Thursday, April 13, 2017

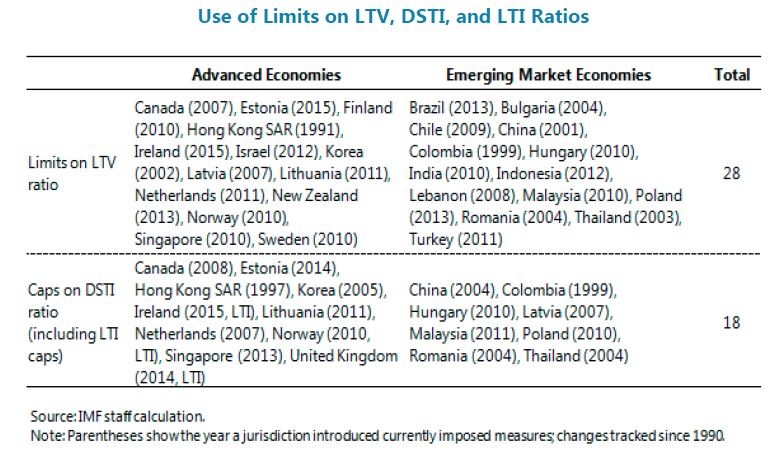

International Experience of Limits on LTV, DSTI, and LTI Ratios

From a new IMF report on Netherlands:

“A growing body of evidence points to the benefit of LTV and DSTI ratios in enhancing resilience and reducing fire-sale dynamics, in housing market downturns. Lee (2012) shows that house prices in Korea fell from 2008, but the delinquency ratio on household loans remained below 1 percent well into 2012, and claims that this implies that strict implementation of limits on LTV and DSTI ratios prevented household defaults even as house prices fell, thus reducing financial institution losses. The Financial Services Authority (2009) finds evidence of a correlation between higher LTV ratios, and higher default rates during 2008 in the United Kingdom Hallissey and others (2014) find that, based on loan-level data in Ireland, the default rate was higher for loans with higher LTV and LTI levels at origination, and that this relationship is stronger for the loans issued at the peak of the housing boom. They also show a positive relationship between LGD and LTV for loans with an LTV greater than 50 percent, with a sharp increase in the losses of defaulted loans at LTVs greater than 85 percent. Wong and others (2011) present cross-country evidence that, for a given fall in house prices (1 percent), the incidence of mortgage default is higher for countries without an LTV ratio limit (1.29 basis points) than for those with such a tool (0.35 basis points). The paper also notes that in the wake of the Asian financial crisis, property prices in Hong Kong SAR dropped by more than 40 percent from September 1997 to September 1998, but the mortgage delinquency ratio remained below 1.43 percent, which suggests that limits on LTV ratio reduced the probability of defaults faced by lenders.”

“Limits on LTV and DSTI ratios have been successful in targeting financial accelerator mechanisms that otherwise lead to a positive two-way feedback between credit growth and house price inflation. A number of studies have found that a tightening of LTV and DSTI ratios is associated with a decline in mortgage lending growth, thereby reducing the risk of an emergence of a housing bubble. Lim and others (2011) find that credit growth declines after limits on LTV and DTI ratios are introduced, and the LTV limits reduce substantially the procyclicality of credit growth. Igan and Kang (2011) show that limits on LTV ratios curb speculative incentives among existing house owners, validating the expectation channel. Crowe and others (2013) confirm the positive association between LTV at origination and subsequent price appreciation using state-level data in the United States—a 10 percentage point increase in the maximum LTV ratio is associated with a 13 percent increase in nominal house prices. Duca and others (2011) estimate that a 10 percentage point decrease in LTV ratio of mortgage loans for first-time buyers is associated with a 10 percentage point decline in the house price appreciation rate. Krznar and Morsink (2014) find that four measures to tighten macroprudential instruments (LTVs, in particular) in Canada were associated with lower mortgage credit and house price growth. IMF (2011) finds that lower LTV ratios reduce the transmission of real GDP growth shocks and shocks to population growth to house prices. Kuttner and Shim (2013) find that an incremental tightening in the DTI ratios is associated with a 4 to 7 percentage point deceleration in credit growth over the following year. RBNZ (2014) suggests that a cap on the share of high-LTV loans was effective, showing a dramatic fall in the share of mortgages over an 80 percent LTV ratio since the introduction in August 2013. Ahuja and Nabar (2011) find that limits on LTV ratios in Hong Kong SAR, where monetary policy is constrained as a small open economy with exchange rate pegs, reduced house prices and transaction volumes, albeit with a lag.”

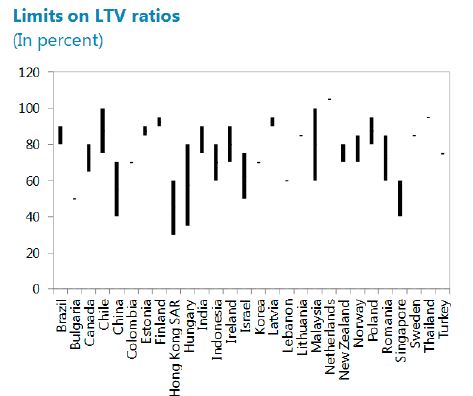

“Since the financial crisis, many countries have newly adopted these instruments. Limits on LTV ratios are below 80 percent in more than half of 28 sample countries, as shown below.”

