Tuesday, June 22, 2021

Housing Market in Switzerland

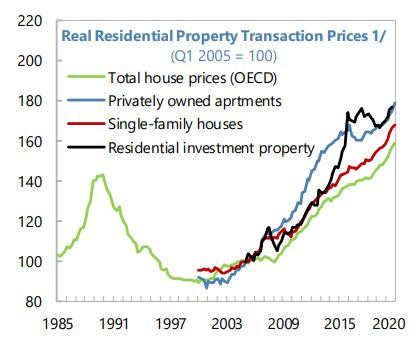

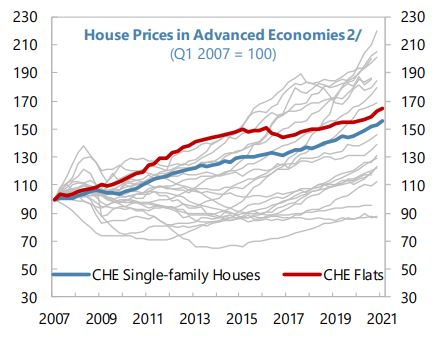

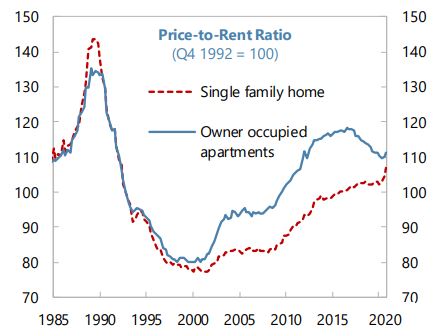

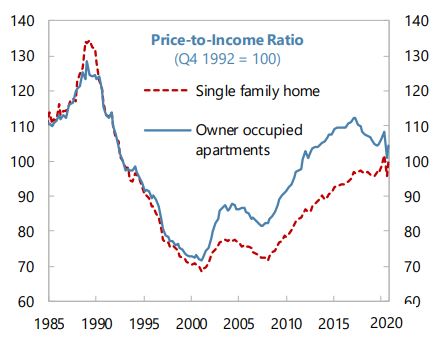

From the IMF’s latest report on Switzerland:

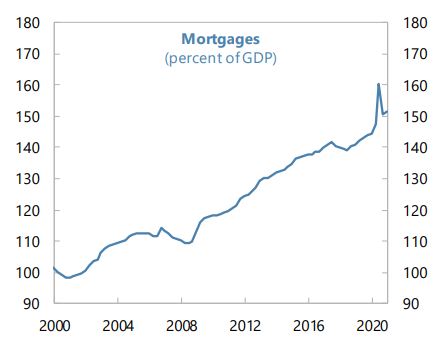

“Residential property prices have risen during the crisis, increasing affordability and imbalance concerns; commercial real estate faces risks from negative COVID-19 effects. Rising house prices have increased imbalances, especially among rentals, where vacancies are higher. A deterioration of affordability may take place when income support is withdrawn and should be monitored. Commercial real estate, especially outside core central business districts, also faces risks from negative pandemic effects and changes in occupancy, rents, and valuations. Voluntary self-regulation by financial institutions may face limits in terms of timeliness and stringency, and proactive measures (e.g., LTV or DTI restrictions) may be needed. The sectoral CCyB deactivation was appropriate, but should remain temporary, with buffers reset for potential real estate developments when conditions allow. Review of restrictions on housing supply in core urban areas and possible tax distortions may help identify measures to address imbalances.”

(…)

The authorities also see risks from real estate and search-for-yield behavior and are monitoring these carefully. They shared staff’s overall assessment and agreed that lagged effects of the COVID-19 crisis, real estate developments, and “lower-for-longer” pressures may have potentially important implications for financial stability. They will continue to monitor developments closely, as well as fintech and crypto activities. They highlighted progress made in implementing FSAP advice, especially on resources for FINMA, strengthening data collection and analysis, increasing risk-based on-site inspections, and improving recovery and resolution planning. They noted that the traditional approach of bank self-regulation in Switzerland has advantages—especially ownership—and stressed that self-regulatory measures may become binding and are augmented when needed. SNB and FINMA pointed to the effectiveness of new, stronger self-regulation on LTV ratios and faster amortization of mortgage loans for investment purposes from January 2020. Recent large market losses and risk controls are being closely examined. Smaller regional and cantonal banks have strong capital buffers and are prepared for further competitive pressures, including digitization. A solution is being sought for PostFinance.”

