Friday, January 30, 2015

House Prices in Canada

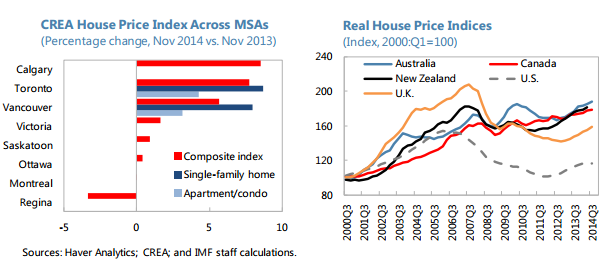

“Housing markets strong with signs of overvaluation to differing degrees. After a brief pause, Canada’s housing market rebounded in 2014, fueled by low and declining interest rates (…). House prices have been rising at 5–6 percent (y/y) nominally through most of 2014 (almost twice the average pace in 2013). Most of the appreciation has been driven by Calgary’s housing market and single-family homes in Toronto and Vancouver (…). Since 2001, house prices have risen significantly—similar to other Commonwealth commodity-exporter countries— though Canada’s cycle seems to be lagging and relatively smoother. Read the full article…

Posted by at 9:42 PM

Labels: Global Housing Watch

Thursday, January 29, 2015

House Prices in Ireland

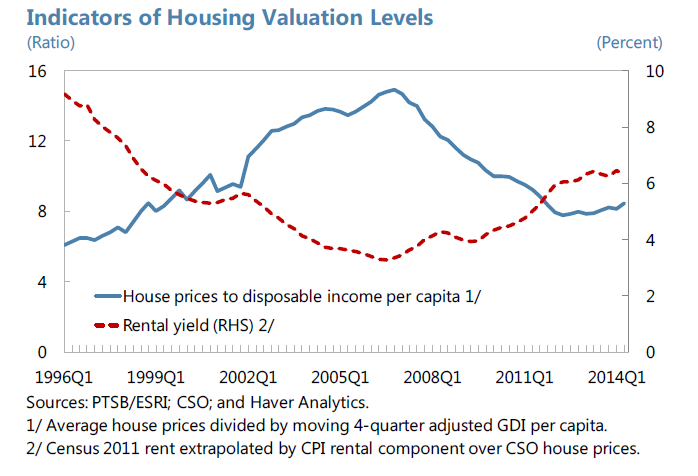

“Property values are up sharply, though valuation risks are not yet evident, and mortgage lending is beginning to rise from a low base. National housing prices rose 16.3 percent y/y in October, with Dublin prices surging 24.2 percent y/y, though they remain 38 percent below their pre crisis peak. New mortgage loans grew about 50 percent y/y in Q3 2014, from a low base, with about half of all residential property transactions in cash. Residential rents are also rising, and house price ratios to rents and incomes do not yet signal valuation concerns. Read the full article…

Posted by at 11:12 PM

Labels: Global Housing Watch

Tuesday, January 20, 2015

State of Housing Markets Across the Globe

Here is my presentation on the IMF’s Global Housing Watch and the state of housing markets across the globe that I gave at the International Housing Association Conference. Also, see country specific presentations that were given by other participants at the conference: Australia, Canada, Japan, Nigeria, Norway, and the United States. And here is the link to the agenda. Read the full article…

Posted by at 3:24 AM

Labels: Global Housing Watch

Wednesday, January 14, 2015

Global Joblessness Returns To Precrisis Levels In New IMF Employment Gauge

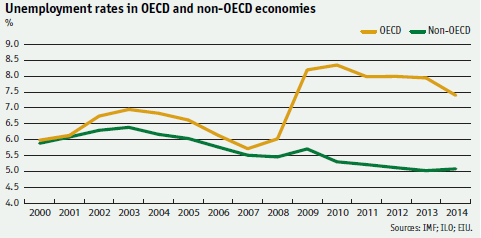

Global unemployment is finally back to levels seen before the global financial crisis. But the recession has left a sharp divergence between advanced and emerging economies, according to a new gauge unveiled by the International Monetary Fund.

