Monday, August 27, 2012

House Prices in Singapore

In Singapore, “indicators of housing affordability are mixed. House prices have risen more quickly than median incomes, especially for HDB resale housing. In addition, the tighter LtV ceilings raise the bar on qualifying for a housing loan. On the other hand, all-time low mortgage interest rates (about 70 percent of which are at floating rates, currently between 1⅓ percent and 2 percent) have reduced debt servicing costs,” according to a new IMF report on Singapore.

Moreover, it says “Following successive rounds of policy tightening, together with external factors, home prices have remained flat since end˗2011, while the volume of transactions has declined noticeably. In particular, the share of foreign buyers collapsed in Q1:2012 to 5½ percent as a result of new macroprudential measures targeting foreigners and weakening external investment sentiment, with buyers from China falling by nearly 50 percent. The more-than-proportionate decline in purchases by Mainland Chinese may reflect the impact of the economic slowdown in China. Transactions in the luxury market have also fallen. However, the share in total transactions of “shoe box” apartments (with an area of less than 50 square meters) doubled in Q1:2012 to close to 20 percent. While this may reflect the characteristics of new supply coming on-stream, demand for such housing is strong, possibly because of the reduced affordability of standard-size units.”

In Singapore, “indicators of housing affordability are mixed. House prices have risen more quickly than median incomes, especially for HDB resale housing. In addition, the tighter LtV ceilings raise the bar on qualifying for a housing loan. On the other hand, all-time low mortgage interest rates (about 70 percent of which are at floating rates, currently between 1⅓ percent and 2 percent) have reduced debt servicing costs,” according to a new IMF report on Singapore.

Moreover,

Posted by at 9:25 PM

Labels: Global Housing Watch

Sunday, August 12, 2012

Interview with IMF Fellow Olivier Coibion

|

| Olivier Coibion |

Loungani: Congratulations on your selection as an IMF Fellow. Is this your first stint at a policy institution?

Coibion: Thanks, I’m thrilled to be here! I worked for a year at the CEA [U.S. Council of Economic Advisers] in 2000-01. It gave me an enduring sense of how economic theory and empirical methods can help address policy questions and make a difference in people’s lives. And because I happened to be there during the transition from the Clinton to the Bush administration, it was fascinating to see the change in style and personalities—and in the dress code. The suits got much more sober and I even had to start wearing a tie once the Bush administration was in place.

Loungani: Dress is casual at the IMF over the summer. You see the suits out in full force in the fall. What will you work on during your year here?

Coibion: I’ll continue some of my work on inequality. One project will look at links between inequality and financial crises, which folks at the IMF have also studied. I’ve also been studying the impact of monetary policy on inequality—who gains, who loses when the Fed changes its policy. This gets debated in policy circles a lot but not much in academia. Ron Paul says that expansionary monetary policies, or debasing the currency as he always puts it, raises income inequality; people on the left like Jamie Galbraith say the opposite.

Loungani: What do you find?

Coibion: We find that expansionary monetary policy has typically reduced U.S. inequality in the short run. This suggests that when the central bank can’t cut interest rates any more—when rates hit the so-called ‘zero lower bound’, as is the case at present—inequality will be higher than it would be otherwise. To avoid these additional increases in inequality at a time of crisis, the government should use other tools, such as targeted fiscal policies. I hope to do some more work on this while I’m here. More generally, I’ll be studying how best to sequence fiscal and monetary policies when the multipliers—the impacts of the policies on the economy—associated with each may vary with the state of the economy.

Loungani: Do you think the Fed has done enough to promote recovery?

Coibion: I think the zero lower bound [on interest rates] has certainly limited the size of their response. They would be lowering rates further if they could. But as the IMF’s latest review of the U.S. economy noted, the Fed still has a few options to further support economic activity, given the weak state of labor markets and given the significant downside risks that still exist.

Loungani: Do you think that to avoid hitting the zero lower bound in the future, central banks should raise the target rate of inflation?