From the IMF’s latest report on Switzerland:

“Residential property prices have risen during the crisis, increasing affordability and imbalance concerns; commercial real estate faces risks from negative COVID-19 effects. Rising house prices have increased imbalances, especially among rentals, where vacancies are higher. A deterioration of affordability may take place when income support is withdrawn and should be monitored. Commercial real estate, especially outside core central business districts, also faces risks from negative pandemic effects and changes in occupancy,

Posted by at 2:28 PM

Labels: Global Housing Watch

Housing Market in Slovak Republic

From the IMF’s latest report on Slovak Republic:

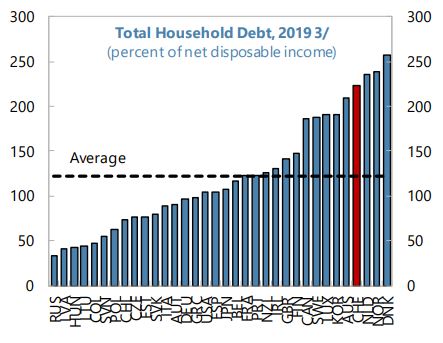

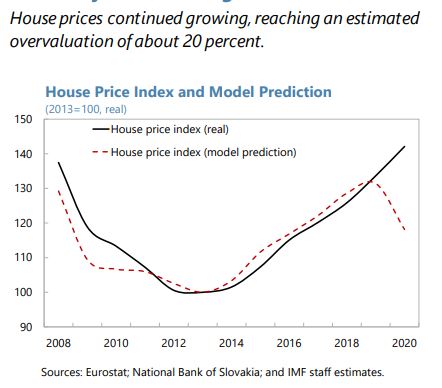

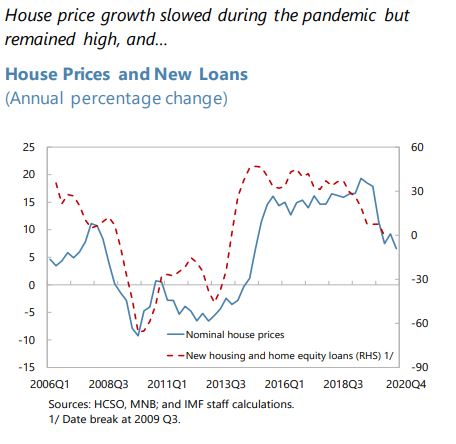

“Credit growth remained resilient, fueled by mortgage loans, while business lending slowed, and consumer loans contracted (…). Real estate prices continued to rise. With the significant GDP decline in 2020, a non-negligible gap emerged between actual and model-predicted house values though the extent of house price misalignment is difficult to gauge given the unique nature of the shock.

(…)

The macroprudential stance is broadly adequate from a financial stability point of view but there is scope to augment the macroprudential policy mix if housing market imbalances persist. Systemic risk stemming from the housing market, while manageable, has not dissipated. Notwithstanding the tightening of regulatory limits, mortgage credit and real estate prices continue to grow, and housing loans account for an increasing share in banks’ private sector loan portfolio.”

From the IMF’s latest report on Slovak Republic:

“Credit growth remained resilient, fueled by mortgage loans, while business lending slowed, and consumer loans contracted (…). Real estate prices continued to rise. With the significant GDP decline in 2020, a non-negligible gap emerged between actual and model-predicted house values though the extent of house price misalignment is difficult to gauge given the unique nature of the shock.

(…)

The macroprudential stance is broadly adequate from a financial stability point of view but there is scope to augment the macroprudential policy mix if housing market imbalances persist.

