Wednesday, March 30, 2016

Marja C Hoek-Smit on Housing Markets in Developing and Emerging Countries

In the interview below, Marja C Hoek-Smit—Director of the International Housing Finance Program at the Wharton School and Director of HOFINET—the Housing Finance Information Portal—talks about her work, about housing markets in emerging and developing economies, and about some of the challenges, and success stories. In doing so, she provides a global picture of the housing market in emerging and developing economies—a region where much remains to be known.

Hites Ahir: Please tell us about your work.

Marja C Hoek-Smit: The broad focus of my work is first on improving the efficiency and reach of urban housing markets in developing and emerging market countries, both real-side markets and housing finance markets. Second, an increasingly important part of what I do is to find the best way to subsidize those who cannot afford to pay for available housing or need a subsidy to access housing finance. In many emerging market countries 60 to 75 percent of the urban population cannot access formal housing markets for a variety of reasons.

Housing is important from an economic, social and political perspective, and, in countries with substantial mortgage markets, the housing sector is critical from a financial stability perspective. Yet, housing has for the past decades not received the attention it deserves, and housing conditions in some developing countries have deteriorated despite economic growth. International agencies have mostly focused on upgrading slum areas. Poor housing is too often just seen as a poverty or low-income problem relative to “unavoidable” house-price trends, a perception that leads to very blunt policies for the improvement of housing conditions, in particular in the type of subsidies applied to housing. For example, in many countries subsidizing interest rates on mortgage loans provided through state housing finance institutions, remains the preferred way to address the “affordability” problem, even though such subsidies are known to be unnecessarily costly, limit the expansion of the private housing finance system and are inequitable. Reasons for high and increasing house-prices are often not analyzed in any detail, nor are reasons for housing finance markets to remain small and mortgage interest rates high relative to the risk-free rate. Yet answers to these questions are critical in the design of the right policy instruments aimed at making these systems more efficient.

Housing markets are complex and depend on well-functioning finance- and land-markets, and on facilitative legal and regulatory systems and administrative procedures in these supply markets. The analysis of housing markets therefore requires many different types of skills. In many countries housing policy is still seen as the domain of planners and architects, and it is difficult to incorporate economic and financial sector aspects of housing in policy analysis.

My consulting work is focused on assisting governments in bringing the different strands of housing market analysis together- on the demand and supply side- and in developing comprehensive housing policies for different segments of the housing market. For the broad middle income market that means addressing the constraints facing private developers in supplying housing for this population segment, and working with the financial sector to assist the expansion of mortgage markets. Relatively small demand-side subsidies may be needed to improve access for households at the margin. For the market segment where low-incomes and poverty make it impossible for market actors to deliver housing, support needs to be much more comprehensive and may focus primarily on the supply of rental housing or alternative home-ownership strategies.

The second pillar of my work is education. My academic and executive teaching is similarly focused on the housing sector in this broader context. Jointly with my colleagues from the Wharton School, I established an executive education program with a focus on housing markets, and housing finance sector analysis, and the related public policies, for senior public and private sector professionals from developing and emerging market countries. The International Housing Finance Program (IHFP) of the Wharton Zell/Lurie Real Estate Center has consistently offered courses both at Wharton and in emerging market countries over the past 30 years and has developed a joint housing finance program for Sub-Saharan African countries with Cape Town University.

More recently a third component has been added to this mix, the development of global data systems for the housing finance sector. Because of the dearth of comparable data on housing markets and housing finance systems globally, the IHFP established a standardized and longitudinal data collection effort – the Housing Finance Information Network. We research and work with many countries’ housing finance institutions to collect such data for more than 140 countries and make it available on a public web-portal — HOFINET. http://hofinet.org

Hites Ahir: What are the key problems and challenges that the housing sector faces in emerging market economies?

