Monday, November 30, 2015

Labor Migration across U.S. States: An Update

A commonly-held view is that when a U.S. state is experiencing tough times (relative to other U.S. states), workers quickly leave the state for greener pastures; this keeps the state’s unemployment rate from going up too much and its labor force participation rate from declining too much.

My new work (with Mai Dao and Davide Furceri) offers a less sanguine view of the ability of U.S. workers to shield themselves from the consequences of adverse shocks. We show that, particularly in the short run, the adjustment to tough times occurs more through unemployment rates going up than through people leaving the state. And while migration picks up during recessions, people in the states that are doing very poorly have a difficult time exiting.

Here is a link to the paper and a technical summary of the paper:

Our first key finding is that labor mobility is less important as a cyclical adjustment mechanism, relative to changes in unemployment and participation, than suggested in earlier work. Some of this shift in view comes from the addition of over 20 years of data to the previous work. But the main reason is that, given the availability of official interstate net-migration data starting in 1991 we can also directly look at the behavior of migration, as opposed to backing it out as a residual. We find that it is primarily the relative unemployment rate, not net migration, that is the main adjustment mechanism in the first two years following a relative shock to state labor demand.

Our second set of findings pertains to a newer literature that documents longer-run movements in U.S. mobility, particularly the steady and widespread reduction in gross internal migration rates since the 1980’s. Here we establish several results that reveal important patterns in regional adjustment mechanisms.

- First, in the last two decades or so starting 1990, the response of net migration to given regional shocks in the short run has decreased, as has the response of relative unemployment and participation rates, resulting in less dispersion of employment growth in response to given dispersion in relative labor demand shocks.

- Second, the smaller migration response to shocks is driven entirely by less net out-migration from states that experience adverse labor demand shifts, whereas the net in-migration response to states with favorable labor demand shifts has increased or remained constant (depending on time horizon). This also suggests that in-migrants to the best states do not disproportionately come from the poorest states, a sign of lack of migration directedness and of scope for efficiency gains from an aggregate perspective.

- Third, despite the trend decline in gross migration rates since the early 1990’s, the migration response to a state-relative demand shock increases strongly in recessions, hence potentially playing a larger role as shock absorber during aggregate downturns than in normal times. Importantly, we observe that this counter-cyclical response of migration is driven primarily by a stronger response of positive net migration into states that do relatively better during recessions, while negative net migration from states that do relatively worse only increases by less and the response is delayed, occurring toward the end of the recession. When a state like North Dakota does relatively better than average during a recession thanks to the shale gas boom, it attracts disproportionately more in-migration than for instance Texas during an expansion, when strong demand for oil creates more jobs in Texas than elsewhere. However, the migrants into North Dakota during the recession do not come disproportionately more from states that are doing worse than average, say Michigan, as one would expect.

A high degree of mobility has long been considered a distinguishing feature of the U.S. labor market.

A commonly-held view is that when a U.S. state is experiencing tough times (relative to other U.S. states), workers quickly leave the state for greener pastures; this keeps the state’s unemployment rate from going up too much and its labor force participation rate from declining too much.

My new work (with Mai Dao and Davide Furceri) offers a less sanguine view of the ability of U.S.

Posted by at 5:12 PM

Labels: Inclusive Growth

Fund Fires Employment Guru?

RG: What was the group set up to do?

Loungani: On jobs, the immediate task was to remind people that sometimes unemployment is high because demand is low. The Fund, like many others, often veers towards thinking of unemployment as largely a supply-side problem—people are lazy or we give them very generous unemployment benefits so they don’t search for jobs or there are structural problems that keep unemployment high. At the onset of the Great Recession, Olivier (Blanchard) and Min (Zhu)—who had oversight over the group—were worried that we would underplay the most obvious explanation for why unemployment had spiked up, namely that aggregate demand had fallen. Our mission was to keep the words “aggregate demand” alive within the building and outside.

RG: Did you succeed?

