Tuesday, May 31, 2022

Who Killed the Phillips Curve? A Murder Mystery

From a new working paper by David Ratner and Jae Sim:

“Is the Phillips curve dead? If so, who killed it? Conventional wisdom has it that the sound monetary policy since the 1980s not only conquered the Great Inflation, but also buried the Phillips curve itself. This paper provides an alternative explanation: labor market policies that have eroded worker bargaining power might have been the source of the demise of the Phillips curve. We develop what we call the “Kaleckian Phillips curve”, the slope of which is determined by the bargaining power of trade unions. We show that a nearly 90 percent reduction in inflation volatility is possible even without any changes in monetary policy when the economy transitions from equal shares of power between workers and firms to a new balance in which firms dominate. In addition, we show that the decline of trade union power reduces the share of monopoly rents appropriated by workers, and thus helps explain the secular decline of labor share, and the rise of profit share. We provide time series and cross sectional evidence.”

From a new working paper by David Ratner and Jae Sim:

“Is the Phillips curve dead? If so, who killed it? Conventional wisdom has it that the sound monetary policy since the 1980s not only conquered the Great Inflation, but also buried the Phillips curve itself. This paper provides an alternative explanation: labor market policies that have eroded worker bargaining power might have been the source of the demise of the Phillips curve.

Posted by at 10:34 AM

Labels: Macro Demystified

Friday, May 27, 2022

Housing View – May 27, 2022

On cross-country:

- Drivers of rising house prices and the risk of reversal – European Central Bank

- ECB warns a house price correction is looming as interest rates rise. Central bank says housing market reversal would hit low-income homes harder – FT

- Euro zone’s overpriced housing market may sag if rates rise, ECB says – Reuters

- Has COVID-19 Triggered an Urban Exodus? – OECD

- Asia’s advanced economies now have lower birth rates than Japan. The cost of housing may be the biggest factor – The Economist

- Housing policy and affordable housing – LSE

- Revisiting International House Price Convergence Using House Price Level Data – IDEAS

- Housing and the Labor Market – Oxford Research Encyclopedias

On the US:

- Conference: Housing & Urban Economics on September 7 – Stanford University

- Rising Interest Rates Concern Apartment-Building Owners, Renters. Returns fall below mortgage figures, with landlords needing higher rents to fill the gap – Wall Street Journal

- Housing Boom Is on Borrowed Time. Higher rates have only just begun to weigh on home sales and prices – Wall Street Journal

- The housing market boom has at least another year to run, Zillow economists predict – Fortune

- Fed Searches for the Magic Number to Cool a Red-Hot U.S. Housing Market. The central bank must decide on an interest rate that will cap sky-high price growth without triggering a painful economic slowdown – Wall Street Journal

- How Homeowners Can Lock in the Steep Rise in Home Values. For those who don’t want to sell, there are strategies to use to hedge against a future decline – Wall Street Journal

- In Battle for Workers, Companies Build Houses. Disney, meatpacker JBS and others launch plans to add affordable housing near job sites; a Vail, Colo., project draws opposition – Wall Street Journal

- April Rental Report: Sun Belt Metros Drive Sustained Growth in Nationwide Rents – Realtor

- Housing in America has become much harder to afford. High prices and soaring mortgage rates are putting some buyers off – The Economist

- Did the pandemic advance new suburbanization? – Brookings

- Effective Zoning Reform Isn’t as Simple as It Seems. The Biden administration’s housing plan will reward cities that change their land-use policies to promote density. But what kind of zoning reforms really work? – Bloomberg

- Fed Liquidity Facility Successfully Anchored Commercial Real Estate amid Pandemic – Dallas Fed

- Biden is doubling down on dense, affordable housing – Quartz

- Pandemic Housing Boom Hits a Wall With US Buyers Priced Out. Home values in the Sun Belt boomtowns spiked, but now rising mortgage rates, inflation, and recession fears are starting to pinch. – Bloomberg

