Thursday, July 5, 2018

Germany’s Housing Market: Preventing Financial Excesses

The IMF’s latest report on Germany says that:

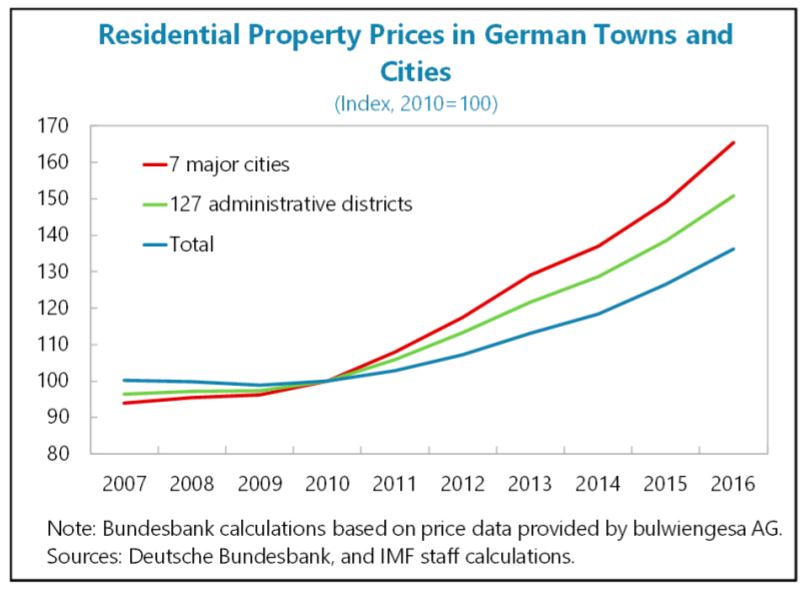

“Staff analysis suggests that house prices have risen faster than can be explained by demand and supply fundamentals in Germany’s major cities. House prices are rising moderately at the aggregate level, but have increased at double-digit rates in some hot spots where they

appear overvalued. Housing demand is driven by rising household income, large immigration flows in recent years, and low interest rates (…). On the supply side, stringent zoning restrictions (including for environmental protection) and high and rising capacity utilization (including labor shortages) in the construction sector prevent a more agile response of supply to price developments. House prices are most overvalued in Munich, Hamburg, Hannover, and Frankfurt, and are estimated to be more than 20 percent above their fundament level on average in major German cities (…). The Bundesbank obtains similar overvaluation estimates for some German cities in its latest assessment. As recommended in the past, lowering the effective burden of tax on new construction and reexamining zoning restrictions, in particular where demand is not likely to abate, would help mitigate price pressures.New housing policies, aimed at improving affordability, are not expected to have a

noticeable impact on prices. The government foresees spending €2 billion in renewed support for social housing in 2020–21, expanding the land available at a discount for social housing construction, and creating tax incentives to build on unused land. It also plans to allocate €2 billion to families with children acquiring a first home. Other measures are still being contemplated, including tax subsidies for rental housing, public loan guarantees and real estate tax exemptions to reduce equity requirements for owner-occupied houses, and strengthening rent controls. As these measures have counteracting effects on housing supply and demand, the overall impact on housing prices is likely to be small.Mortgage growth at the aggregate level has been moderate so far. Housing loans have

grown only marginally faster than GDP in recent years. German households are not highly leveraged (household debt stood at 53 percent of GDP at end-2017) and the overall debt-service-to-income ratio is low and declining (…). Mortgage lending spreads have compressed due to high competition among banks, but no widespread deterioration of lending conditions has been observed. Mortgage credit is recourse and based on fixed interest rates.However, data gaps prevent a full assessment of financial stability risks in the housing sector and should be urgently addressed. The absence of regional credit statistics and granular loan information prevents a full assessment of potential financial stability risks in specific market segments. The distribution of housing credit growth by type of bank, for instance, suggests that there could be important differences between major urban centers and the rest of the country. Given this, it is increasingly urgent that data gaps should be addressed.

The macroprudential toolkit should be strengthened. New tools—loan to value (LTV)

caps and amortization requirements—were legally created in 2017, a welcome development.

However, income-based instruments, such as the debt-to-income ratio and the debt-service-to income ratio, are not included in the legislation. These tools, which can help prevent an excessive build-up of debt by households when house prices are rising rapidly, should be added.Given rapidly rising house prices in some cities alongside data gaps that hinder a full

assessment of risks, early activation of macroprudential tools should be considered. As noted

in the 2016 Financial Sector Assessment Program (FSAP), international experience suggests that macroprudential tools should be deployed early to be most effective. It is therefore important that the macroprudential framework is sufficiently nimble such that instruments can be utilized preventatively to avoid the build-up of vulnerabilities. In Germany, early activation would help preserve financial stability by dampening risks of excessive leverage, especially in the context of insufficient data to assess whether pockets of vulnerability are arising. To the extent that vulnerabilities are not present, macroprudential measures—such as application of LTV caps and amortization requirements—would not likely be binding anyway. On this basis, consideration should be given to early activation of the existing macroprudential tools.Authorities’ Views

The Bundesbank monitors developments in the real estate markets closely, and authorities assess corresponding financial stability risks to be low. An early activation of borrower-based macroprudential tools is deemed unjustified at this stage and would face legal obstacles. They saw overvaluation concerns as localized and the lack of substantial credit growth or deterioration of credit standards, alongside households’ strong balance-sheets, as reassuring. They therefore saw no need for activation of LTV caps or amortization requirements at the present juncture. They fully shared staff’s concern over the information gaps which prevent a fuller assessment of risks. The authorities highlighted that microprudential tools are available and can be effectively used to address bank-specific concerns.”

Posted by at 11:04 AM

Labels: Global Housing Watch

Subscribe to: Posts