Loungani: Perhaps more outside the building than within it, at least initially. Under Olivier’s supervision—he gave me a two-page outline and said “follow this”—Mai Dao and I wrote a 2010 paper which Paul Krugman praised: “A recovery in aggregate demand is the single best cure for unemployment. What a relief to hear the IMF say that!” This sentiment was echoed by many others over the ensuing years, including many in the trade union movement. We had a tougher time at other institutions: after one of my presentations in Europe a person came up to me and said: “I heard the same thing from Olivier 30 years ago and I didn’t believe it then.”

RG: And within the Fund building?

Loungani: It has been a tough sell. Larry Ball (of Johns Hopkins), Davide Furceri, Daniel Leigh and I kept up a drumbeat that the short-run relationship between output and unemployment—known as Okun’s Law—had remained stable through the Great Recession. Antonio Spilimbergo started calling us the “Okun police”. I think it eventually started to rub off; one piece of evidence is EUR’s paper on the rise in youth unemployment, which provides an even-handed treatment of the respective roles of aggregate demand and supply factors.

RG: What was the task on growth?

Loungani: Olivier put it as “moving beyond mantras”. Both he and I had the view that the Fund goes to countries and says: “Here are 25 (structural) areas on which you are behind international standards. Improve on all them by next year and you will surely grow”. So I started to look through the Fund’s advice on growth.

RG: What did you find?

Loungani: That the characterization is unfair. Though you can still find examples of the kind I mentioned, the bulk of the Fund’s advice on growth is actually quite ‘granular’; that is, it digs down to see the specific problems the country is facing. Think, for example, of the great work that Patrizia Tumbarello and many other Fund staff have done in providing advice to small states on sustainable growth.

RG: So what did the group do?

Loungani: In the “Jobs & Growth” Board paper, we summarized the current ‘do’s and don’ts’ on growth and then showed that staff had been broadly following that advice. We also issued a very nice guidance note for Fund staff on how to tackle growth issues—I am not praising myself here as this was largely the work of several SPR colleagues. In this case too, as with jobs, we got some external recognition—in this case some back-handed praise from Dani Rodrik, who in the past has been critical of our advice on growth.

RG: And, finally, on inequality?

Loungani: Here the guidance came largely from Min (Zhu), at least initially. Around 2010-11, when the group’s work started, Min was more concerned about inequality than was Olivier. Min said we should see how policies, including Fund policies, affect inequality, so we could take these effects into account in our surveillance and program work.

RG: So does Fund policy advice affect inequality?

Loungani: One of the first things we did was to see how fiscal consolidations—referred to as ‘austerity’ outside our building—affected inequality. In a 2011 piece we found that austerity raises inequality. This initially proved controversial within the building—and, not surprisingly, popular in some circles outside—but management supported us and the paper was published. In 2014, FAD did a very nice Board paper on fiscal policy and inequality and has just issued a new book on the topic. Recently we have shown that openness—capital account liberalization—raises inequality; I hope MCM picks up on this, the way FAD did with fiscal policy. Min also wanted us to see how monetary and exchange rate policies affect inequality; I never got around to it but hope springs eternal—here again MCM could help.

RG: What’s next for you?

Loungani: I have a few residual tasks to complete in the Jobs & Growth agenda. One is to finish extensions of the work on Okun’s Law to emerging markets and low-income countries. The other is to think about the advice the Fund gives to these countries on the design of labor market institutions. This was a topic close to Olivier’s and my hearts; but while Olivier and I did a paper on it for advanced economies (with Florence Jaumotte), I never got around to doing the follow-up paper for other countries. But my main job is to head the division within RES that deals with low-income countries.

RG: And what’s next for the group? Is it disbanded and how would you summarize its impact?

Loungani: Well, my co-chair Ranil Salgado and I have both moved on. But the agenda continues under new management—and the seminar series we launched continues as well. In RES, Romain Duval has taken over and had added structural reforms to the agenda—this is good as the focus we had placed on aggregate demand was appropriate for the time but we should be even-handed. And of course, inequality has become a big deal at the Fund now—with the astounding success of the work by Jonathan Ostry and Andy Berg, the blossoming work on gender inequality, the pilot cases on operationalizating inequality.

On the impact: I suspect Gerry Rice would not call it “huge”. But, in the words of the poet, we managed “to swell a progress, start a scene or two.”

