Wednesday, November 21, 2018

Developments in Spain’s Housing Market: Already a Cause of Concern?

From the IMF’s latest report on Spain:

“House prices have increased in recent years, although from a low level and without signs of a construction boom. While there is no clear evidence of a significant price misalignment yet, the authorities need to be vigilant. The set of macroprudential tools should be expanded to deal with potential financial stability risks.

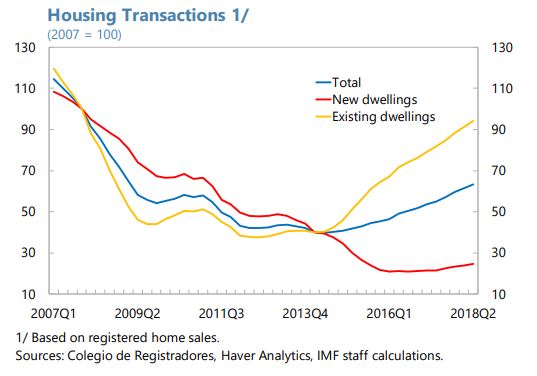

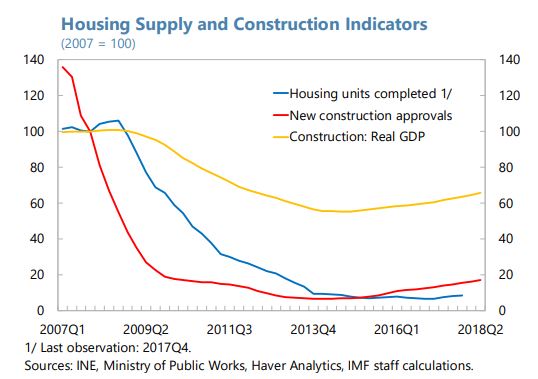

The ongoing price recovery is not associated with a construction boom. House prices have increased by around 15 percent between 2014–17, boosted by fast recoveries in cities like Madrid and Barcelona. Registered sales have disproportionately risen among existing dwellings, whereas new-dwelling transactions are still well below their pre-crisis peak. Despite early signs of mild supply-side recovery, such as an increase in new construction approvals from a low level, the housing stock has barely risen so far. In the overall economy, the contribution of value added from the construction sector is nearly half of what it was before the crisis. These trends have been accompanied by a small decline in home ownership (from 80 to 77 percent between 2008–17), while renting activity has strengthened. Against this background, new rent subsidy programs and social home loans were recently introduced. The authorities are also considering expanding the social housing stock.

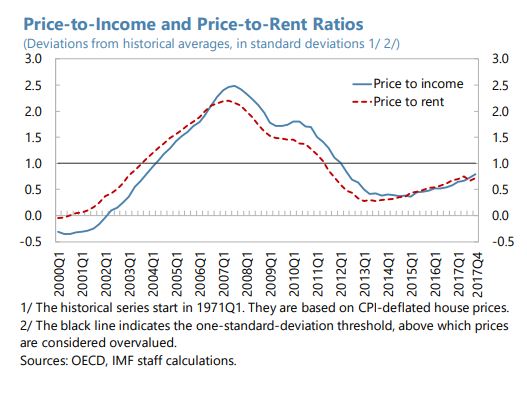

Although house prices are rising, there is no strong evidence of a clear overvaluation yet. Two approaches are used to assess house price misalignment. The first approach measures deviations from historical averages of the price-to-rent and the price-to income ratios. As of 2017:Q4, both ratios stand at roughly similar levels as in mid-2003 and less than one standard deviation above their historical averages, thus indicating no overvaluation. The second approach is a regression that includes the growth rates of income per capita, working-age population, interest rates, equity prices, and construction costs, as well as a long-term equilibrium relationship with the price-to-income ratio, which measures housing

affordability. This model suggests a slight overvaluation in 2017:Q4. However, this regression-based result should be treated with caution given that the model is particularly

limited in capturing supply-side dynamics.To prevent financial stability risks emerging, the macroprudential toolkit should be expanded and ready to be used. While housing valuation gaps are not significant so far and households’ balance sheets have gradually improved since 2012, persistent demand pressures in the housing market could increase risks to financial stability. As noted in the 2017 FSAP, banks are highly exposed to real estate sector developments, and therefore the macroprudential toolkit should be expanded to deal with risks associated with that exposure (see IMF Country Reports No. 17/321 and 17/336). Other actions would be welcome to: (i) further improve balance sheets in the construction and real estate sectors; (ii) encourage greater use of fixed-rate mortgages; (iii) ensure that eligibility criteria for social home loans and rent subsidies are prudently assessed; and (iv) improve housing development regulation to address supply constraints. Any new measures aimed at reducing rent pressures should avoid causing negative supply-side effects with adverse impact on low-income renters.”

Posted by at 1:34 PM

Labels: Global Housing Watch

Subscribe to: Posts