Thursday, March 8, 2018

Housing Market in Belgium

The latest IMF report on Belgium says that:

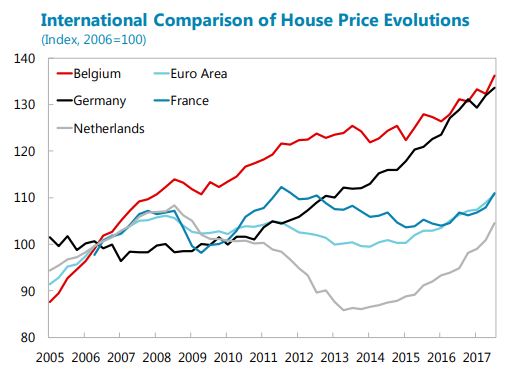

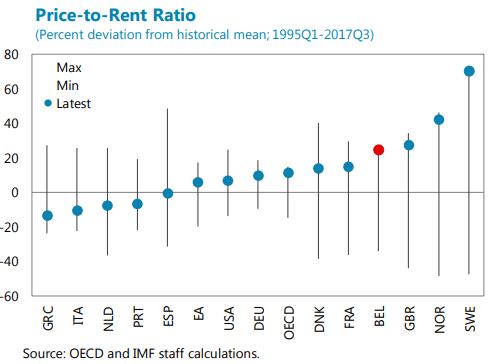

“The housing market appears to be only moderately overvalued, but pockets of vulnerability exist. Having grown rapidly in the 2000s, residential housing prices did not experience a sharp decline during the crisis, and have since risen by about 20 percent in nominal terms. The price-to-rent and price-to-income ratios stand well above their historical averages. More sophisticated measures, however, indicate only a moderate overvaluation. Since 2015 there has been a reversal in the tightening of mortgage lending standards, as evidenced by a growing share of loans with high loan-to-value (LTV) and/or high debt service-to-income (DSI) ratios. Risks are mitigated to some extent by the fact that Belgian households generally hold considerable financial assets. Nevertheless, nearly a third of outstanding mortgage debt is held by households whose liquid financial assets cover less than six months of debt service.

It will be important to stand ready to tighten macroprudential conditions further if balance sheet risks were to grow significantly. To address growing risks in the housing market, the NBB in 2014 introduced a 5 percent risk weight add-on for banks using internal ratings models to determine their minimum regulatory capital requirements for mortgage loans. In 2017, the NBB proposed a tightening of macroprudential policies through a targeted increase in capital charges linked to the riskiness of exposures, proxied by LTV ratios. However, as this proposal was not accepted by the government, the NBB subsequently proposed a new macroprudential measure requiring banks with riskier mortgage portfolios to hold more capital. This measure should be enacted promptly. Looking ahead, it will be important to strengthen the NBB’s ability to deploy cyclical macroprudential measures in the financial sector in a timely manner.”

Posted by at 4:26 PM

Labels: Global Housing Watch

Subscribe to: Posts