So, did the Fund fire its employment guru? Well, not quite, but after five years at the helm of the Fund’s Jobs & Growth working group, Prakash Loungani is moving on to other assignments. RES GESTAE spoke to him about the group’s travails in promoting the Fund’s work on jobs, growth and equity.

RG: What was the group set up to do?

Loungani: On jobs, the immediate task was to remind people that sometimes unemployment is high because demand is low.

Posted by at 3:33 PM

Labels: Inclusive Growth

Canada’s Housing Market: Which Way Now?

When looking at the national level, “moderate overvaluation is still observed (…). The inventory of completed and unsold units has trended higher and is above its historical average in large part because of the multi-unit segment”, says Canada Mortgage and Housing Corporation (CMHC). When looking at the local level, CHMC notes that there is “strong overall evidence of problematic conditions in Toronto, Winnipeg, Saskatoon and Regina. In Toronto, strong evidence of problematic conditions reflects a combination of price acceleration and overvaluation. Strong evidence of problematic conditions in Winnipeg, Saskatoon, and Regina reflects detection of overvaluation and overbuilding.” The divergence in Canada’s housing market is also pointed out by Scotiabank and the Canadian Real Estate Association. On developments in the west part of Canada, CMHC is expecting to see more homeowners fall behind in their mortgage payments as a prolonged slump in oil prices hit household budgets. Finally, the OECD recently released a report warning that the “newly completed but unoccupied housing units have soared in Toronto, increasing the risk of a sharp market correction.” However, Benjamin Tal at CIBC says that the most widely used data on unabsorbed units overstates and misrepresents the level of condo inventory.

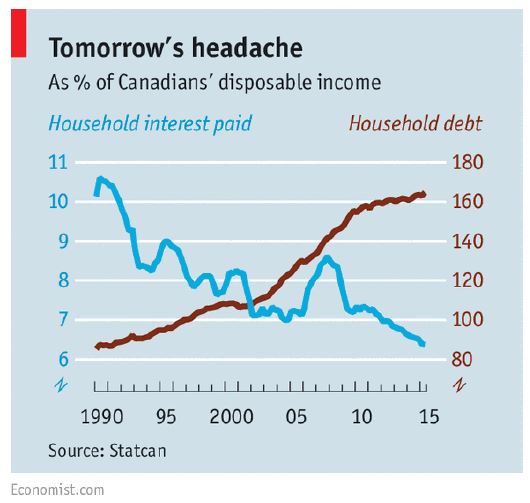

The views on household debt: “Consumer debt is a record 165% of disposable income. Most of that borrowing has gone into buying houses, which now look scarily overpriced”, says the Economist. TD Economics looked at the household debt issue in geographical terms. In doing so, TD Economics finds that “(…), financial vulnerability remains at elevated levels nationally. Households in British Columbia, Ontario and Alberta hold the top three spots, in that order. Households in these three provinces report having the highest debt-to-income ratios, devote the greatest share of income to making debt payments and have built up the highest degree of froth in their housing markets over the last decade.” Meanwhile, the Canadian Centre for Policy Alternatives looked at the household debt issues in terms of age group. It “(…) assesses the impact of a housing market correction on the net worth of Canadian families and finds a 20% decline in real estate prices would leave 169,000 families under 40 underwater, with more debts than assets.” However, the risk of household debt is not shared among the developers and builder community. A report by Ben Myers at Fortress Real Developments says: “The elevated level of household indebtedness in Canada is frequently cited as a vulnerability to the domestic economy, yet none of the builders and developers in our 2015 survey felt it was a significant risk to the housing market.” A new paper by the Central Bank of Canada finds “(…) that high and rising levels of both house prices and debt since the late-1990s can be mostly explained by movements in incomes, housing supply, mortgage interest rates and credit conditions, suggesting that the outlook for house prices and debt could depend mainly on the future paths of these variables.” A paper by Alan Walks (University of Toronto Mississauga) provides a picture of the emerging urban debtscape in Canadian cities, reflecting an essential element of the geography of risk and financialization. His research demonstrates that debt-related risk is associated with high and rising real estate values at each scale. Urban growth has thus brought with it significant new vulnerabilities, mainly related to housing costs and large mortgages, and this is particularly evident within Canada’s global cities.