- Amid a Housing Crunch, Homes Pop Up on the Fairway. With large expanses of grass and trees, former golf courses are being reconsidered for housing, but developers face challenges, including community resistance. – New York Times

- Housing and Access to Credit Are Two Sides of the Financial Inclusion Coin – San Francisco Fed

- The Household Mystery: Part II – Calculated Risk

- Wall Street’s housing grab continues. As rising rates deter families from buying, being a rentier looks as appealing as ever – The Economist

- US house prices never go down. I mean, they don’t, right? – FT

- Dissecting Housing Supply And Demand: Macro Man Podcast. Bloomberg’s Cameron Crise compares the current state of the housing market with the 2006 bubble peak and its aftermath. – Bloomberg

On China

- China cuts mortgage lending rate by record as lockdowns hit economy. Five-year loan prime rate slashed by most since before pandemic as government steps up stimulus – FT

- China’s property market woes expected to worsen in 2022, Reuters poll shows – Reuters

- China property market slumps on developers’ debt crisis, weak buyer sentiment – Reuters

- China’s Real Estate Slump: Underlying Issues. Although the current approach will ease some major indicators, such as property sales and prices, they will not necessarily resolve the core issues. – The Diplomat

On other countries:

- [Australia] Housing in the Endemic Phase – Reserve Bank of Australia

- [Australia] Australia’s housing boom to deflate as mortgage rates rise – Reuters

- [Canada] One of the World’s Frothiest Housing Markets Turned Into a Seller’s Headache Overnight. House hunters from Toronto to small Ontario suburbs are changing how they navigate the tight housing landscape with interest rates heading higher. – Bloomberg

- [Canada] How much will Canada’s block on foreign buyers help its housing crisis? – NPR

- [Hong Kong] New Hong Kong Leader’s Vow to Fix Housing Crisis Draws Skeptics. John Lee will focus on national security in wake of protests. Lack of policy, business experience could also hamper ability – Bloomberg

- [New Zealand] New Zealand banks predict 20% drop in house prices over next year. Economists say tighter credit conditions, higher mortgage rates and increased housing supply behind sinking prices – The Guardian

- [United Kingdom] Nationwide warns inflation surge will hit house prices. Profits double at UK’s largest building society on back of mortgage growth and higher interest margins – FT

- [United Kingdom] Slowdown ahead for UK housing market. Gap between equity-rich house owners and first-time buyers set to widen as cost of living crisis hits – FT

- [United Kingdom] Bridging loans surge as UK buyers scramble for property. Brokers urge caution in volatile market – FT

On cross-country:

- Drivers of rising house prices and the risk of reversal – European Central Bank

- ECB warns a house price correction is looming as interest rates rise. Central bank says housing market reversal would hit low-income homes harder – FT

- Euro zone’s overpriced housing market may sag if rates rise, ECB says – Reuters

- Has COVID-19 Triggered an Urban Exodus?

Posted by at 5:00 AM

Labels: Global Housing Watch

Wednesday, May 25, 2022

Housing Market in Europe

From the European Central Bank:

