Thursday, September 13, 2018

Housing Market Developments in Austria

The IMF’s latest report on Austria says:

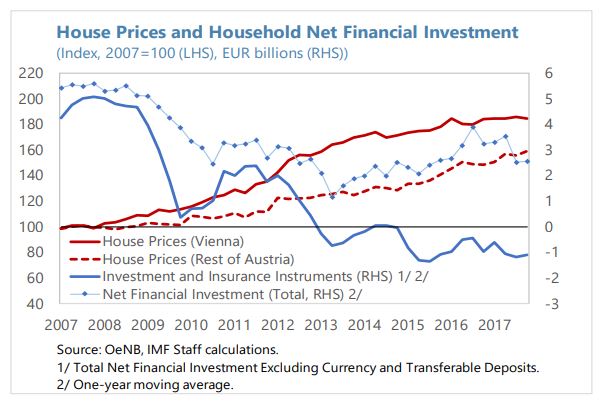

“The Austrian housing market has shown a strong trend rise in valuations over the last decade, mainly driven by price increases in Vienna. Prices stagnated through the mid-2000s

but have since outpaced most of Austria’s EU peers. In September 2016, the ESRB issued Austria a warning on medium-term residential real estate vulnerabilities because of the robust price and credit growth and the risk of further loosening in credit standards. Recently, price growth moderated to 4.7 percent (y/y) at end-2017, due to a slowdown in Vienna, though prices accelerated in the rest of the country.”

While the robust price growth has largely reflected underlying market fundamentals, the nationwide market has recently started to show signs of modest overvaluation. Housing demand has been buoyed by demographic factors, including the spike in immigration in 2015–16, and low interest rates which also have increased the attractiveness of housing assets as a form of saving. Supply-side constraints, such as land availability, have also played a role, despite some recent pickup in construction activity. The OeNB’s fundamentals indicator for residential property prices suggests a modest overvaluation of around 10 percent for Austria in 2017 (and a larger overvaluation for Vienna of about 20 percent), broadly corresponding to a range of ECB indicators as of end-2017.

Real estate related financial stability risks are nonetheless contained. The rise in mortgage debt in Austria has been modest compared to other EU countries experiencing large property price increases, and its share relative to households’ incomes has remained stable and among the lowest in the Euro Area. Residential real estate exposures account for only about a fifth of Austrian banks’ total loan stock and about 150 percent of consolidated CET-1 capital. Furthermore, the prevalence of rental accommodation (about half and three-quarters of housing nationwide and in Vienna, respectively) shield a large share of the population from adverse price developments. Less than half of homeowners have outstanding mortgages, and they also typically have higher incomes and net wealth relative to the rest of the population.

Some pockets of vulnerability and early signs of increasing risks nonetheless warrant continued close monitoring. The share of foreign exchange denominated housing loans at around

15 percent remains high relative to Austria peers, although it has declined significantly in recent years. Furthermore, the recent prolonged period of low lending rates saw a significant increase in the share of variable interest rate mortgages, which despite a recent decline still amount to about three-quarters of the total stock. There are also signs of some easing in banks’ lending standards, with a rising—albeit still limited—share of relatively high loan-to-value, debt service-to-income, and debt-to-income ratios in new housing loans to households.Supply side measures could help ease the modest price imbalances over time, while the recently expanded macroprudential toolkit can help prevent a build-up of systemic risks.

Measures to address supply-side constraints could include reviewing zoning regulations and other restrictions on construction. Addressing outdated property tax valuations could help improve residential mobility and market efficiency. At the same time, the new real-estate specific macroprudential policy tools provide additional scope for tailored preventive measures to ensure systemic risks arising from the mortgage market remain contained. These are accompanied by new reporting requirements, expected to be introduced in 2019, to facilitate evaluation of risks and impact of potential policy changes. They also complement a 2016 call by the Financial Market Stability Board for the Austrian banks to maintain sustainable lending standards, although the guidance does not specify quantitative limits for the vulnerability ratios.”

Posted by at 10:57 AM

Labels: Global Housing Watch

Subscribe to: Posts