Who is buying in the city of Vancouver? And how? New research by Andy Yan (Bing Thom Architects) looks at all the sales to occur within three west side neighborhoods in the City of Vancouver over a 6 month period and the ownership and mortgage patterns within these titles. There were a total of 172 transactions, with a total dwelling value of $525 million and with a starting price of $1.25 million and above. Here are some of the interesting findings: in terms of cash vs. mortgage, the study finds that 82 percent of the properties held a mortgage. In terms of ownership, 109 properties were listed with a single name and only 8 listed as corporation. In terms of occupations, 52 were listed as homemaker/housewife. And 66 percent of the 172 buyers had non-anglicized Chinese name. On a separate note, Tony Roy (BC Non-Profit Housing Association) says that nearly half of all renters are pouring more than 30 percent of their income into rent, while 24 percent in Metro Vancouver are spending more than half of their income on rent.

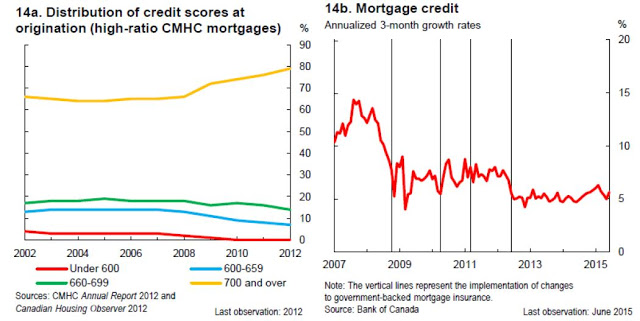

Macroprudential Policies: Are they working? More needed? According to the Central Bank of Canada, there have been four successive rounds of macroprudential tightening. The main target has been the rules for insured mortgages. For example, the maximum amortization period for insured loans has been shortened from 40 years to 25. Loan-to-value ratios have been lowered to 95 percent for new mortgages, and 80 percent for refinancing and investor properties. Qualification criteria such as limits on the total debt-service ratio and the gross debt-service ratio, as well as requirements for qualifying interest rates, have also been tightened.

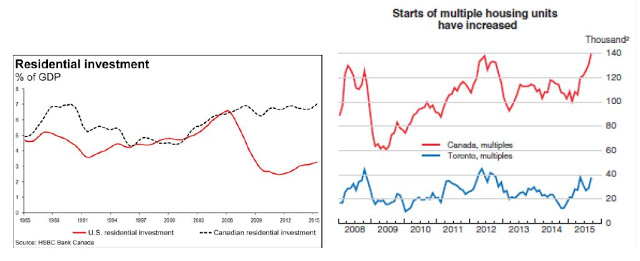

The measures taken have resulted in higher average credit scores, which have improved the quality of mortgage borrowing. With respect to household credit growth, the trend growth of mortgage credit declined from 14 percent in 2007–08 to around 5 percent in 2013–15. However, David Watt at HSBC Bank Canada says that there is a strong case for further macroprudential measures. He points out the trend in residential investment (see figure below on the left) and says that “the rise in residential investment as a percentage of GDP between 2002 and 2008 was in the backdrop of a generally rising terms of trade … With the terms of trade now worsening, it suggest that these trends should cool off, not accelerate.” Moreover, the OECD says that “(…) high household debt and strong price increases in some markets (single dwellings in Toronto and Vancouver) that are already expensive relative to fundamentals, further macro-prudential tightening on mortgage lending in these markets, such as maximum loan-to-value or debt-servicing ratios, should be implemented to ensure financial stability.”

From the Global Housing Watch Newsletter: November 2015

The views on the housing market: New research by National Bank Financial says that “There are now two housing markets in Canada.”

When looking at the national level, “moderate overvaluation is still observed (…). The inventory of completed and unsold units has trended higher and is above its historical average in large part because of the multi-unit segment”,

Posted by at 10:00 AM

Labels: Global Housing Watch

Sunday, November 29, 2015

Sovereign wealth funds in the new era of oil

As a result of the oil price plunge, the major oil-exporting countries are facing budget deficits for the first time in years. This column goes through the evidence, suggesting that the low price environment is likely to test the relationship between governments in oil-exporting countries and their sovereign wealth funds, at a time when spending is going up.