Posted by at 2:21 PM

Labels: Global Housing Watch

Sunday, June 20, 2021

Housing Market in Hungary

Posted by at 2:15 PM

Labels: Global Housing Watch

Thursday, June 17, 2021

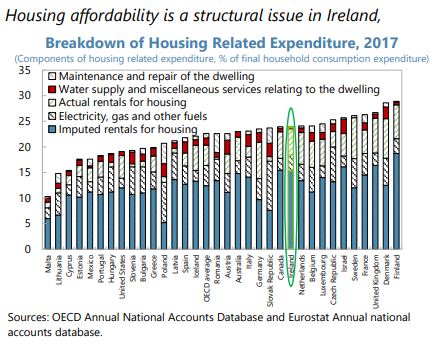

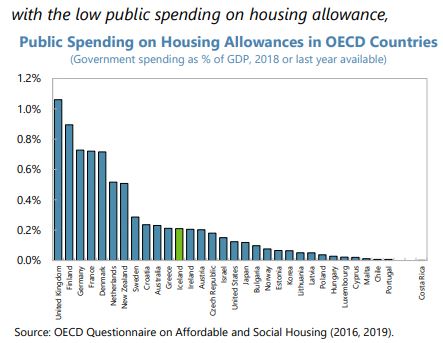

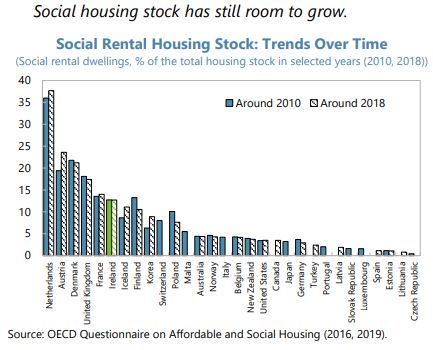

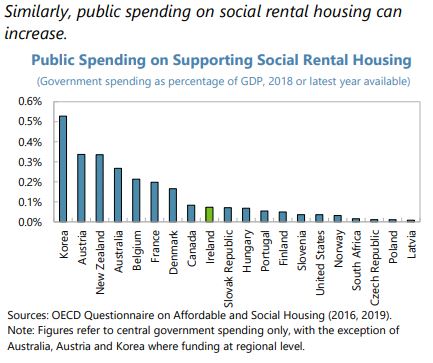

Housing Market in Ireland

From the IMF’s latest report on Ireland:

“Well-targeted macroprudential measures contained the build-up of vulnerabilities in the housing market and helped stabilize prices, but supply shortages and affordability concerns are on the rise. The initial dampening impact of COVID on the housing market was followed by a robust recovery in H2:2020, with the overall fall in residential construction only at 2 percent in 2020, which was largely due to the stringent first lockdown. To ease the dampening impact of the third lockdown on housing construction, the Health Regulations allowed for the designation of certain social housing projects as essential projects13, however, the housing supply-demand gap will likely widen further in the pandemic aftermath. After a small decline in H1:2020, house prices started to grow as demand exceeded supply. If an increasing part of household pandemic savings is directed to the housing market it could put further upward pressure on house prices.

Reducing shortages in affordable housing requires a multi-pronged approach. The government’s effort in this regard is welcome but more needs to be done by (i) releasing more land for development, (ii) streamlining approval processes for permits and re-zoning, (iii) assessing incentives to build rental properties, and (iv) increasing supply, including of social housing. The establishing of the Land Development Agency is a step in the right direction. On the other hand, policies should resist stimulating demand further given the existing supply-demand imbalances, and avoid resorting to short-term solutions such as relaxing prudential regulations to enable households to borrow more and the program to subsidize home purchase needs to be carefully designed and remain limited in size in order to minimize risks to the financial sector.

(…)

The authorities reiterated their commitment to address the housing and climate change challenges. They noted the progress towards improving housing supply and affordability through a comprehensive policy package, including the Help-to-buy Program, National Cost Rental Policy, and Land Development Agency (LDA) Bill, that provides a permanent basis to increase the supply of social and affordable homes and promote optimal use of State land. The recently legislated Affordable Housing Bill includes a 10 percent affordable housing requirement on new developments in addition to the existing requirement for 10 percent social housing. The authorities highlighted the recently legislated carbon tax increase, with a trajectory to 2030, and the ring-fenced use of the projected revenues of €9.5 billion for investment in energy efficiency, just transition, and low-emission agriculture. Additionally, the National Home Retrofit Scheme provides incentives for homeowners to improve their energy rating with 35 to 50 percent grant elements.”

From the IMF’s latest report on Ireland:

“Well-targeted macroprudential measures contained the build-up of vulnerabilities in the housing market and helped stabilize prices, but supply shortages and affordability concerns are on the rise. The initial dampening impact of COVID on the housing market was followed by a robust recovery in H2:2020, with the overall fall in residential construction only at 2 percent in 2020, which was largely due to the stringent first lockdown.

