Wednesday, June 20, 2018

Are House Prices and Homeownership Moving in Tandem?

Global Housing Watch Newsletter: June 2018

In this interview, Carlos Garriga and Pedro Gete talk about their latest research: “Housing Recoveries without Homeowners: A Global Perspective.” Garriga is a Vice President at the Federal Reserve Bank of St. Louis. Gete is a Finance Professor at IE Business School.

Hites Ahir: “Housing Recoveries without Homeowners: A Global Perspective” is a blog that you recently co-authored with Daniel Eubanks (Federal Reserve Bank of St. Louis). What triggered your interest to work on this?

Carlos Garriga and Pedro Gete: Housing markets and housing finance are at the center of our research in macroeconomics. Housing played a key role in the lead up to the Great Recession, but also in the aftermath. Most of the new research has focused on analyzing that boom-bust cycle, ignoring the recovery period. We wanted to study what happened to housing markets after the Great Recession, and we found some new patterns that are surprisingly strong across countries.

Hites Ahir: What did you find?

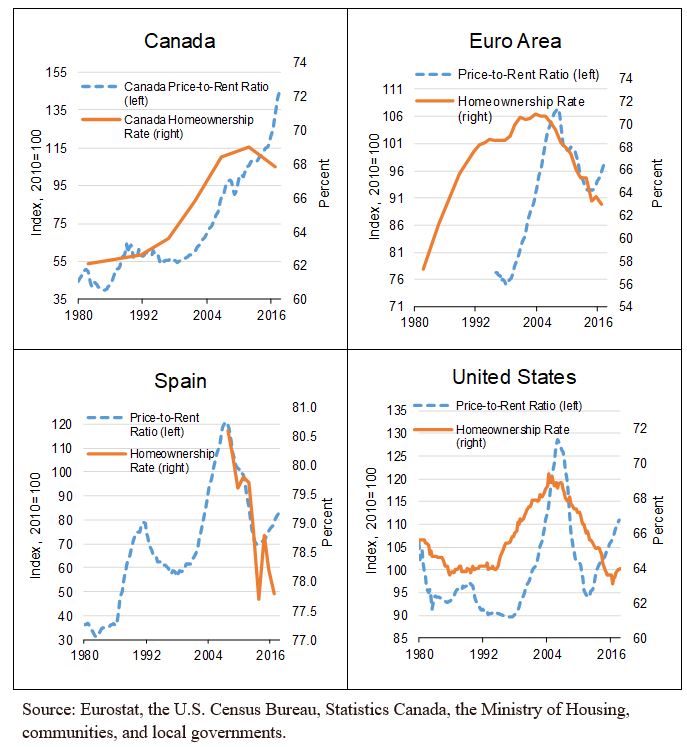

Carlos Garriga and Pedro Gete: In the postwar period, booms in house prices have been accompanied by sizeable increases in homeownership; that is, an increase in the number of households that own the house they occupy. Historically, these two series have usually been positively related. Our research, however, finds an important change in the correlation between these series in the post-Great Recession period for a large number of countries, including the United States. We currently observe a decoupling of house prices and homeownership.

This shift changes the traditional cyclical view of homeownership and house prices. Normally, during a recovery, households buy houses, driving up house values. In the post-Great Recession period, however, we see global increases in house prices and decreases in homeownership. Thus, we identify a new stylized fact that decouples the variables, hence the title “Housing Recoveries without Homeowners.”

Hites Ahir: Is this good news or bad news?

Carlos Garriga and Pedro Gete: Well, the ownership of housing wealth is becoming concentrated among a smaller number of individuals. Whether this is good or bad news is difficult to assess, as we are still in the early stages of the research project documenting these novel facts. It is essential to understand the key driving forces before assessing the welfare effects and prescribing particular policies. The key issue is that in many countries and cities, the focus of the policy debate has changed: households are complaining that “rents are too high,” when the usual complaint used to be that “prices are unaffordable.”

Hites Ahir: Is this also happening in countries with different circumstances (e.g., diverging monetary policy rates)?

Carlos Garriga and Pedro Gete: The fact is very robust across countries, and in the United States it is very evident across most MSAs. We need more work to understand the exact drivers, but it does not seem to be that monetary policy alone can explain the fact.

Hites Ahir: So, we are transitioning from a nation of homeowners to a nation of renters. Has this type of development happened before?

Carlos Garriga and Pedro Gete: In the United States and United Kingdom, homeownership rates were low until post WWII. It seems this was the case in other countries as well. Going back even earlier, the homeownership rate was even lower, as the absence of credit markets makes it very difficult to undertake such a large investment as a house.

Figure 1: Homeownership and Price-to-Rent Ratio

Hites Ahir: What explains the decoupling of house prices and homeownership?

Carlos Garriga and Pedro Gete: Several factors could be driving the decoupling of the price-to-rent ratio and the homeownership rate. From the housing supply side, there is a trend toward decreased construction of starter and midsized housing units. Developers have increased the construction of large single-family homes at the expense of the other segments in the market. Recent increases in regulatory costs could have encouraged builders to focus on larger homes with higher margins. Supply may be just reacting to developments in demand (discussed next).

From the demand side, there are three leading explanations, which are likely to be complementary and self-reinforcing. The first focuses on changes in individual preferences or attitudes toward homeownership. The second builds on changes in the access to mortgage credit. The third tentative explanation relates to changes in the investment nature of real estate.

Hites Ahir: In your note, you say that the “price of houses is again increasing more quickly than the price of rentals.” But, as you know, in some countries, rents are controlled. So how do you reconcile this fact with your findings?

Carlos Garriga and Pedro Gete: It is true that in some countries and cities rent controls might limit the growth of one factor. There are also areas, however, with units not subject to controls that cause prices to rise faster than rents, for example, San Francisco and New York City.

Hites Ahir: In your blog, you also talk about “changes in the investment nature of real estate.” Could you elaborate on this?

Carlos Garriga and Pedro Gete: There are several types of real estate investors with different goals and targets in terms of the type of investment (i.e., single family vs. multi-family homes): First, there are sole proprietorship investors (i.e., “mom & pop”) looking for investment income. Second, there are foreign investors. Third, there are new institutional property owners, such Invitation Homes and American Homes 4 Rent, among others. In fact, since 2016, the real estate industry group has been elevated to the sector level in the S&P Dow Jones Indices.

Technology and globalization have made it easier for the second and third types to increase. For example, technology now makes it profitable to rent single-family houses. In addition, the widespread use of Internet rental portals such as Airbnb and VRBO has increased the opportunity to offer short-term leases, increasing the revenue stream from rental housing.

Hites Ahir: What is next for your research?

Carlos Garriga and Pedro Gete: A closely related issue is to what extent current homeownership rates are artificially high because of an aging population—a global phenomenon. The decline in the number of homeowners is observed across most age groups, but it is also true that the fraction of households over age 45 that are homeowners is substantially larger than for younger households. For this reason, population aging mechanically increases the homeownership rate. For example, in the United States, eliminating the aging effect would generate a homeownership rate of 60.9 percent instead of the observed 63.9 percent—suggesting the impact of aging is quite large. We have a lot of work to do, but we are enthusiastic the topic is worthy!

Posted by at 5:01 AM

Labels: Global Housing Watch

Subscribe to: Posts