Marja C Hoek-Smit: On the demand side, low incomes relative to house prices, the informality of incomes (often as high as 60 percent of the labor force), high inequality (increased over the past years particularly in Sub-Saharan Africa and SE Asia), high indebtedness, and related low propensity to save, are major constraints on the demand side, exacerbated by a lack of access to finance.

On the supply-side, constraints in real-supply-systems are frequently a more difficult problem to solve and lead to high prices relative to construction costs. Rapid urbanization at increasingly lower levels of per capita income strain governments’ capacity to provide services and infrastructure, including transportation systems, for formal housing expansion, increasing land scarcity. Unrealistically high standards and zoning/planning restrictions, as well as inefficiencies of the permitting process drive up housing costs and make it impossible for developers to cater to lower middle, and middle income groups.

Difficulties in safely expanding housing finance systems, are often a more binding constraint on the supply-side and include: i) poor systems to understand and deal with credit risk, ii) high transaction costs associated with lower-income and non-salaried customers, iii) stress on funding sources, iv) lack of mechanisms to deal with asset-liability mismatches when capital market funding is limited, and, iv) in some emerging market economies, the dominance of government housing finance systems benefitting from implicit subsidies and the related reluctance of private lenders to enter the market, ultimately limiting the overall scale of mortgage availability. In addition, Basel III regulations and solvency and liquidity requirements make it more difficult for the banking sector to expand longer term mortgage lending and the banking sector is the core provider of mortgage loans in most emerging market countries.

Hites Ahir: Which regions face the biggest challenges and why?

Marja C Hoek-Smit: Low-income countries that are urbanizing rapidly, starting from a low urban base, face the most complex urban housing problems, i.e., countries in Sub-Sahara Africa, and South and SE Asia. On the other end of the spectrum are the highly urbanized middle income countries of Latin America with dominant state supported and subsidized housing finance systems, such as Mexico and Brazil, which have created policy-induced volatility in the housing- and construction markets and stress in the housing finance systems. While these policies were successful in addressing high income inequality, they created locational inequalities and housing risks for households and government. Mexico has started a process of comprehensive policy reform both on the real-supply side and in the housing finance system.

Hites Ahir: What are some of the successful approaches to expand affordable housing?

Marja C Hoek-Smit: From the above discussion it follows that there is not one right approach or set of policies that address the housing affordability problems across emerging market countries and that policies must differ according to the specific demand and supply constraints in each market. In general, countries that have invested in a comprehensive housing market analysis, differentiated by type of urban area, and have put in place a medium/long-term agenda for reforms of land-policies, and land registration systems, planning regulations, housing finance sector and subsidy policies, have done better compared to countries with similar demographics and income levels that have not addressed these issues. Several countries are in the process of implementing such comprehensive approach to housing reforms, e.g., Mexico, South Africa, Egypt, India, and, although in an early phase, Indonesia. I focus here on two countries that have gone through such reforms in the past.

Thailand is a country that reformed its housing finance system and its urban development policies in the 1980s and 1990s, and was able to gradually expand the formal supply of middle and lower-middle income housing with minimum subsides. Community-based upgrading and resettlement policies were effective in further decreasing its sizable urban slum population by the early 2000s. Political instability and budget cuts for housing during the recent decade, however, are serving to jeopardize these achievements.

Chile is a country that has implemented a successful housing sector reform program that has been fine-tuned over many years. Like Thailand, it reformed its government housing finance system in the 1980s. It introduced demand-side subsidies linked to market-rate loans for the middle income segment. Its private housing finance system expanded and so did the private housing market. Gradually, Chile was able to decrease the proportion of the population that cannot access market provided housing, but with increasing subsidy levels. It adjusted its approach to support housing for the lowest-income group many times, and, currently, supports the supply of housing for the poor with very high supply-side subsidies channeled through NGOs. The recent economic down-turn has put pressure on the subsidy budget, however. This cloud may have a silver lining. It may entice Chile’s housing ministry to analyze whether its liberal housing subsidy system may in fact have price effects that it should address.

Outstanding issues in both countries are the lack of development of a private rental sector.