From a new IMF report on Netherlands:

“A growing body of evidence points to the benefit of LTV and DSTI ratios in enhancing resilience and reducing fire-sale dynamics, in housing market downturns. Lee (2012) shows that house prices in Korea fell from 2008, but the delinquency ratio on household loans remained below 1 percent well into 2012, and claims that this implies that strict implementation of limits on LTV and DSTI ratios prevented household defaults even as house prices fell,

Posted by at 1:54 PM

Labels: Global Housing Watch

Tuesday, April 11, 2017

A Closer Look at Global Housing

Posted by at 4:55 PM

Labels: Global Housing Watch

Monday, April 10, 2017

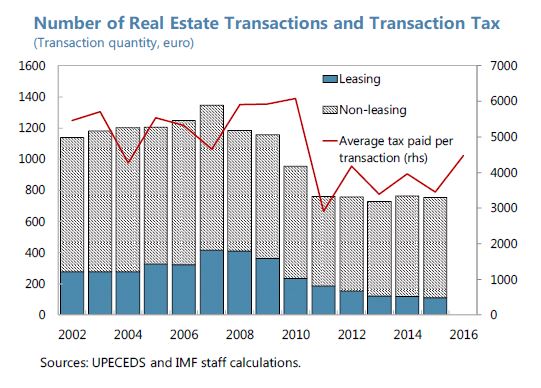

Housing Market in San Marino

“Credit growth continues to be subdued, and activity in the housing market remains at the low level. (…) In the housing market, the number of real estate sales remains low, but the average tax per transaction for non-leasing properties, which is likely correlated with real estate prices, has stabilized”, says IMF report.

“Credit growth continues to be subdued, and activity in the housing market remains at the low level. (…) In the housing market, the number of real estate sales remains low, but the average tax per transaction for non-leasing properties, which is likely correlated with real estate prices, has stabilized”, says IMF report.

Posted by at 1:30 PM

Labels: Global Housing Watch

Saturday, April 8, 2017

Workshop on Forecasting Issues in Developing Economies

Forecasting Issues in Developing Economies

April 26-27, 2017, Washington, DC

Wednesday, April 26

8.45-9.30 Registration and Breakfast

9.30-9.45 Opening Remarks: Tao Zhang, Deputy Managing Director, IMF

9.45-10.15 Session 1: Forecasting Turning Points

Chair: Prakash Loungani, Research Department, IMF

David Kuenzel, Wesleyan University

Chris Papageorgiou, Research Department, IMF

IMF Forecasts in Time of Crisis (Paper and Presentation)

(with Charis Christofides and Theo Eicher)

Discussant: Herman Stekler, George Washington University

10.15-11.15 Session 2: Energy and Climate Change

Chair: Gail Cohen, National Academies of Sciences, Engineering & Medicine

Jevgenijs Steinbuks, The World Bank

Assessing the Accuracy of Electricity Demand Forecasts in Developing Countries (Paper and Presentation)

Xinye Zheng, Renmin University of China

Economic Structure and Energy Consumption: Implications for 2030 Chinese Energy Demand (Paper and Presentation)

(with Fanghua Li and Li Zhang)

Discussant: Fred Joutz, George Washington University

11.15-11.30 Coffee Break

11.30-12.30 Session 3: Dealing with Uncertainty

Chair: Min Wei, Federal Reserve Board

Xuguang Simon Sheng, American University

The Measurement and Transmission of Macroeconomic Uncertainty: Evidence from the U.S. and BRIC Countries (Paper and Presentation)

(with Yang Liu)

Svetlana Makarova, University College London

Quasi Ex-Ante Inflation Forecast Uncertainty (Paper and Presentation)

(with Wojciech Charemza and Carlos Diaz)

Discussant: Sangyup (Sam) Choi, Mideastern & C. Asia Dept., IMF

12.30-2.00 Lunch

2.00-3.00 Session 4: Issues in Macroeconomics and Empirical Finance

Chair: Kirstin Hubrich, Federal Reserve Board

Speaker: Jonathan Wright, Johns Hopkins University

Ten Thoughts for Forecasting and Policy (Presentation)

Gloria Gonzalez-Rivera, University of California, Riverside

A Bootstrap Approach for Generalized Autocontour Testing. Implications for VIX Forecast Densities (Paper and Presentation)

(with J.H. Mazzeu, E. Ruiz, and H. Veiga)

3.00-3.30 Session 5: Financial Forecasting

Chair: Rita Biswas, University at Albany – SUNY

Sophia Chen, Research Department, IMF

Financial Information and Macroeconomic Forecasts (Paper and Presentation)

(with Romain Ranciere)