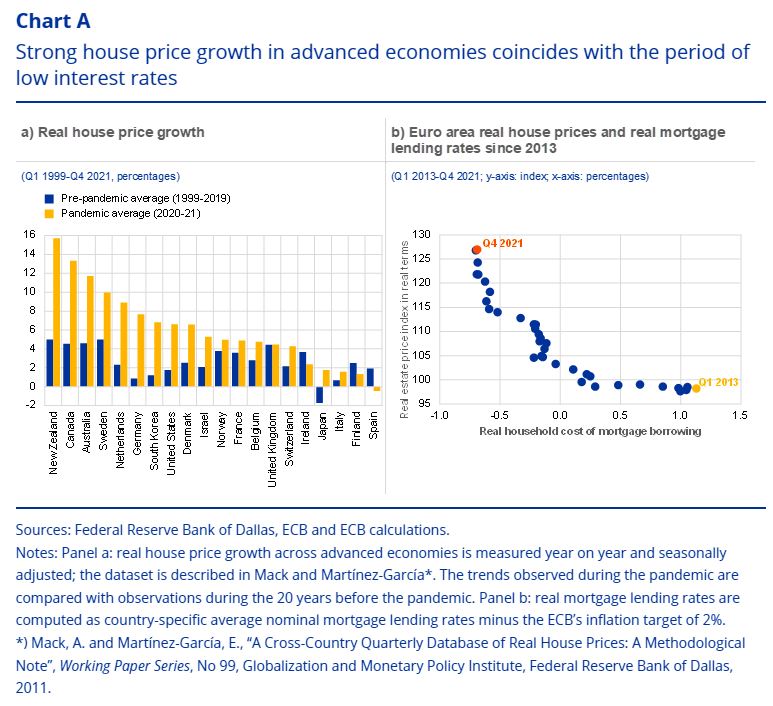

“House prices increased substantially during the pandemic, fuelling concerns about possible price reversals and their implications for financial stability. In many advanced economies, real house price growth exceeded 4% during the pandemic (Chart A, panel a), reaching 4.3% in the euro area in the fourth quarter of 2021[1] amid signs of exuberance in some countries.[2] At the same time, real mortgage lending rates in the euro area have fallen further to reach historic lows in the current low interest rate environment (Chart A, panel b).[3] Against this backdrop, this box discusses the main drivers of recent house price increases across advanced economies and in the euro area, and the associated risks of possible price reversals and the potential implications for financial stability.

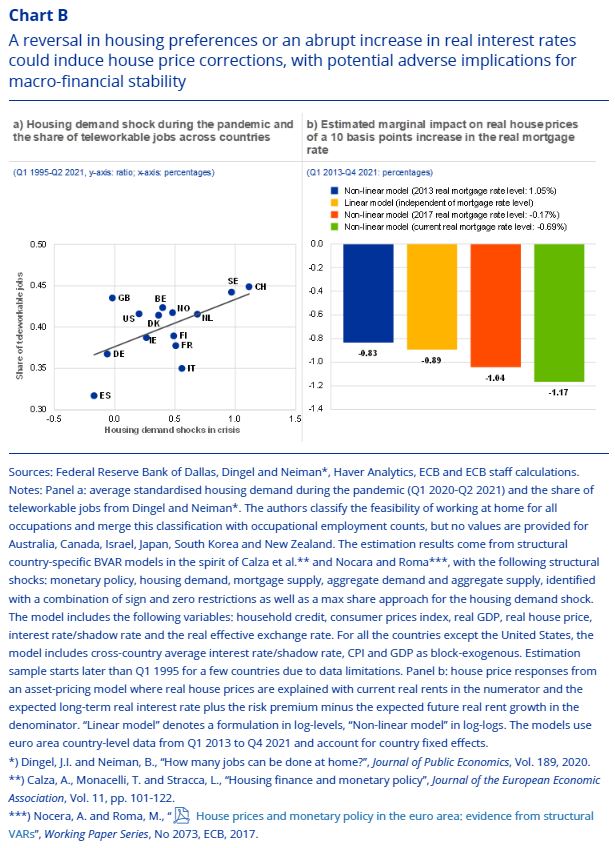

Shifts in housing preferences and low interest rates have been important drivers of recent strong house price growth across advanced economies. Estimates based on country-specific Bayesian vector autoregression (BVAR) models indicate that the house price increases across advanced economies during 2020-21 were mainly driven by increased demand for housing. There is a positive correlation between the magnitude of the estimated housing demand shock across countries and the share of teleworkable jobs, signalling that the housing demand shocks are related to a shift in housing preferences during the pandemic (Chart B, panel a), possibly reflecting a desire for more space coupled with less need for commuting.[4] Increased demand for housing could also be related to search-for-yield behaviour in the low-yield environment. In addition, monetary policy shocks combined with mortgage supply shocks contributed to the recent house price increases across advanced economies, including the euro area. Unlike housing demand shocks, monetary policy and mortgage supply shocks move interest rates and house prices in opposite directions.