The world’s jobless rate ended 2014 at 5.6%, where it stood in 2007. But global employment is growing at just 1.5% a year, far slower than the 2% to 2.5% growth rate seen before the crisis.

The figures are from a new Global Jobs Index by the IMF and the Economist Intelligence Unit. The index, the first worldwide gauge of its kind, will offer quarterly estimates based on employment in 64 economies that represent about 95% of the world’s economic output and 80% of its labor force. (Some jobs numbers are drawn from historical relationships between jobs and economic growth.)

The world’s top policy makers, convening through the G-20 and the IMF, have long used overall economic growth measures to assess their progress. But they often note that jobs are the key measure of their success. The latest gauge shows one way they’re struggling. Top-line measures such as unemployment are returning to normal levels in many nations, including the U.S., but overall employment growth remains sluggish.

“The index can be used to take the pulse of global labor markets at more regular intervals than has been done before,” IMF economist Prakash Loungani wrote. “While financial markets are monitored second-by-second, data on jobs—which matters more to most people—are often not available every quarter because many countries do not report employment numbers in a timely manner.”

The new report shows a striking divergence between advanced and emerging economies. Unemployment in advanced economies–members of the Organization for Economic Cooperation and Development–stood at 7.4% in 2014, far higher than the 5.7% seen in 2007. The eurozone is largely responsible for that elevated level, with most economies other than Germany struggling to regain ground.

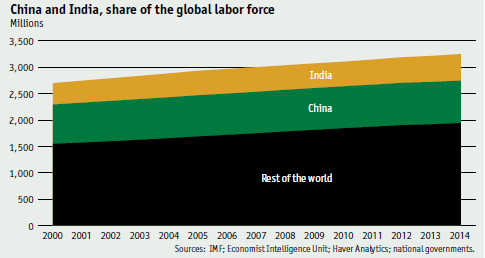

Emerging markets have generally fared better on the employment front, at least according to official measures. But the report notes that official gauges for China and India, which together account for 40% of the global labor force, are widely seen as too low. Substituting a measure of joblessness for those countries from the private Economist Intelligence Unit would put the global unemployment rate in 2014 just above 7%.

From the Wall Street Journal:

Global unemployment is finally back to levels seen before the global financial crisis. But the recession has left a sharp divergence between advanced and emerging economies, according to a new gauge unveiled by the International Monetary Fund.

The world’s jobless rate ended 2014 at 5.6%, where it stood in 2007. But global employment is growing at just 1.5% a year, far slower than the 2% to 2.5% growth rate seen before the crisis.

Posted by at 9:58 PM

Labels: Inclusive Growth

Wednesday, January 7, 2015

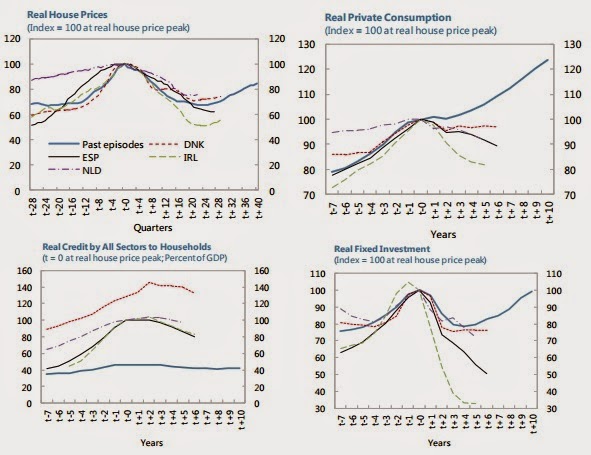

Housing Recoveries: Denmark, Ireland, Netherlands and Spain

Also, read an iMFdirect blog post on the report here.

A new report by the IMF “(…) examines the experiences of Denmark, Ireland, the Netherlands, and Spain—four countries in which the house-price cycle has been especially large and that share a similar institutional environment (a common monetary policy and the EU’s institutional framework)—with a view to exploring how policies can best support economic recovery in the wake of a house-price bust. (…) These countries’ experiences share similarities, but also important differences. Shocks to house prices, unemployment, Read the full article…

Posted by at 7:27 PM

Labels: Global Housing Watch

Subscribe to: Posts