Coibion: No, I don’t. A higher inflation rate also has economic costs. So raising the target inflation rate will confer the benefit that we’ll be less likely to hit the zero lower bound. But such episodes are rare. So the high benefits conferred on rare occasions have to be balanced against the small but frequent costs of having higher inflation. In some work I’ve done, it turns out that the costs consistently outweigh the benefits for inflation rates above 2%. So rather than raise the target rate of inflation to deal with future episodes like the Great Recession, I’d prefer the more aggressive use of temporary policies designed for precisely this kind of episode, such as additional quantitative easing or fiscal policy.

Olivier Coibion–Recent Publications:

- The Optimal Inflation Rate in New Keynesian Models: Should Central Banks Raise their Inflation Targets in Light of the ZLB?” (with Yuriy Gorodnichenko and Johannes Wieland), forthcoming in Review of Economic Studies.

- “Why are target interest rate changes so persistent?” (with Yuriy Gorodnichenko), forthcoming in American Economic Journal: Macroeconomics.

- “What Can Survey Forecasts Tell Us About Informational Rigidities?” (with Yuriy Gorodnichenko), 2012, Journal of Political Economy 120(1), 116-159.

- “One for Some or One for All? Taylor Rules and Interregional Heterogeneity” (with Daniel Goldstein), 2012, Journal of Money Credit and Banking 44(2:3), 401-432.

- “Are the Effects of Monetary Policy Shocks Big or Small?” 2012, American Economic Journal: Macroeconomics 4(2), 1-32.

- “Strategic Complementarity among Heterogeneous Price-Setters in an Estimated DSGE Model” (with Yuriy Gorodnichenko), 2011, The Review of Economics and Statistics 93(3), 920-940.

- “Monetary Policy, Trend Inflation, and the Great Moderation: An Alternative Interpretation” (with Yuriy Gorodnichenko), 2011, The American Economic Review 101(1), 341-370.

Olivier Coibion

Loungani: Congratulations on your selection as an IMF Fellow. Is this your first stint at a policy institution?

Coibion: Thanks, I’m thrilled to be here! I worked for a year at the CEA [U.S. Council of Economic Advisers] in 2000-01. It gave me an enduring sense of how economic theory and empirical methods can help address policy questions and make a difference in people’s lives. And because I happened to be there during the transition from the Clinton to the Bush administration,

Posted by at 7:31 PM

Labels: Profiles of Economists

Thursday, August 2, 2012

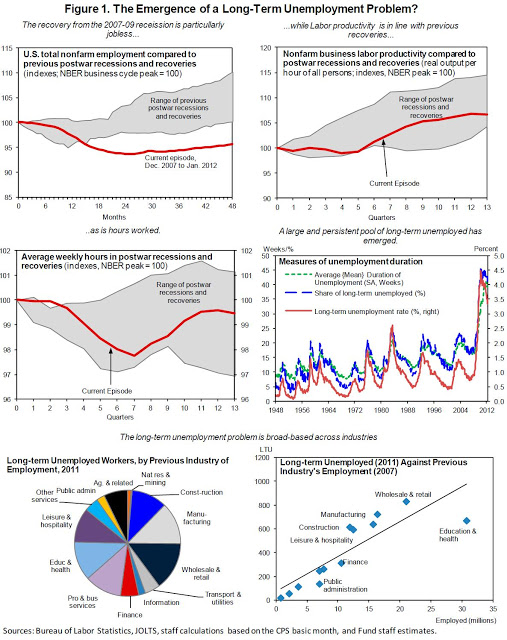

Is Long-Term Unemployment Pushing Up Structural Unemployment?

A new IMF report on US structural unemployment says that

while high long-term unemployment has not yet morphed into a permanent structural problem, it does pose an upward risk to the structural rate of unemployment. We have found that long-term unemployed are significantly less likely to find a job now than before the crisis, and that the loss in labor market matching efficiency observed since the recession is entirely due to a worsening of the labor matching of the long-term unemployed. Together, these results point to a risk that the structural rate of unemployment might be greater now than before the crisis.