In the current low interest rate environment, increased sensitivity of house price growth to changes in real interest rates makes substantial house price reversals more likely. Evidence for the euro area shows that a model with an interest rate-dependent sensitivity of real house prices to real interest rates outperforms a model with a constant sensitivity. Such a non-linear model is consistent with asset pricing theory and implies that the lower the level of the real interest rate, the larger should be the response of house prices for a given change in that rate.[5] Given the current low level of interest rates, therefore, potential reversals in residential real estate prices could be larger than several years ago, especially if interest rates increased sharply. In particular, the comparison between estimated linear and non-linear models (Chart B, panel b) for the euro area shows that the estimated house price response to a 0.1 percentage point increase in real mortgage rates from the current very low level is around 28 basis points stronger when accounting for non-linear relationships (Chart B, panel b).[6]

An abrupt repricing in the housing market – if the demand for housing were to go into reverse, for example, or real interest rates were to rise significantly – could produce spillovers to the wider financial system and economy. Such price reversals in housing markets could reflect a return to pre-pandemic work modalities or a strong increase in real interest rates. Other possible factors include a change in investor preferences for holding residential real estate assets, as well as a more general deterioration in risk sentiment related to an exacerbation of geopolitical risks or progressing climate change. The BVAR models described above indicate that a 1% drop in house prices due to a shift in housing demand could, on average across countries, generate a peak drop in real GDP of 0.2% after two years. However, the decline varies from country to country, with a fall of up to 0.9% in some advanced economies and wide uncertainty bands around these estimates. To cushion adverse financial stability implications of potential house price reversals, a tightening of macroprudential measures seems warranted in some countries, especially where strong house price growth has been accompanied by buoyant credit dynamics.[7]“

From the European Central Bank:

“House prices increased substantially during the pandemic, fuelling concerns about possible price reversals and their implications for financial stability. In many advanced economies, real house price growth exceeded 4% during the pandemic (Chart A, panel a), reaching 4.3% in the euro area in the fourth quarter of 2021[1] amid signs of exuberance in some countries.[2] At the same time,

Posted by at 11:00 AM

Labels: Global Housing Watch

Friday, May 20, 2022

Housing View – May 20, 2022

On the US:

- President Biden Announces New Actions to Ease the Burden of Housing Costs – The White House

- Biden Administration Targets Housing Supply Shortage. New regulatory moves aim to dent housing shortage of millions of U.S. homes – Wall Street Journal

- Five housing policies that wouldn’t drive up prices in Australia. If reforms to negative gearing and capital gains tax are a bridge too far, how about tackling supply? – The Guardian

- How Biden is taking action on the housing shortage – The Hill

- Biden green-lights a home-building boom. But there’s a catch. The Biden administration has a plan to fast-track housing construction. But much of it depends on Congress. – Fast Company

- U.S. housing market cooling as building permits tumble, starts fall – Reuters

- Bidding Wars Show Signs of Cooling as Mortgage Rates Bite. Fewer homes are receiving multiple offers as higher borrowing costs limit buyers, according to Redfin – Bloomberg

- These Are the Nation’s Most—and Least—Affordable Real Estate Markets – Realtor.com

- First-Time Buyers Were Undeterred by Rapid Home Price Appreciation in 2021 – New York Fed

- We’re not in a housing bubble, say Zillow economists – Fortune

- Housing Demand and Remote Work – NBER

- The Housing Market Is Cooling and 2 Other Takeaways From Real Estate Earnings – Barron’s

- How does the Consumer Price Index account for the cost of housing? – Brookings

- America still isn’t building enough homes – Quartz

On other countries:

- [Canada] Seven Slowdown in Canada’s Housing Sector Shows Risk of Higher Rates. Bank of Canada efforts to curb inflation threaten to end the country’s real-estate boom, which has been a strong driver of its economy – Wall Street Journal

- [Canada] Rate Hikes Hit Canada Housing With First Price Drop in Two Years. Sales plunge 12.6% as borrowing costs begin to rise sharply. Price declines are heaviest in smaller markets around Toronto – Bloomberg

On the US:

- President Biden Announces New Actions to Ease the Burden of Housing Costs – The White House

- Biden Administration Targets Housing Supply Shortage. New regulatory moves aim to dent housing shortage of millions of U.S. homes – Wall Street Journal

- Five housing policies that wouldn’t drive up prices in Australia. If reforms to negative gearing and capital gains tax are a bridge too far,

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, May 13, 2022

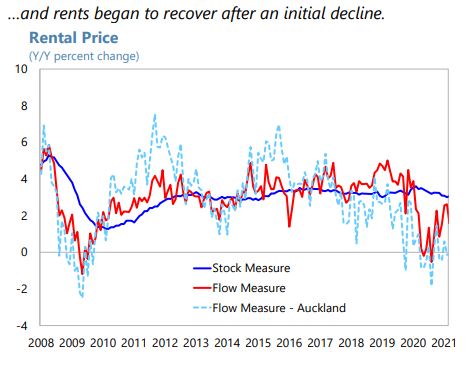

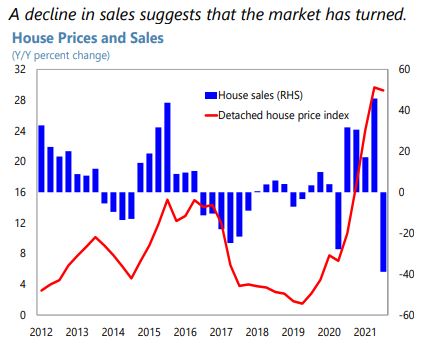

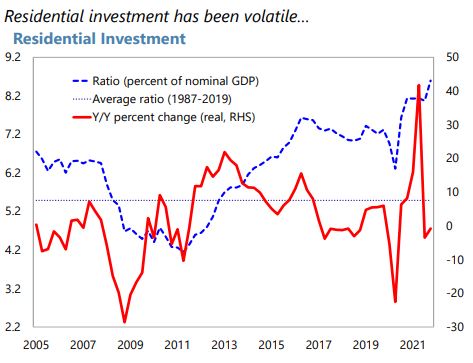

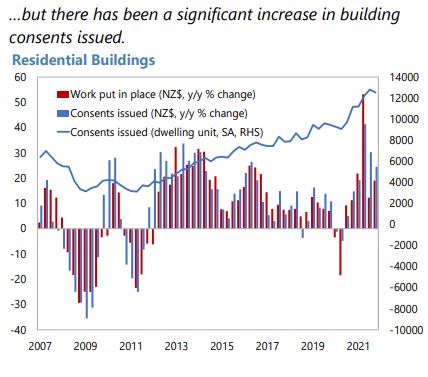

Housing Market in New Zealand

From the IMF’s latest report on New Zealand:

“House prices have peaked and are expected to correct. The market is turning given that important drivers over previous years, such as low mortgage rates and easy credit availability, are now reversing (…). The recent trend of falling sales volumes and mortgage lending is expected to continue, supporting a house price correction, although the period and intensity are difficult to estimate.