As a result of the oil price plunge, the major oil-exporting countries are facing budget deficits for the first time in years. The growth in the assets of their sovereign wealth funds, which were rising at a rapid rate until recently, is now slowing – and some have started drawing on their buffers.

Figure 1. Brent crude price, 2014-2015 (US dollars per barrel)

In the short run, this phenomenon is not cause for alarm. Most oil exporters have enough buffers to withstand a temporary drop in oil prices. But what will happen if low oil prices persist, and how will policymakers react? We explore here the fallout from low oil prices on sovereign wealth funds in oil-exporting countries and find that that they have important domestic implications. The impact on global asset prices will depend on the extent of unwinding of the sovereign wealth funds of oil exporters that will not be compensated by portfolio adjustment in other parts of the world that will in turn depend on their economic prospects.

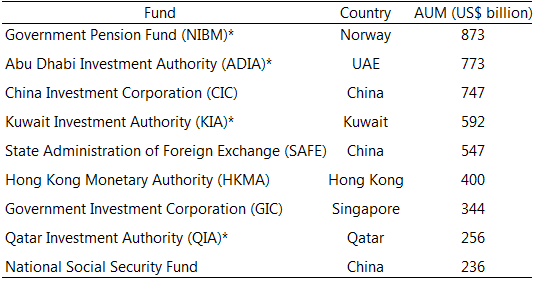

Figure 2. World’s biggest sovereign wealth funds, 2015 estimates

The rise of sovereign wealth funds

In the early 2000s, high oil prices brought about a massive redistribution of income to oil exporters, resulting in current account surpluses and a rapid buildup of foreign assets. Governments established new sovereign wealth funds or increased the size of existing ones to help manage the larger pool of financial assets. The total assets of sovereign wealth funds are concentrated in a few countries. As of March 2015, it is estimated at $7.3 trillion, of which $4.2 trillion are oil and gas related. While there are large differences across sovereign wealth funds, available information on their asset allocation points to a significant share in equities and bonds.

From Vox by Rabah Arezki, Adnan Mazarei, and Ananthakrishnan Prasad

As a result of the oil price plunge, the major oil-exporting countries are facing budget deficits for the first time in years. This column goes through the evidence, suggesting that the low price environment is likely to test the relationship between governments in oil-exporting countries and their sovereign wealth funds, at a time when spending is going up.

As a result of the oil price plunge,

Posted by at 11:49 AM

Labels: Energy & Climate Change

Tuesday, November 24, 2015

IMF’s Thanksgiving message: ensure benefits of foreign capital are shared broadly

“Davide Furceri and Prakash Loungani use an event-study framework — looking at what happens on average after clear changes in policy — to assess the effects of “neoliberal” policy changes (although they don’t put it that way) on inequality. Sure enough, they find that both fiscal austerity and liberalization of international capital movements are followed by noticeable rises in income inequality. So, if you were a ranting leftist, you might say that political attitudes are shaped by class, and that ideological justifications for high inequality are just a veil for class interest. You might also say that “sound” economic policies are really just policies that redistribute income upwards. And it turns out that the econometric evidence more or less supports your rant.”

Well, our evidence holds up to further scrutiny. And the conclusions we’d like you to draw from our work are summarized in our new blog. And then, if you really want to get a break from the in-laws, here’s the paper. Nothing clears the living room better than a statement like “Guys, let me tell you about this fascinating paper – its findings do not imply that countries should not undertake capital account liberalization, but it suggests an additional reason for caution.”

Happy Thanksgiving,

Prakash

Opening up capital markets, unless managed well, can raise inequality. That’s the message of a new working paper by Davide Furceri and me that the IMF released today. Paul Krugman, based on the early evidence from our work, wrote:

“Davide Furceri and Prakash Loungani use an event-study framework — looking at what happens on average after clear changes in policy — to assess the effects of “neoliberal” policy changes (although they don’t put it that way) on inequality.

Posted by at 8:34 PM

Labels: Inclusive Growth

Subscribe to: Posts