Tuesday, May 29, 2018

Fundamental Drivers of House Prices in the Netherlands? A Cross-Country Analysis

The latest IMF report on the Netherlands says that:

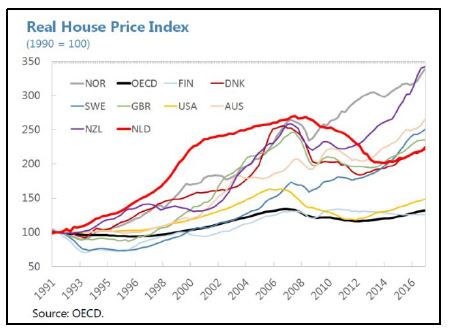

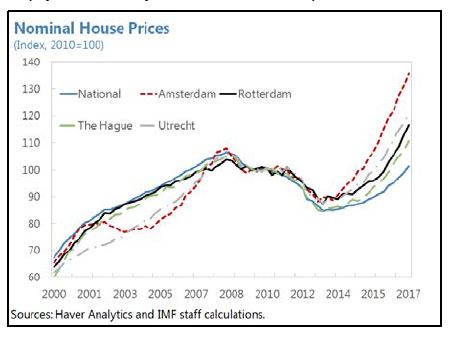

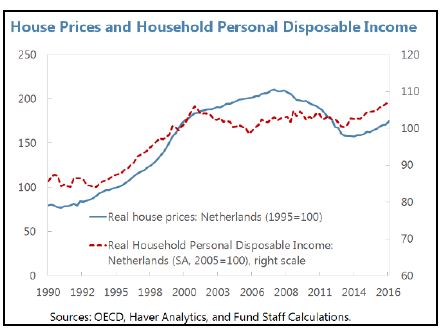

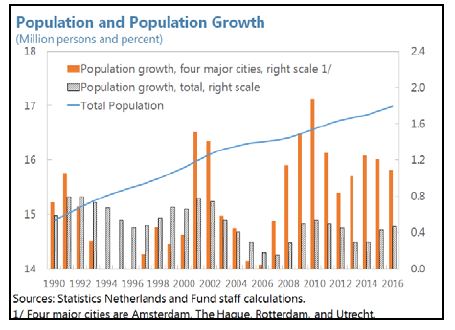

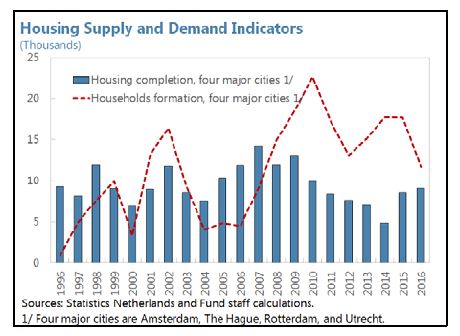

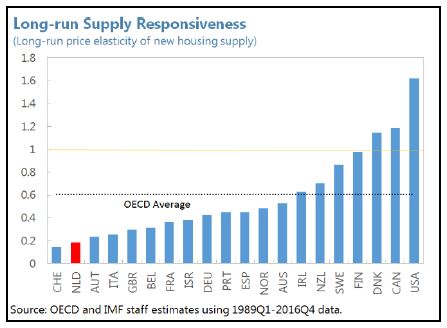

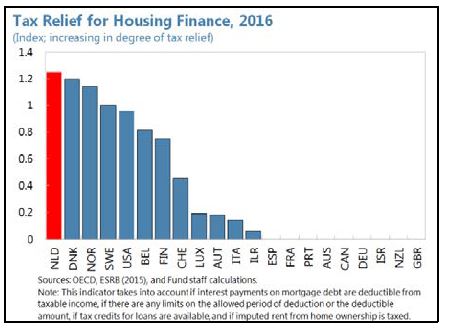

- “In sum, apart from the conventional fundamental demand and supply factors, the interaction of various institutional and structural factors seems to have contributed significantly to high and rapidly rising house prices in the Netherlands. The large direct and indirect subsidies for social housing and the highly regulated rental market is likely skewing housing needs and use in the Netherlands. The coexistence of a well-developed mortgage market and large tax preferences for owner-occupied housing and mortgage debt seems to have further fueled the surge in demand for homeownership and household debt. In addition, the sluggish response of housing supply exacerbated the situation by failing to cushion the impact of demand pressures.”

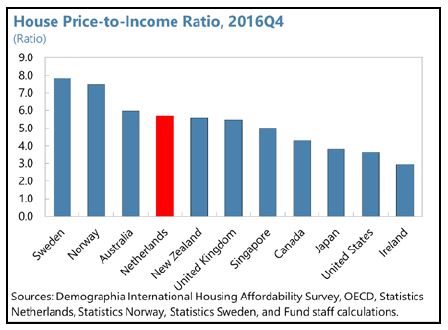

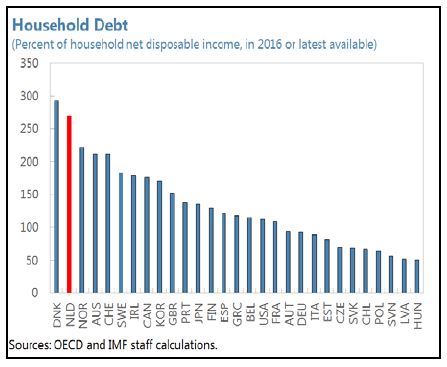

- “Overvalued house prices and elevated household debt are a source of vulnerability in the Netherlands in view of the importance of the housing market to both financial and macroeconomic stability. The recent house-price cycle left the Netherlands with elevated level of household debt and a significant share of underwater mortgages. While households have started to deleverage gradually from the record debt levels over the past years, a large correction of house prices, driven by slower real income growth, a reverse in sentiment, or interest rate hikes could weaken household balance sheets further and depress private demand, and in turn adversely affect corporate and bank earnings.”

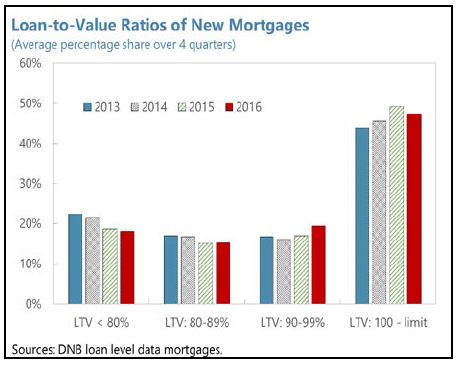

- “The authorities have been vigilant about the risks and have introduced a series of measures to target the owner-occupied housing sector and strengthen the resilience of banks and households, including additional bank capital buffer requirements in line with Basel III/CRD IV, an introduction of LTV and debt service-to-income (DSTI) caps since 2013, a gradual reduction of LTV limit for mortgages to 100 percent by 2018, a tax exemption for gifts used for housing down payments or mortgage repayments, allowing MID only for new fully amortizing loans, and a gradual reduction of the maximum tax rate allowed for MID from 52 percent in 2013 to 38 percent in 2042 in steps of ½ percent per year.”

- “Nevertheless, further and comprehensive reforms are needed to address the risks from the housing market and enhance the macro-financial resilience of the economy. A stable housing market (without pronounced boom-bust cycles) would contribute to smoother economic development. It is critical that policies work together to fundamentally address housing market imbalances that pose risks to stability and growth and hinder labor mobility:”

Posted by at 5:32 PM

Labels: Global Housing Watch

Subscribe to: Posts