Rising mortgage rates and recent policy actions are curbing demand. In response to actual and expected withdrawal of monetary stimulus, standard mortgage rates rose by between 40 and 150 bps in 2021H2. The removal of property investors’ tax deductibility of mortgage interest and the extension of the minimum holding period to exempt capital gains on investment properties from income tax have contributed to a decline in investor demand. The RBNZ re-introduced loan-to-value ratio (LVR) limits on mortgages in March 2021 and tightened them in May and November. The December 2021 amendments to the Credit Contracts and Consumer Finance Act (CCCFA), designed to protect borrowers and strengthen the consumer credit regulatory regime, had the unintended effect of tightening credit conditions further. These developments contributed to a significant decline in mortgage lending (-31 percent y/y in March 2022), with new loans to investors and highly leveraged buyers (LVR exceeding 80 percent) declining more rapidly (-44 percent and -56 percent y/y, respectively). The RBNZ intends to implement additional MPMs for potential future use to broaden its toolkit. A framework to introduce DTI ceilings will be released by end-2022 for implementation by mid-2023. The RBNZ is also looking at the possible use of a floor on test interest rates to assess borrowers’ ability to meet debt service obligations.

Efforts are ongoing to improve housing supply. A NZ$3.8 billion (around 1.1 percent of GDP) allocation was made to the Housing Acceleration Fund to increase housing supply and improve affordability. Amendments to the Resource Management Act (RMA) in October 2021 allow for higher-density housing construction without requiring resource consent, making it easier to build new homes. However, these measures will take time to bear fruit: a cost-benefit appraisal by the Treasury estimated that about 75,000 additional dwellings would be built in the next 5-8 years, with more than 200,000 additional dwellings available in 20 years. The government is also in the process of reforming the RMA, which should streamline planning processes. There are plans to boost effective land supply by incentivizing local authorities to approve new housing projects faster.

Staff Views

Tackling housing imbalances requires a comprehensive approach, and recent initiatives will help address these imbalances. Achieving long-term housing sustainability and affordability depends critically on freeing up land supply, improving planning and zoning, and fostering infrastructure investments to enable fast-track housing developments and lower construction costs. There is a need for continued spending on land, infrastructure, and housing, including financial incentives that enable and incentivize local councils and iwi (Māori tribal organizations) to provide infrastructure for new developments. Increasing the stock of social housing also remains important in the near term, while supply constraints are addressed over time.

A moderation of prices is widely expected, and macroprudential policy should be adjusted commensurate with the evolution of financial stability risks. The use of macroprudential measures to address the financial stability impact of surging house prices has been appropriate. LVR restrictions have been effective in making lending for housing more cautious. Restrictions could be relaxed in case of a stronger-than-expected downturn in the housing market. Financial stability risks from a sharp downturn in the housing market are limited given high bank capitalization, but pockets of vulnerability, particularly among recent borrowers, may exist. More broadly, in case of a sharp downturn, potentially reinforced by a faster rise in interest rates, there could be a significant impact on consumption through wealth and confidence effects. A more extensive MPM toolkit, including the ability to readily implement DTI ceilings and loan serviceability test interest rate requirements when warranted, would be useful in addressing future risks.

Authorities’ Views

The authorities stressed that, while the housing cycle had likely turned, improving affordability remained a key priority. While prices are expected to decline in 2022, this only partially reverses the very large increases of recent years and will therefore not make a significant impact on affordability. A comprehensive approach covering the demand and supply sides of housing is underway, with more initiatives planed under the wider review of the RMA and laid out in the National Policy Statement on Urban Development. The Housing Acceleration Fund will provide funding at the local level for infrastructure development, and the first tranche of projects is likely to be approved soon. The authorities emphasized their commitment to invest in social housing. They agreed that the CCCFA amendments may have impacted credit conditions, though the effect is hard to quantify. They noted that clarifications have already been issued, with further changes being considered in consultation with the industry.”

From the IMF’s latest report on New Zealand:

“House prices have peaked and are expected to correct. The market is turning given that important drivers over previous years, such as low mortgage rates and easy credit availability, are now reversing (…). The recent trend of falling sales volumes and mortgage lending is expected to continue, supporting a house price correction, although the period and intensity are difficult to estimate.

Rising mortgage rates and recent policy actions are curbing demand.

Posted by at 6:49 PM

Labels: Global Housing Watch

Subscribe to: Posts