Thursday, July 22, 2021

Housing Market in Estonia

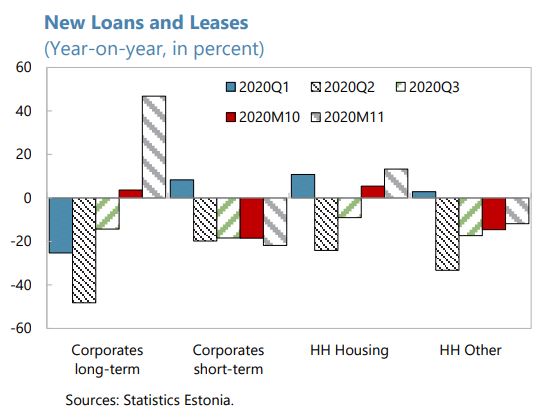

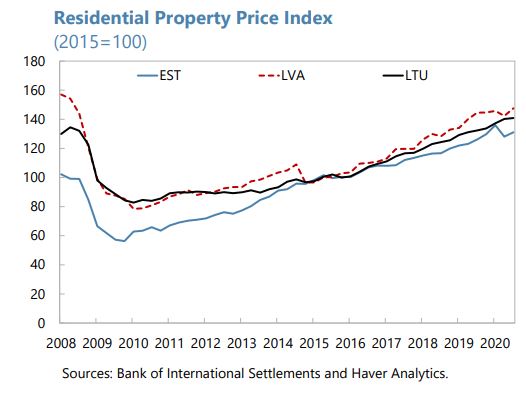

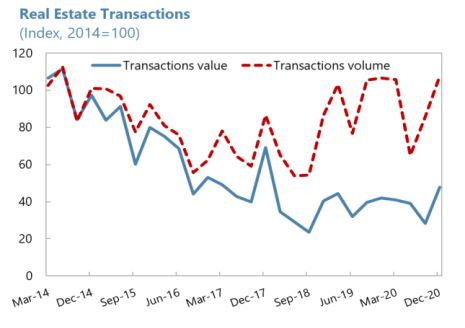

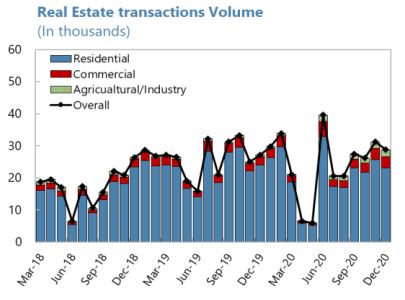

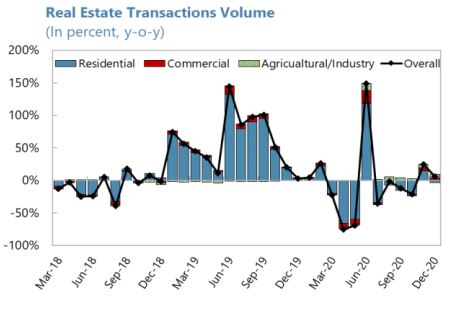

From the IMF’s latest report on Estonia:

“Housing market and macroprudential policy. Although the housing market has weathered the crisis well, it is critical as a preventive policy tool that the standard macroprudential instruments (debt to income, loan-to-value, and loan maturity cap requirements and the 15 percent risk weight for mortgage loans), be maintained to help keep the housing prices aligned with fundamentals. The authorities should be ready to re-calibrate tools in light of the risks of housing market overheating that are posed by the pension system withdrawals. As the economy recovers, the systemic risk and countercyclical capital buffers (both currently at zero) could be re-assessed and macroprudential tools may need to be used more actively if significant divergences with the euro-area’s cyclical conditions emerge.”

From the IMF’s latest report on Estonia:

“Housing market and macroprudential policy. Although the housing market has weathered the crisis well, it is critical as a preventive policy tool that the standard macroprudential instruments (debt to income, loan-to-value, and loan maturity cap requirements and the 15 percent risk weight for mortgage loans), be maintained to help keep the housing prices aligned with fundamentals. The authorities should be ready to re-calibrate tools in light of the risks of housing market overheating that are posed by the pension system withdrawals.

