Tuesday, April 21, 2020

Forecasting Turning Points: An Update

An update of my previous work on forecasting turning points. While the previous work was on how well economists could predict recessions, this one is on how well they can predict recoveries.

An update of my previous work on forecasting turning points. While the previous work was on how well economists could predict recessions, this one is on how well they can predict recoveries.

Posted by at 6:05 AM

Labels: Uncategorized

Monday, April 20, 2020

A Look at Demographia’s Latest Housing Affordability Survey

Global Housing Watch Newsletter: April 2020

*In this interview, Wendell Cox talks about Demographia’s latest housing affordability . Wendell Cox is an American urban policy analyst and academic. He is the principal of Demographia (Wendell Cox Consultancy). The survey is co-authored with Hugh Pavletich of Performance Urban Planning.

Hites Ahir: You recently released the 16th Annual Demographia International Housing Affordability Survey: 2020. Tell us about the housing affordability measure used in the survey.

Wendell Cox: Demographia uses the “median multiple,” which is the median house price divided by the median household income. This measure meets two important requirements for assessing middle-income housing affordability; it evaluates the relationship between housing costs and household incomes, and it measures the middle of the market.

Hites Ahir: How does your measure compare to other existing measures?

Wendell Cox: Demographia presents current housing affordability between markets as well as in an historical context. This may be the most important difference with other measures, which often consider only recent experience, limited to only a few years or a decade or two.

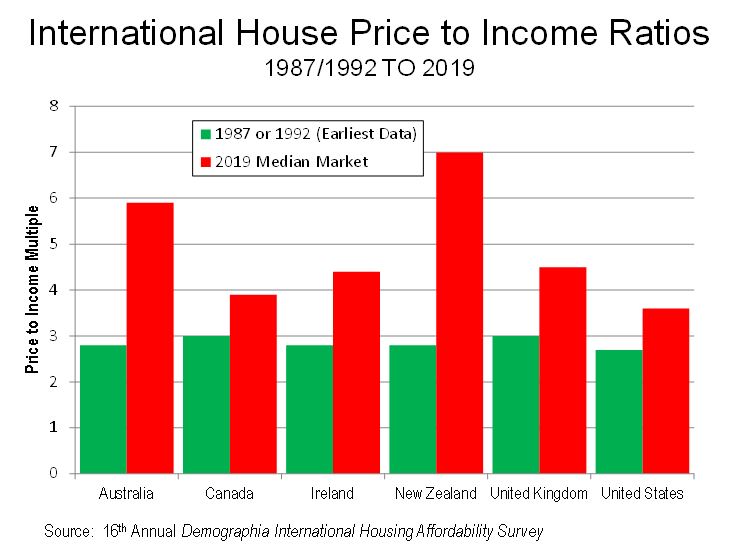

In many metropolitan markets, housing affordability has deteriorated significantly in the last three decades, from a time that in many nations the median multiple was 3.0 or below.

Figure 1.

Hites Ahir: Which countries and cities does it cover?

Wendell Cox:The Survey includes Australia, Canada, China (Hong Kong), Ireland, New Zealand, Singapore, the United Kingdom and the United States. The principal focus is on the more than 90 major housing markets areas (metropolitan areas) with more than 1,000,000 residents. More than 200 additional smaller markets are also included.

Hites Ahir: What is the overall message from the latest survey?

Wendell Cox: The message of this edition as well as the entire series is that governments should closely monitor housing affordability, to position themselves to restore it where it has been lost and maintain it where it remains.

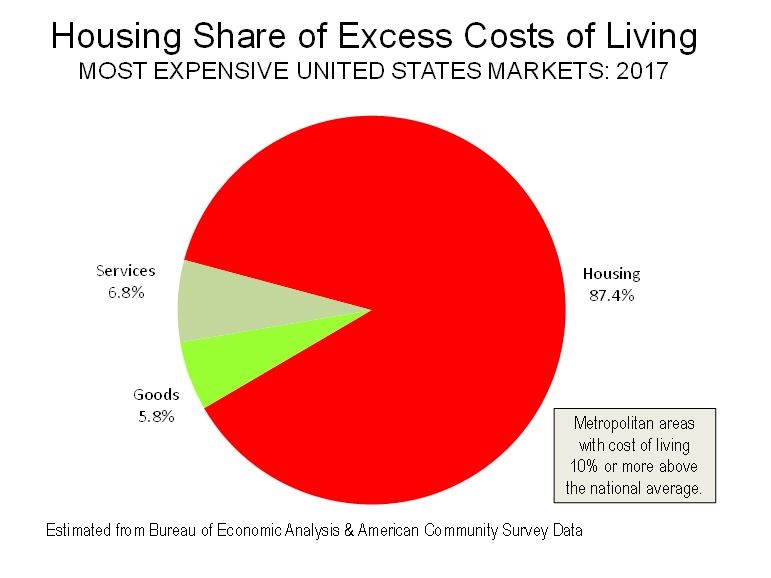

The costs of housing largely define differences in the cost of living and thus, the standard of living. In the United States, we estimate that 87 percent of the excess cost of living in higher cost metropolitan areas is comprised of housing costs.