Posted by at 3:54 PM

Labels: Global Housing Watch

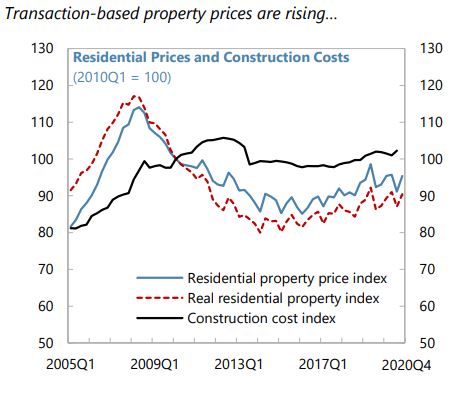

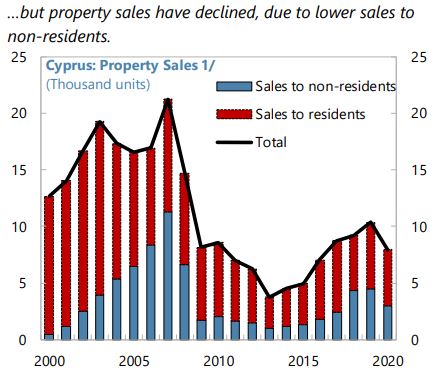

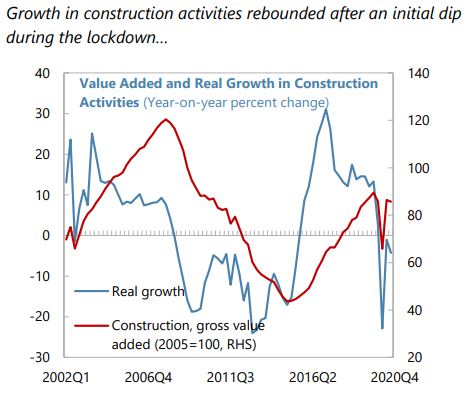

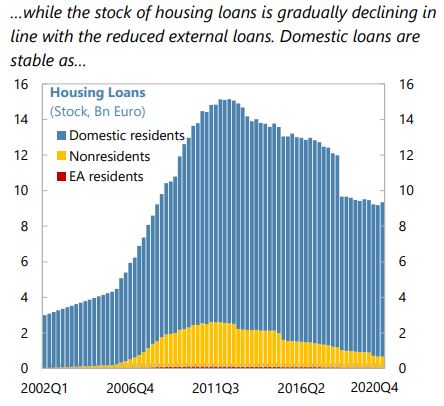

Housing Market in Cyprus

From the IMF’s latest report on Cyprus:

“Nevertheless, challenges are building. Nearly half of legacy NPLs were terminated five years earlier, potentially requiring sizable write-downs (Annex VI). Foreclosures have been suspended until end-July for smaller, collateralized loans and proposals under discussion in Parliament are expected to weaken the framework (¶22, third bullet). More than 80 percent of bank loans are to highly leveraged households and SMEs, concentrated in sectors like accommodation, food and retail, implying a high risk of an escalation of default rates and lower recovery value of assets after the expiry of loan repayment and foreclosure moratorium (Box 1). Banks are also exposed to property market risks through real estate holdings and collateral valuation. Although regulatory forbearance and fiscal support have prevented an immediate surge in loan impairments, a new wave of defaults as loan repayment obligations resume amidst tapering fiscal support could quickly consume the capital buffers of banks. Based on a stylized scenario with a 10 percent increase10 in NPLs that would push the latter to some 19.5 percent of total loans from the current 17.7 percent, staff estimates that restoring capital and provisions to pre-pandemic levels would entail capital needs of 1.5 percent of GDP.

(…)

Macro-financial risks from possible declines in property prices should be closely monitored, especially given the continued active use of debt-to-asset swaps in NPL resolution by banks and CACs. Risks appear limited for now given stable residential price developments (Text Figure 5 and Figure 8) and limited size of commercial real estate transactions. To ensure proper collateral valuation, results of actual sales transactions of repossessed collateral properties should be used by banks and CACs to review adequacy of valuation methodologies of these assets. Supervisory guidance to prevent excessive holding of repossessed collateral assets by banks should be maintained.”

From the IMF’s latest report on Cyprus:

“Nevertheless, challenges are building. Nearly half of legacy NPLs were terminated five years earlier, potentially requiring sizable write-downs (Annex VI). Foreclosures have been suspended until end-July for smaller, collateralized loans and proposals under discussion in Parliament are expected to weaken the framework (¶22, third bullet). More than 80 percent of bank loans are to highly leveraged households and SMEs, concentrated in sectors like accommodation,

Posted by at 3:27 PM

Labels: Global Housing Watch

Subscribe to: Posts