From the Global Housing Watch Newsletter: March 2016

In the interview below, Marja C Hoek-Smit—Director of the International Housing Finance Program at the Wharton School and Director of HOFINET—the Housing Finance Information Portal—talks about her work, about housing markets in emerging and developing economies, and about some of the challenges, and success stories. In doing so, she provides a global picture of the housing market in emerging and developing economies—a region where much remains to be known.

Posted by at 9:00 AM

Labels: Global Housing Watch

Thursday, March 24, 2016

Oil Prices and the Global Economy: It’s Complicated

Oil prices have been persistently low for well over a year and a half now, but as the April 2016 World Economic Outlook will document, the widely anticipated “shot in the arm” for the global economy has yet to materialize. We argue that, paradoxically, global benefits from low prices will likely appear only after prices have recovered somewhat, and advanced economies have made more progress surmounting the current low interest rate environment.

Since June 2014 oil prices have dropped about 65 percent in U.S. dollar terms (about $70) as growth has progressively slowed across a broad range of countries. Even taking into account the 20 percent dollar appreciation during this period (in nominal effective terms), the decline in oil prices in local currency has been on average over $60. This outcome has puzzled many observers including us at the Fund, who had believed that oil-price declines would be a net plus for the world economy, obviously hurting exporters but delivering more-than-offsetting gains to importers. The key assumption behind that belief is a specific difference in saving behavior between oil importers and oil exporters: consumers in oil importing regions such as Europe have a higher marginal propensity to consume out of income than those in exporters such as Saudi Arabia.

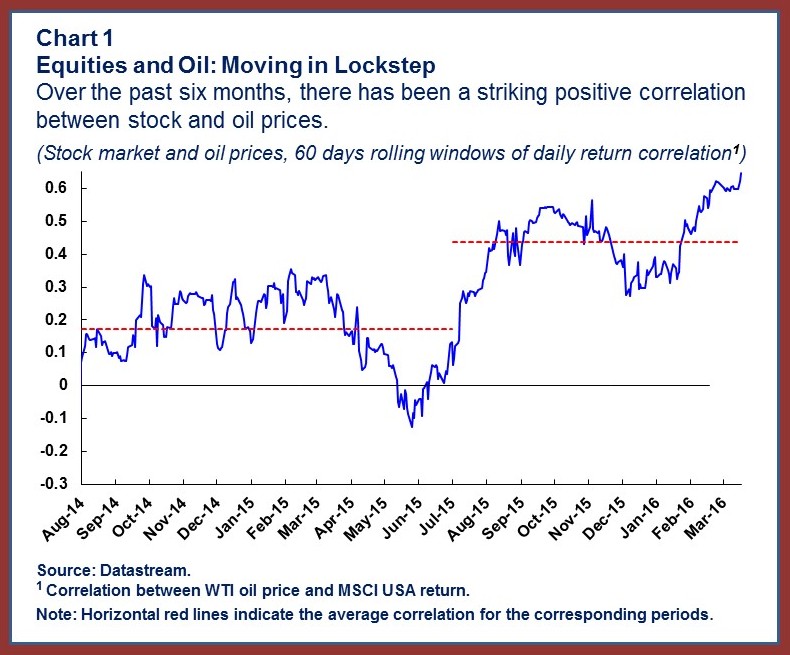

World equity markets have clearly not subscribed to this theory. Over the past six months or more, equity markets have tended to fall when oil prices fall—not what we would expect if lower oil prices help the world economy on balance. Indeed, since August 2015 the simple correlation between equity and oil prices has not only been positive (Chart 1), it has doubled in comparison to an earlier period starting in August 2014 (though not to an unprecedented level).

Past episodes of sharp changes in oil prices have tended to have visible countercyclical effects—for example, slower world growth after big increases. Is this time different? Several factors affect the relation between oil prices and growth, but we will argue that a big difference from previous episodes is that many advanced economies have nominal interest rates at or near zero.

