrophes with the help of evidence from events like the Black Death and the Thirty Years’ War. They conclude with insights like the fact that inequality falls in the aftermath of epidemics only in the presence of extremely high mortality rates.

Click here to read more.

The ongoing Covid-19 crisis, which is likely to exacerbate economic inequality within countries in the West and probably among countries worldwide (Furceri, Loungani, Ostry, Pizzuto, 2021), has reinstated the need for a thorough investigation into the causes and consequences of inequality. In a recent column for VoxEU CEPR, economists Guido Alfani, Victoria Gierok, and Felix Schaff discuss inequality in the context of Germany over the years.

This column reconstructs wealth inequality in Germany over five centuries and demonstrates potential leveling effects of catastrophes with the help of evidence from events like the Black Death and the Thirty Years’

Posted by at 10:35 AM

Labels: Inclusive Growth

Sunday, January 30, 2022

Interest-rate surveys

New article by John Cochrane from John Cochrane’s blog.

“Torsten Slok, chief economist at Apollo Global Management, passes along the above gorgeous graph. Fed forecasts of interest rates behave similarly. So does the “market forecast” embedded in the yield curve, which usually slopes upward.

Torsten’s conclusion:

The forecasting track record of the economics profession when it comes to 10-year interest rates is not particularly impressive, see chart [above]. Since the Philadelphia Fed started their Survey of Professional Forecasters twenty years ago, the economists and strategists participating have been systematically wrong, predicting that long rates would move higher. Their latest release has the same prediction.

Well. Like the famous broken clock that is right twice a day, note the forecasts are “right” in times of higher rates. So don’t necessarily run out and buy bonds today.

Can it possibly be true that professional forecasters are simply behaviorally dumb, refuse to learn, and the institutions that hire them refuse to hire more rational ones?”

To read more click here.

New article by John Cochrane from John Cochrane’s blog.

“Torsten Slok, chief economist at Apollo Global Management, passes along the above gorgeous graph. Fed forecasts of interest rates behave similarly. So does the “market forecast” embedded in the yield curve, which usually slopes upward.

Torsten’s conclusion:

The forecasting track record of the economics profession when it comes to 10-year interest rates is not particularly impressive, see chart [above].

Posted by at 10:56 AM

Labels: Forecasting Forum

Gravity at 60: A celebration of the workhorse model of trade

From a VoxEU post by Yoto Yotov:

“This year marks the 60th anniversary of the workhorse model of trade – the gravity equation. This column celebrates the anniversary by addressing some misconceptions about gravity and by tracing its evolution from an intuitive a-theoretical application to an estimating computable general equilibrium model that can be nested in more complex frameworks.

This year marks the 60th anniversary of the workhorse model of trade – the gravity equation (Tinbergen1962). Gravity is a ‘celebrity’ among economic models; it has been applied and extended in thousands of papers by trade economists, colleagues from other fields, and policy practitioners. Moreover, as noted by the brilliant late Peter Neary, the gravity equation is probably the only econometric model that has been featured on the front page of the Financial Times (on 19 April 2016).

Unfortunately, and as sometimes happens to celebrities, the gravity model is misspecified (misunderstood) by the press. More worrisome, we often see gravity applications in academic papers and policy reports that are not consistent with theory and/or do not take into account major developments in the empirical gravity literature. As a result, the estimates in such papers could be severely biased and their policy recommendations could be misleading. Moreover, while it is well understood that trade theory and trade-policy analysis should be set in general equilibrium (GE), there is still a division and scepticism among academics and trade-policy practitioners about the usefulness of the gravity as a Computable GE (CGE) framework for counterfactual projections. A prominent example, which motivated the inclusion of the gravity equation in the Financial Times, is the debate among UK economists over gravity-based projections of the Brexit effects.

To celebrate gravity’s anniversary and address some misconceptions about the gravity model, in a new paper (Yotov 2022) I trace its evolution, as depicted in Figure 1, from a naive application to an ‘estimating CGE’ (E-CGE) model that can be nested in more complex frameworks.”

Continue reading here.

From a VoxEU post by Yoto Yotov:

“This year marks the 60th anniversary of the workhorse model of trade – the gravity equation. This column celebrates the anniversary by addressing some misconceptions about gravity and by tracing its evolution from an intuitive a-theoretical application to an estimating computable general equilibrium model that can be nested in more complex frameworks.

This year marks the 60th anniversary of the workhorse model of trade – the gravity equation (Tinbergen1962).

Posted by at 8:27 AM

Labels: Macro Demystified

Subscribe to: Posts