This is an international problem, as is indicted in recent Organisation for Economic Cooperation and Development (OECD) research, Under Pressure: The Squeezed Middle-Class, suggests an existential threat to the middle-class in OECD countries. According to the OECD, the costs of living have risen much more rapidly than household incomes over the past three decades. Housing, according to the OECD, has been “the largest spending category” and “has been the main driver of rising middle-class expenditure in recent decades.” According to the OECD, owned housing costs have contributed more to the problem than those of rentals, though rental cost increases have been significant.

Figure 2.

Considerable economic research has associated diminished housing affordability with more restrictive land use regulation. In the Demographia Survey, virtually all of the major housing markets that are “severely unaffordable” have urban containment (such as urban growth boundaries and other policies that severely limit or prohibit new development on the urban fringe).

Research in Australia, New Zealand, the United Kingdom and the United States has found comparable land values spiking 10 times and more across urban growth boundaries. Within the San Francisco metropolitan area, economists Edward Glaeser of Harvard and Joseph Gyourko of the University of Pennsylvania found land values for median value houses were “roughly 10 times” the “minimum profitable production cost.” This is in a market stretching across five counties, with ample suitable land, nearly all of it off-limits to development.

There is need for reform, and we cite Paul Cheshire, Max Nathan and Henry Overman of the London School of Economics who suggest that urban planning should focus on “people rather than places.” Part of the solution, according to former World Bank principal planner Alain Bertaud, is to apply “basic economic principles to the practice of urban planning.”

Hites Ahir: How does the findings of this editions compare to the past editions?

Wendell Cox: We have reported on the commitments made by New Zealand’s Labour government to make major land use policy revisions to restore housing affordability and establish effective infrastructure finance mechanisms.

We have also focused on subsidized low-income housing and the extent to which its cost and availability is driven by market housing costs. Because housing subsidies are typically based on ability to pay, deteriorating housing affordability compromises the ability of government to provide for low income housing.

Hites Ahir: In the current issue of the survey, you talk about Singapore. Could you talk to us about “Singapore’s unequalled housing challenge”?

Wendell Cox: Singapore is a city-state confined to an island that has virtually no hinterland in which inexpensive housing development can occur. Yet this topographically contained market has housing affordability considerably better than many markets that have administratively imposed urban containment.

Singapore designed a market that kept house price increases under control, despite the shortage of land. It started with a commitment, more than a half-century ago, to “(…) encourage a property-owning democracy in Singapore and to enable Singapore citizens in the lower middle-income group to own their own homes.” The mandate was assigned to the Housing Development Board (HDB) which has delivered on the objective.

Singapore’s model for the world is not so much the characteristics of its market, as it is having adopted a fundamental objective of housing affordability and focusing on its achievement.

Hites Ahir: How is the ongoing crisis related to Covid-19 likely to affect next year’s survey?

Wendell Cox: Obviously, the economic decline from the lockdowns will make things worse, and probably more for the middle-income households we focus on. Lower-income households are likely to be impacted even more. Housing affordability seems more likely to worsen than to stay the same or improve.

Global Housing Watch Newsletter: April 2020

*In this interview, Wendell Cox talks about Demographia’s latest housing affordability . Wendell Cox is an American urban policy analyst and academic. He is the principal of Demographia (Wendell Cox Consultancy). The survey is co-authored with Hugh Pavletich of Performance Urban Planning.

Hites Ahir: You recently released the 16th Annual Demographia International Housing Affordability Survey: 2020.