Supply versus demand

One obvious problem in predicting the effects of oil-price movements is that a fall in the world price can result either from an increase in global supply or a decrease in global demand. But in the latter case, we would expect to see exactly the same pattern as in recent quarters—falling prices accompanied by slowing global growth, with lower oil prices cushioning, but likely not reversing, the growth slowdown.

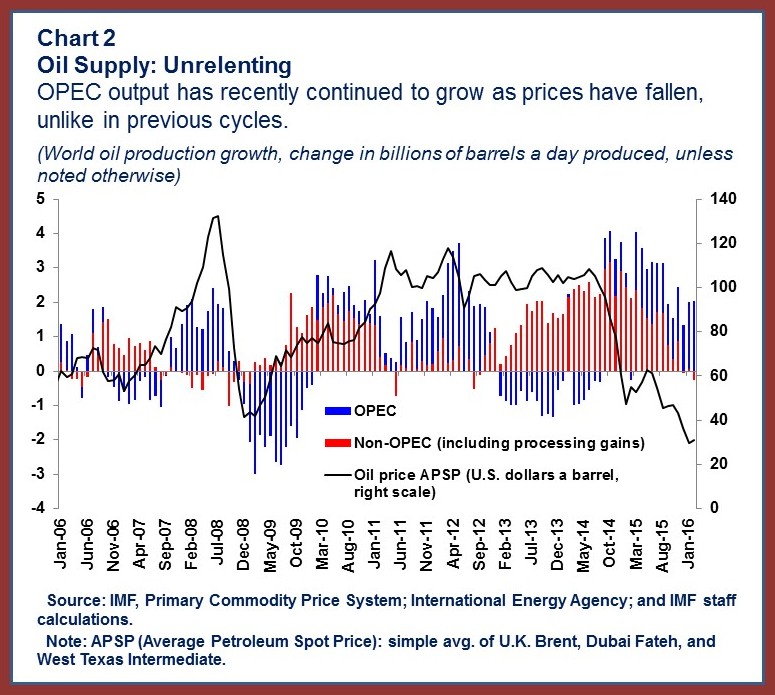

Slowing demand is no doubt part of the story, but the evidence suggests that increased supply is at least as important. More generally, oil supply has been strong owing to record high output from members of the Organization of the Petroleum Exporting Countries (OPEC) including, now, exports from Iran, as well as from some non-OPEC countries. In addition, the U.S. supply of shale oil initially proved surprisingly resilient in the face of lower prices. Chart 2 shows how OPEC output has recently continued to grow as prices have fallen, unlike in some previous cycles.

Continue reading here.

Below is an iMFdirect post by Maurice Obstfeld, Gian Maria Milesi-Ferretti, and Rabah Arezki:

Oil prices have been persistently low for well over a year and a half now, but as the April 2016 World Economic Outlook will document, the widely anticipated “shot in the arm” for the global economy has yet to materialize. We argue that, paradoxically, global benefits from low prices will likely appear only after prices have recovered somewhat,

Posted by at 12:07 PM

Labels: Energy & Climate Change

Breaking the Link between Housing Cycles, Banking Crises, and Recession

“By not reflecting liquidity risks in capital requirements, banking and insurance regulators have conjured up a dangerous system in which financial firms without liquidity take liquidity risks and financial firms with liquidity fail to do so. Two simple regulatory steps could change this system. Financial firms need to maintain a long-term stable funding ratio, and the regulatory risk weightings of assets should take into account the maturity of liabilities. These changes would encourage institutions with liquidity (life insurers, pension funds, and others with long-term liabilities) to provide it through instruments such as the self-rescheduling mortgage. They would also encourage banks to sell their illiquid assets to institutions with liquidity or lighten their dependency on short-term funding. Read the full article…

Posted by at 9:00 AM

Labels: Global Housing Watch

Wednesday, March 23, 2016

Monetary Policy and Financial Stability: Canada’s House-Price Dilemma

Canada’s housing market is sizzling hot and the Bank of Canada has a monetary policy dilemma: increase interest rates to cool the housing market would hurt borrowers and the economy; keep interest rates low adds fuel to the borrowing that led to the rise in housing prices and in household debt. What to do?

