Saturday, June 30, 2018

Housing: Is This Time Different?

The IMF’s latest report on Ireland says that:

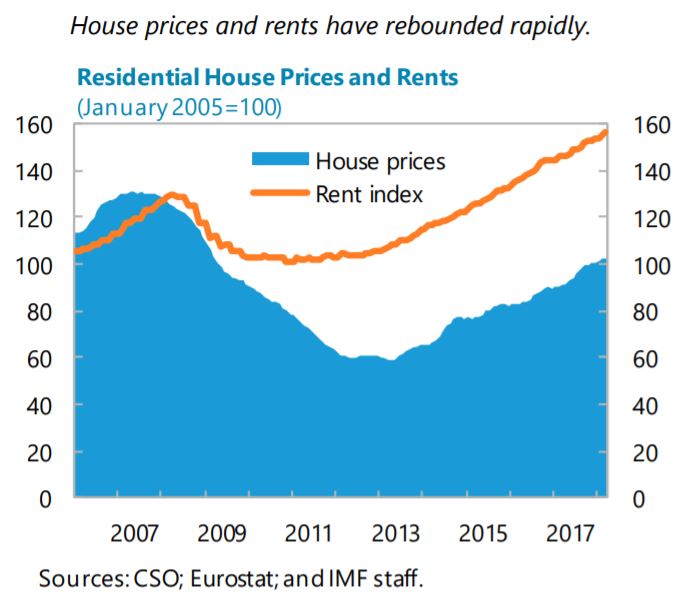

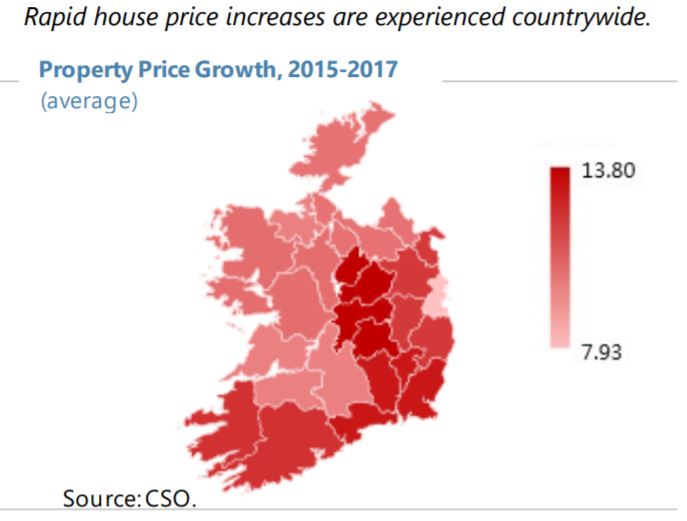

“As in the run-up to the crisis, the ongoing strong economic momentum is accompanied by a surge in house prices and rents. While house prices remain well below the pre-crisis peak, they have rebounded rapidly in Dublin and other regions, posting an average annual increase of 13 percent in March 2018. Rents have also increased at a strong pace (6 percent as of

end-2017) and surpassed their pre-crisis level.Unlike in the pre-crisis period, house prices are fueled by a persistent supply shortfall