Hence, forceful measures should be introduced that reduce long-term unemployment and address the risks associated with long spells of unemployment, namely skills erosion and a weaker attachment to the labor force. These measures include policies to increase demand for the long-term unemployed in the short run (active labor market policies, ALMP). When appropriately designed, such policies have been shown to be effective in improving employment and earnings prospects of long-term unemployed workers (Card et al, 2010; Card and Levine, 2000; Heinrich et al., 2008; Hotz et al., 2006). In particular, as discussed in the Staff report, a significant increase in ALMP resources is warranted given the persistently large pool of long-term unemployed and the risk that, as duration lengthens, their skills and attachment to the workforce might erode. Indeed, in terms of resources per long-term unemployed, the United States spends relatively little on active labor market policies, both compared to other OECD countries, and relative to its own pre-recession levels.

A new IMF report on US structural unemployment says that

while high long-term unemployment has not yet morphed into a permanent structural problem, it does pose an upward risk to the structural rate of unemployment. We have found that long-term unemployed are significantly less likely to find a job now than before the crisis, and that the loss in labor market matching efficiency observed since the recession is entirely due to a worsening of the labor matching of the long-term unemployed.

Posted by at 3:34 PM

Labels: Inclusive Growth

House Prices in the US

The authorities noted that the series of measures taken since last year to support the housing market were starting to bear fruit. These measures include in particular an expansion of the Home Affordable Refinancing Program (HARP) for loans owned or guaranteed by the GSEs, and a strengthening of the Home Affordable Modification Plan (HAMP), including loosened eligibility criteria through the elimination of debt service-to-income cutoffs, and the tripling of incentives for investors to carry out principal reductions under HAMP’s Principal Reduction Alternative (PRA) (Box 5). Recent data suggests that the October 2011expansion of HARP seems to have led to a significant increase in HARP refinancing. The share of loans that have benefited from a principal reduction under the modification program (Home Affordable Modification program of HAMP) has also been on the rise, and early signs show that the tripling of the incentives for principal reductions is receiving interest from investors, and is likely to spur further principal reductions in the future. The recent State Attorneys General Settlement with the major banks, which resolved claims about improper foreclosures and abuses in servicing the loans, could lead in the medium run to a non-trivial reduction in foreclosures, including through up to $34 billion of principal reduction. Early signs indicate that the settlement has led banks to delay foreclosures and also to increasingly substitute them with “short sales” of underwater properties, which are less costly and count toward the banks’ commitment for principal reduction under the settlement. The authorities highlighted that greater reliance on short sales, as opposed to foreclosures, could support the housing market going forward.

The mission welcomed this progress, but also noted that more aggressive policy action may be warranted to accelerate the resolution of the housing crisis. As noted in the Fed’s November 2011 white paper, housing markets do not self-correct efficiently and, absent forceful policies to support the market, prices could fall below their equilibrium levels due to feedback loops from prices to demand and supply. If house prices are anticipated to decline, potential buyers could stay out of the market even if interest rates are low. Moreover, a decline in prices reduces housing equity, triggering further defaults and foreclosures. Foreclosures, in turn, put renewed downward pressure on prices, not only by adding to the supply of houses for sale, but also because they lead to a destruction of value and impose “deadweight” losses on the economy, hurting consumer wealth and credit availability.

The IMF’s 2012 annual report on the US economy says that “house prices have shown some firming recently, with a surprising increase in Q1 2012.” It also highlights that

The authorities noted that the series of measures taken since last year to support the housing market were starting to bear fruit. These measures include in particular an expansion of the Home Affordable Refinancing Program (HARP) for loans owned or guaranteed by the GSEs, and a strengthening of the Home Affordable Modification Plan (HAMP),

Posted by at 3:33 PM

Labels: Global Housing Watch

Subscribe to: Posts