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, April 17, 2020

Housing View – April 17, 2020

On the US:

- Coronavirus is squeezing more people out of the housing market – Axios

- Fed’s Housing-Market Concerns Increase Pressure to Help Mortgage Firms – Wall Street Journal

- Another U.S.-Wide Housing Slump Is Coming – Bloomberg

- Making a Home That’s Affordable, for Good – Citylab

- Despite Stay-at-Home Order, Seattle’s Real-Estate Market Continues to Show Up – Wall Street Journal

- Rental Market Likely Headed for a Slowdown – Harvard Joint Center for Housing Studies

- America’s Housing Finance System in the Pandemic, Part 3: Q&A on the Ugly Fight over Servicer Advances – Harvard Joint Center for Housing Studies

- Housing policy should stop creating competition between young and old – The Hill

On other countries:

- [Germany] The German housing market cycle: Answers to FAQs – Bundesbank

- [United Arab Emirates] Property prices in UAE continues to drop – Global Property Guide

- [United Kingdom] What is the outlook for the UK housing market? – Financial Times

On the US:

- Coronavirus is squeezing more people out of the housing market – Axios

- Fed’s Housing-Market Concerns Increase Pressure to Help Mortgage Firms – Wall Street Journal

- Another U.S.-Wide Housing Slump Is Coming – Bloomberg

- Making a Home That’s Affordable, for Good – Citylab

- Despite Stay-at-Home Order, Seattle’s Real-Estate Market Continues to Show Up – Wall Street Journal

- Rental Market Likely Headed for a Slowdown – Harvard Joint Center for Housing Studies

- America’s Housing Finance System in the Pandemic,

Posted by at 5:00 AM

Labels: Global Housing Watch

Wednesday, April 15, 2020

The German housing market cycle: Answers to FAQs

From a new paper by the Bundesbank:

“Research Question

Frequently asked questions in the analysis of housing markets are: What are the effects of interest rates, income or housing supply on house prices? What is the impact of house price increases on the supply of housing? How much is housing inflation due to land price increases and what is the contribution of construction prices? How long do house price fluctuations last? This paper seeks to shed light on the joint price and supply responses on the German housing market to exogenous changes in macroeconomic determinants.

Contribution

Computing typical reactions of price and supply on the housing market across different episodes of the house price cycle requires a long time series for house prices. The paper presents a novel aggregate price index for housing in Germany, which goes back to 1993. The long house price series, which can be split into a land and a construction price component, is incorporated in an econometric model that takes into account the interaction between the price and supply of housing.

Results

Estimation results suggest that house prices in Germany mainly depend on current and expected income and on the level of interest rates. A decomposition suggests that land prices react more strongly to interest rate changes and to current income developments, whereas for construction prices expected income and the level of construction activity appear to play a larger role. While in the years before the Great Recession, construction prices contributed most to house price growth, land price growth was the main driver behind the recent strong house price increases. The estimates point to a moderate housing supply elasticity in international comparison. The house price dampening effect of additional housing supply is found to be small. This is the result of the combination of a positive price effect of additional construction via construction prices and a price dampening effect of additional building land. Finally, house prices and residential investment take several years to adjust to shocks.”

From a new paper by the Bundesbank:

“Research Question

Frequently asked questions in the analysis of housing markets are: What are the effects of interest rates, income or housing supply on house prices? What is the impact of house price increases on the supply of housing? How much is housing inflation due to land price increases and what is the contribution of construction prices? How long do house price fluctuations last?

Posted by at 8:36 AM

Labels: Global Housing Watch

Monday, April 13, 2020

Sneak Preview of COVID-19 Impact on U.S. Job Market

Three leading economists have used a new data set to offer a sneak preview of the impact that COVID-19 has had on the U.S. job market. They estimate that:

“First, job loss has been significantly larger than implied by new unemployment claims: we estimate 20 million lost jobs by April 8th, far more than jobs lost over the entire Great Recession.

Second, many of those losing jobs are not actively looking to find new ones. As a result, we estimate the rise in the unemployment rate over the corresponding period to be surprisingly small, only about 2 percentage points.

Third, participation in the labor force has declined by 7 percentage points, an unparalleled fall that dwarfs the three percentage point cumulative decline that occurred from 2008 to 2016. Early retirement almost fully explains the drop in labor force participation both for those survey participants previously employed and those previously looking for work.”

The paper is by Coibion, Gorodnichenko and Weber.

Three leading economists have used a new data set to offer a sneak preview of the impact that COVID-19 has had on the U.S. job market. They estimate that:

“First, job loss has been significantly larger than implied by new unemployment claims: we estimate 20 million lost jobs by April 8th, far more than jobs lost over the entire Great Recession.

Second, many of those losing jobs are not actively looking to find new ones.

Posted by at 4:40 PM

Labels: Inclusive Growth

Subscribe to: Posts