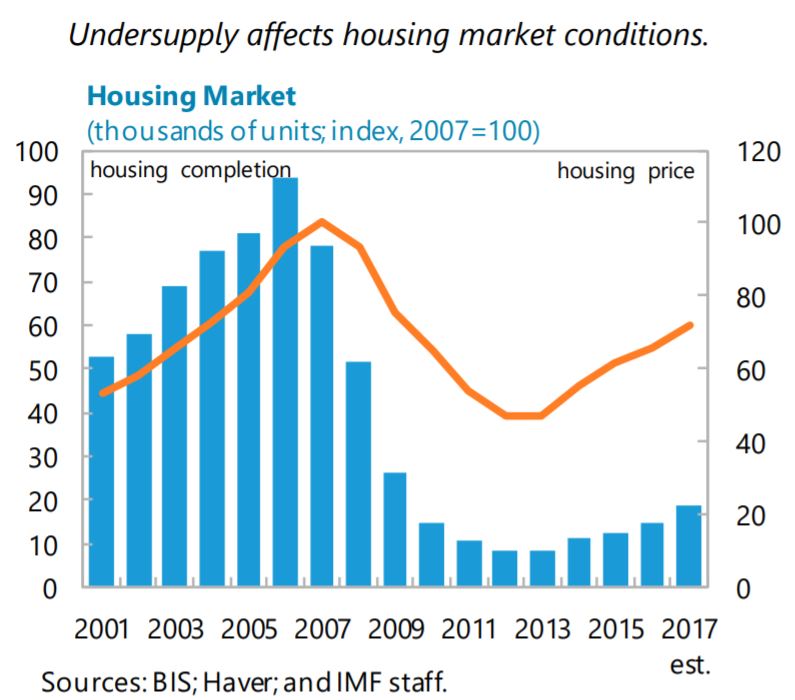

rather than by bank credit. Housing demand has recovered strongly, reflecting improved labor market conditions, rising incomes, and low interest rates. While mortgage drawdowns and approvals have rapidly increased, albeit from a low base, cash transactions remain relevant. In contrast, the recovery of the housing supply has been modest so far, with house completions falling well below the estimated underlying demand of about 35,000 units per year. The government has taken several measures to help boost supply (…) but these will need time to have an impact. High building costs, impaired balance sheets of construction firms and related funding difficulties, skill shortages, and land hoarding are the main factors holding back supply. In CRE properties, high yield attracted strong investment, largely from abroad, alleviating financing constraints and resulting in a fast supply response. Returns have moderated to levels seen in peers, after years of strong gains.While house prices are not significantly misaligned, upward pressure is likely to persist. Price-to-income and priceto-rent ratios have steadily increased in recent years and at present modestly exceed their historical average. However, model-based measures of house price misalignment are inconclusive with results ranging from some undervaluation (ESRI) to a small overvaluation. While there are no immediate financial stability risks, house price pressures are likely to persist over the medium term, as demand growth is

likely to continue outpacing supply.Against this backdrop, priority should be given to encourage greater housing supply…

- Further rationalization of building regulations and streamlining of planning processes are warranted. Reducing skills gaps in the construction sector, advancing debt restructuring of distressed but viable construction firms, and improving their access to financing are important.

- The establishment of the HBFI could provide funding to financially-constrained developers in the residential market. However, its operations should remain limited in scope and subject to prudent risk assessment and a robust governance structure to minimize risks for public finances.

- With a view to reducing land hoarding, a vacant site levy will be introduced starting

in 2019. However, its rates (3 percent for the first year and 7 percent for the second

and subsequent years) should be reviewed periodically to ensure effectiveness.

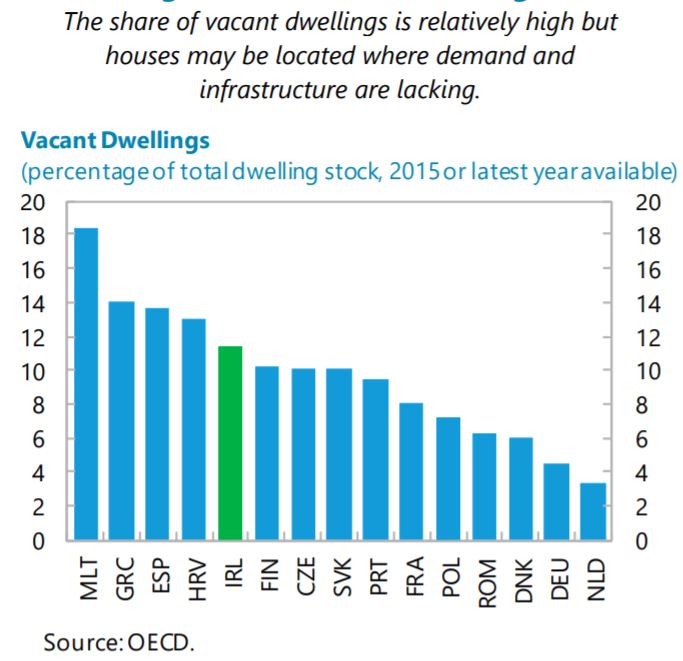

- Ireland has a high level of vacant dwellings, though some of these are located in areas

where demand and infrastructure are lacking. To ensure greater utilization of these properties, consideration should be given to adopting a surcharge on properties that are left vacant in urban areas.…while enacted measures to improve housing affordability need to be well-targeted…

- There is scope to re-calibrate the Help-to-Buy scheme, which provides a tax rebate of up to 5 percent of the dwelling purchase price for FTBs, towards low-income households.

- Measures to stabilize rents should be reconsidered as they may deter new construction. Support for disadvantaged groups should be delivered through well-targeted housing assistance payments.

- The RIHL, which provides loans to risky borrowers outside the banking system, should remain of limited scope and subject to stringent risk assessment to safeguard financial stability, particularly because the use of the RIHL might breach the central bank’s loan-to-income (LTI) limits.

…and macroprudential policy should continue to be deployed proactively. Following

last November’s review of mortgage measures, the central bank has kept the core parameters of the macroprudential framework intact, while halving the proportion of new non-FTB loans allowed to exceed the 3.5 LTI limit to 10 percent. Although currently appropriate, it is crucial that the macroprudential limits are adjusted pre-emptively to ensure that bank and household balance sheets remain resilient to shocks. In addition, as the Central Credit Registry becomes operational in 2018, staff encourages the authorities to shift from a LTI to a debt-to-income limit, which better captures household repayment capacity, once comprehensive data on household debt are available.”

Posted by at 6:48 AM

Labels: Global Housing Watch

Subscribe to: Posts