Posted by at 3:13 PM

Labels: Global Housing Watch

Monday, July 19, 2021

Housing Market in Germany

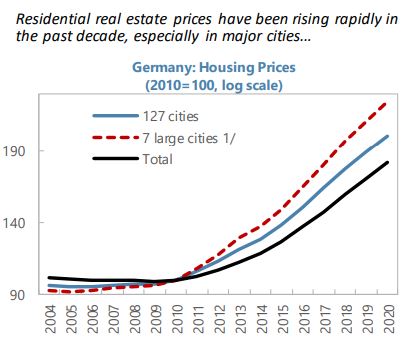

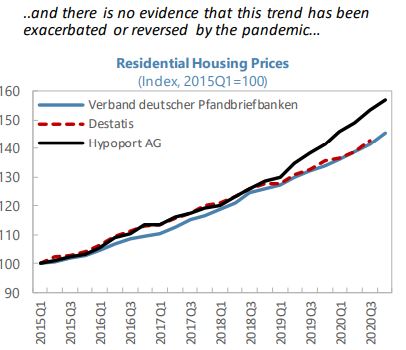

From the IMF’s latest report on Germany:

“Vulnerabilities in real estate markets call for close monitoring and addressing remaining data gaps. The COVID-19 pandemic has elevated risks related to the real estate market, which was marked by significant price increases in the years prior to the crisis. Commercial Real Estate (CRE) remains susceptible to lower demand following behavioral changes engendered by the pandemic, increasing vulnerabilities of German banks which are among Europe’s most exposed to CRE. Residential real estate prices have been rising rapidly over the past decade, especially in major cities (…). However, there is little evidence that this trend has been either exacerbated or reversed by the pandemic. Although household indebtedness remains relatively low, the continued build-up of vulnerabilities in real estate lending warrants close monitoring. The lack of granular data—which hinders a full assessment of potential risks to financial stability—should be quickly remedied. The authorities took an important step in this direction recently, providing a legal framework for the Bundesbank for more comprehensive data collection on residential real estate loans. An assessment of the adequacy of supervisory data should be conducted following initial data collection, and any remaining gaps promptly closed. Germany should also expand its macroprudential toolkit for real estate lending, including income-based instruments such as debt-to-income or debt-service-to-income caps, while recognizing that the CRE sector is characterized by considerable heterogeneity in financing structures.”

From the IMF’s latest report on Germany:

“Vulnerabilities in real estate markets call for close monitoring and addressing remaining data gaps. The COVID-19 pandemic has elevated risks related to the real estate market, which was marked by significant price increases in the years prior to the crisis. Commercial Real Estate (CRE) remains susceptible to lower demand following behavioral changes engendered by the pandemic, increasing vulnerabilities of German banks which are among Europe’s most exposed to CRE.