Discussant: Zhaogang Song, Johns Hopkins University

3.30-3.45 Group Photo

3.45-4.00 Coffee Break

4.00-5.15 Session 6: Frontiers of Forecasting

Chair: Herman Stekler, George Washington University

Keynotes:

Frank Diebold, University of Pennsylvania

Econometrics, Predictive Modeling, Causal Estimation, and Machine Learning

Kajal Lahiri, University at Albany – SUNY

The International Transmission of Shocks. A Factor Structural Analysis Using Forecast Data (Presentation)

7.00 Workshop Dinner

Taberna del Alabardero (1776 I St., NW; entrance on 18th Street)

Thursday, April 27

9.00-9.30 Breakfast

9.30-10.30 Session 7: Unemployment and Growth Forecasts

Chair: Milt Marquis, Florida State University

Neil Ericsson, Federal Reserve Board

Detecting Time-dependent Bias in the Fed’s Greenbook Forecasts (Paper)

(with Emilio Fiallos and J E. Seymour)

Laurence Ball, Johns Hopkins University

An Assessment of IMF Unemployment Forecasts for Advanced and Developing Economies (Paper and Presentation)

(with Zidong An, Joao Jalles and Prakash Loungani)

Discussant: Gabe Mathy, American University

10.30-10.45 Coffee Break

10.45-11.45 Session 8: Inflation and Monetary Policy

Chair: Subir Gokarn, Office of Executive Directors, IMF

Abhiman Das, Indian Institute of Management

Herbert Zhao, Towson University

Asymmetries in Indian Inflation Expectations: A Study Using IESH Quantitative Survey Data (Paper and Presentation)

(with Kajal Lahiri)

Roberto Duncan, Ohio University

New Perspectives on Forecasting Inflation in Emerging Economies: An Empirical Assessment (Paper and Presentation)

(with Enrique Martinez-Garcia)

Discussant: Tara Sinclair, George Washington University

11.45-12.30 Session 9: Economic Prospects for Africa

Chair: Maxwell Opoku-Afari, African Department, IMF

Speakers:Anthony Simpasa, African Development Bank

Intelligent Forecasting of Economic Growth for African Economies: Artificial Neural Networks versus Time Series and Structural Econometric Models (Paper and Presentation)

(with Chuku Chuku and Jacob Oduor)

Discussant: Khaled Hussein, UN Economic Commission for Africa

Forecasting Issues in Developing Economies

April 26-27, 2017, Washington, DC

Wednesday, April 26

8.45-9.30 Registration and Breakfast

9.30-9.45 Opening Remarks: Tao Zhang, Deputy Managing Director, IMF

9.45-10.15 Session 1: Forecasting Turning Points

Chair: Prakash Loungani, Research Department, IMF

David Kuenzel, Wesleyan University

Chris Papageorgiou, Research Department, IMF

IMF Forecasts in Time of Crisis (Paper and Presentation)

(with Charis Christofides and Theo Eicher)

Discussant: Herman Stekler,

Posted by at 5:11 PM

Labels: Forecasting Forum

Tuesday, April 4, 2017

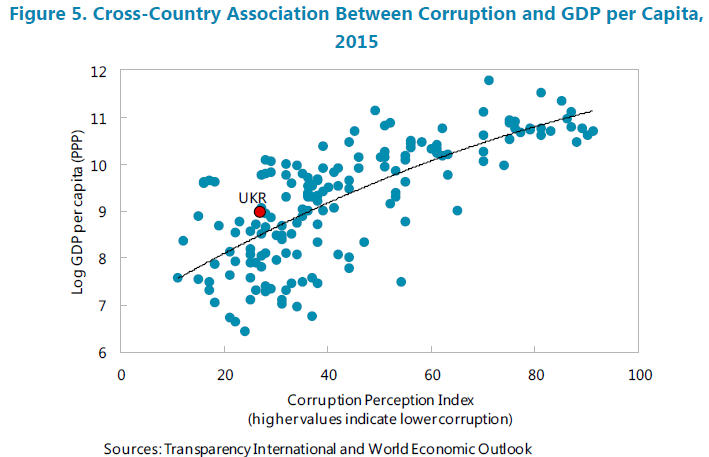

Corruption and Growth in Ukraine

An IMF report says “The level of corruption in Ukraine is exceptionally high. This can severely undermine economic growth prospects, in particular by hindering private investment. Reducing corruption is therefore essential to speed up the process of economic convergence to the rest of Europe. Regional comparisons help identifying best practices in reducing corruption. The Ukrainian authorities have recently adopted important measures that follow some of these best practices. They are, however, facing a number of specific challenges, including the concentration of political and economic powers in a small group of people which may hamper effective anti-corruption efforts.”

Continue reading here.

An IMF report says “The level of corruption in Ukraine is exceptionally high. This can severely undermine economic growth prospects, in particular by hindering private investment. Reducing corruption is therefore essential to speed up the process of economic convergence to the rest of Europe. Regional comparisons help identifying best practices in reducing corruption. The Ukrainian authorities have recently adopted important measures that follow some of these best practices.

Posted by at 12:00 PM

Labels: Inclusive Growth

Subscribe to: Posts