Housing headache

The latest national data on house prices in February suggest a year-on-year increase of 9 percent. House prices in Vancouver and Toronto—that contribute about a third of Canada’s GDP—have led the increase.

Canada’s housing boom has been accompanied by a steady rise in the nation’s household debt to 165 percent of disposable income by the end of 2015 (see chart). One way to cool the housing sector is to increase interest rates, but that would hurt the slowing economy, which has been hit hard by the decline in oil prices. Hence, the dilemma.

Low mortgage rates are an important factor feeding the housing market boom. This has helped keep interest payments low even as the size of the average mortgage has risen. As the figure shows, the share of interest payments in households’ disposable income has declined from 9 percent in 2008 to 6 percent in 2015, while the average size of mortgages has increased by some 40 percent over the same period. This means more households are able to afford more expensive homes, which, in turn, prompts households to borrow more money and get further into debt, while house prices continue to be pushed upward. This process should continue as long as employment is robust and interest rates remain low.

The Bank of Canada is rightly concerned about the rise in household debt, which makes the economy more vulnerable to unanticipated shocks and financial strains more probable. A mini version of this is playing out in Alberta, which has the third highest level of household debt among the provinces—after British Colombia and Ontario—and was hit by a large terms of trade shock from the oil price decline. The Alberta economy is expected to have contracted by almost 2 percent last year amid massive layoffs by the oil industry and house prices fell by 4 percent since their peak in late 2014.

Continue reading here.

Via iMFdirect:

Canada’s housing market is sizzling hot and the Bank of Canada has a monetary policy dilemma: increase interest rates to cool the housing market would hurt borrowers and the economy; keep interest rates low adds fuel to the borrowing that led to the rise in housing prices and in household debt. What to do?

Housing headache

The latest national data on house prices in February suggest a year-on-year increase of 9 percent.

Posted by at 9:00 AM

Labels: Global Housing Watch

Monday, March 21, 2016

Financial Stability and Interest-Rate Policy

The paper notes that “At the current conjuncture Canada represents an interesting case: Monetary policy faces the dilemma of supporting a struggling economy by cutting interest rates and maintaining financial stability in a context of high household debt and ever growing housing prices.”

The paper’s “findings show that it is very unlikely that the benefits of having a meaningfully tighter policy (i.e., at least 25 basis points higher than otherwise) would outweigh its costs, in the current Canadian context. In fact, even though the interest rate increase reduces the growth of real household credit and house prices and the ratio of household debt to GDP, the reduction in the crisis probability is minor and peaks only after about 8 years. At the same time, costs are front loaded and magnified by the tighter economic conditions. The policy rate path which takes into account financial stability risks is, thus, only 6 basis points higher than otherwise (for 8 quarters)—which, quantitatively, is not a meaningful policy alternative. A policy rate that is 25 basis points higher than otherwise (for 8 quarters) is expected to be welfare improving only under a scenario where a crisis would impose severe costs on the economy and real credit is expected to grow (in absence of policy intervention) at or above 9 percent a year for the next 3 consecutive years.”

“Should monetary policy use its short-term policy rate to stabilize the growth in household credit and housing prices with the aim of promoting financial stability? (…) the answer is no— especially when the economy is slowing down”, according to a new IMF working paper by Andrea Pescatori and Stefan Laseen–Financial Stability and Interest-Rate Policy: A Quantitative Assessment of Costs and Benefits.

The paper notes that “At the current conjuncture Canada represents an interesting case: Monetary policy faces the dilemma of supporting a struggling economy by cutting interest rates and maintaining financial stability in a context of high household debt and ever growing housing prices.”

Posted by at 7:50 PM

Labels: Global Housing Watch

Subscribe to: Posts