Posted by at 3:30 PM

Labels: Global Housing Watch

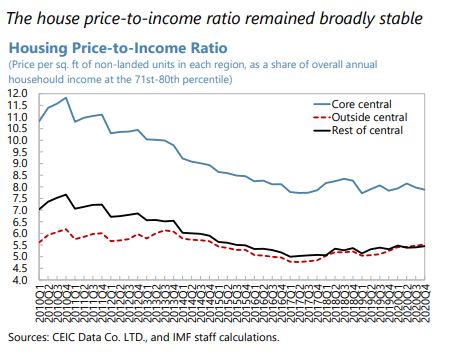

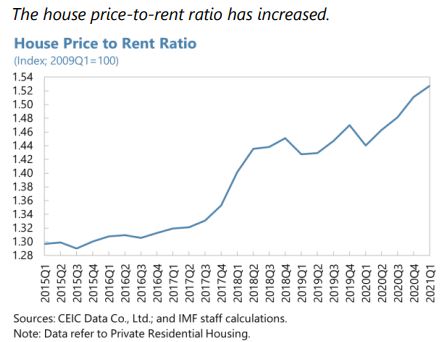

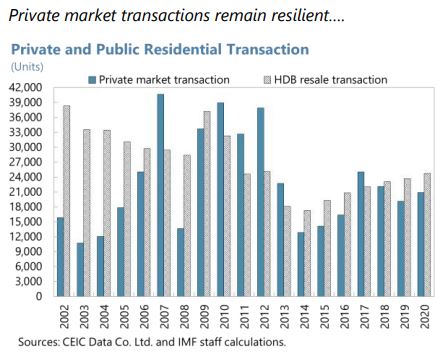

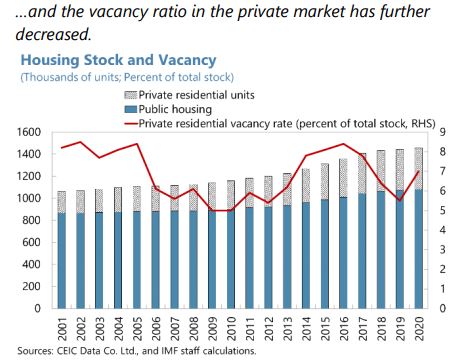

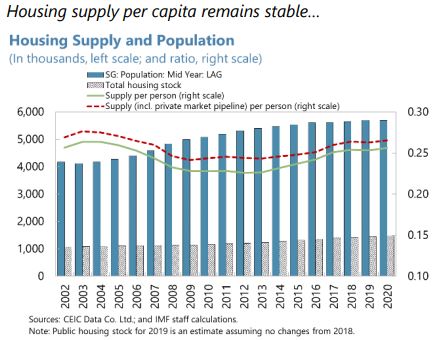

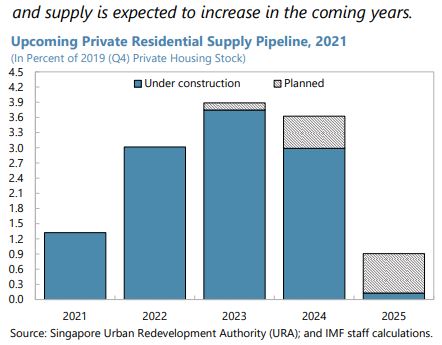

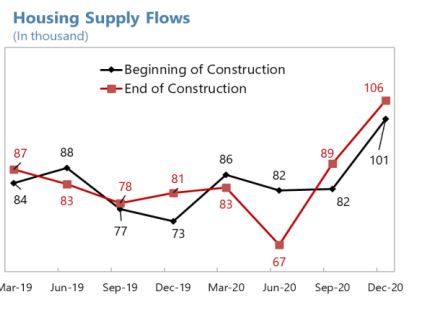

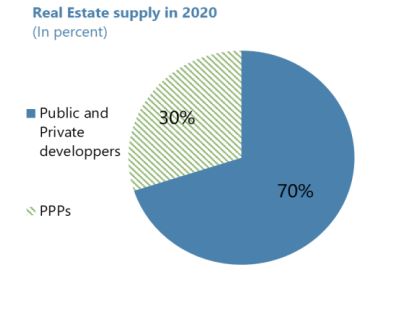

Housing Market in Singapore

From the IMF’s latest report on Singapore:

“The housing market has been stable during the pandemic, while the commercial real estate market has been more adversely impacted. Private house prices and transactions have held up; following a 2.2 percent increase in 2020, house prices further increased by 6.6 percent in 2021Q1 (year-on-year), while household mortgage loan NPLs remained stable at ½ percent of the bank’s mortgage book in 2020 (…). The economic downturn, however, has reduced demand for commercial space, and by end-2021Q1 prices for office and retail space had declined by 9.5 percent and 4.6 percent respectively. Vacancy rates for retail space edged up from 8.0 percent in 2020Q1 to 8.5 percent in 2021Q1, and for office space from 11.0 percent to 11.9 percent during the same period, although these have come down from peak levels in 2020.”

From the IMF’s latest report on Singapore:

“The housing market has been stable during the pandemic, while the commercial real estate market has been more adversely impacted. Private house prices and transactions have held up; following a 2.2 percent increase in 2020, house prices further increased by 6.6 percent in 2021Q1 (year-on-year), while household mortgage loan NPLs remained stable at ½ percent of the bank’s mortgage book in 2020 (…). The economic downturn,

Posted by at 3:19 PM

Labels: Global Housing Watch

Friday, July 9, 2021

Housing Market in Saudi Arabia

From the IMF’s latest report on Saudi Arabia:

“Mortgage lending has continued to grow rapidly as government programs have supported housing demand and supply (…). Retail mortgage lending has more than doubled over the past two years to around 18 percent of total bank credit. SAMA and staff agreed that risks to banks still appear limited given debt service limits on borrowers, the low average loan-to-value ratio, and the fact that most repayments are made by salary assignment from borrowers employed in the public sector. Nevertheless, risks need to be carefully monitored and SAMA stressed that they carefully monitor banks and have surveillance systems in place to identify any build-up of vulnerabilities to inform macroprudential policy.”

From the IMF’s latest report on Saudi Arabia:

“Mortgage lending has continued to grow rapidly as government programs have supported housing demand and supply (…). Retail mortgage lending has more than doubled over the past two years to around 18 percent of total bank credit. SAMA and staff agreed that risks to banks still appear limited given debt service limits on borrowers, the low average loan-to-value ratio, and the fact that most repayments are made by salary assignment from borrowers employed in the public sector.

Posted by at 3:48 PM

Labels: Global Housing Watch

Subscribe to: Posts