Friday, January 28, 2022

China: Downside Risks from Property Developer Stress

From the IMF’s latest report on China:

“One of China’s largest property developers, Evergrande, has begun restructuring talks with offshore creditors to alleviate rising financial stress following a tightening of regulations to rein in the highly-leveraged real estate sector. Funding pressures have since spread to other property developers, posing concerns of negative spillovers to the broader economy and global markets.2 The authorities have the policy space and tools to contain these risks but will have to balance difficult trade-offs between financial stability and moral hazard. Over the long term, deeper structural reforms are needed to comprehensively address the risks from China’s property market.

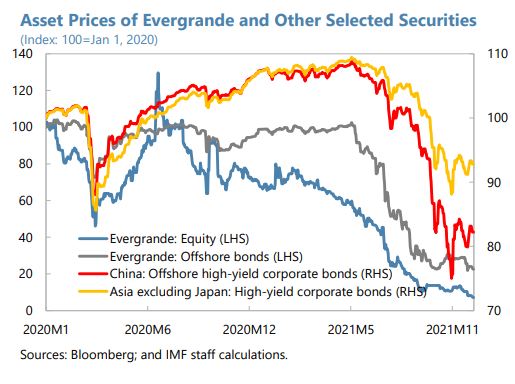

Evergrande, one of China’s largest property developers, has entered restructuring negotiations amid severe funding strains. With over US$300 billion in liabilities to creditors, suppliers, and households, the company’s bond prices are trading at distressed levels. So far, contagion has spread mostly to other financially weak developers and lower-rated corporates in China, with limited impact on higher-rated developers. Markets in and outside of China initially reacted strongly to Evergrande’s stress but subsequently stabilized following actions by the authorities to limit wider spillovers.

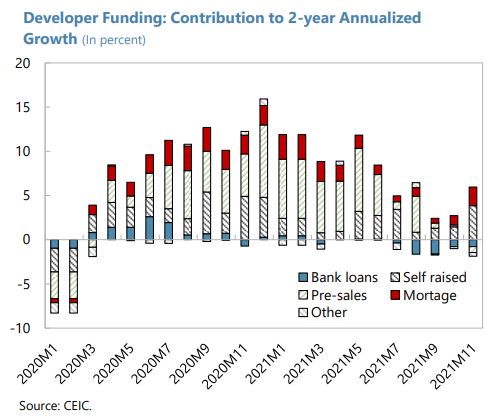

Evergrande’s troubles follow a broad regulatory campaign to rein in China’s highly leveraged real estate sector. Property plays a large role in both China’s economy and financial system, accounting for about a quarter of both total fixed investment and bank lending over the past 5 years before the pandemic. On the demand side, the property sector’s importance reflects massive household savings—linked, in part, to the inadequate social protection system (see Box 2)—and limited alternative investment options. After allowing private housing investment to function as a key countercyclical policy tool in the aftermath of the Global Financial Crisis, including through a significant run-up in leverage, the authorities have repeatedly sought to rein in the property sector owing to financial stability concerns. They redoubled these efforts after the initial recovery from last year’s national pandemic lockdown, including by imposing tougher restrictions on new funding for developers.

New controls on developer credit bring to the fore concerns over the potential for intra-sector contagion. Like Evergrande, many property developers are also highly leveraged, with weak earnings and liquidity. Many developers are also exposed to inadequately disclosed risks, like sizeable but opaque off balance sheet risks from guarantees and joint ventures. The sector’s growing dependence on pre-sales of unfinished housing as a source of funding—now over one-third, up from 25 percent in 2014—increases its vulnerability to sector-wide confidence shocks and runs.3 Some of this revenue is not properly escrowed, a risky practice which increases leverage and makes households creditors, despite their limited ability to monitor the risks of these loans. The failure to complete unfinished housing inventory by defaulting developers not only undermines consumer confidence, but also risks lowering households’ willingness to buy homes via pre-sales with other developers, propagating liquidity strains within the sector. These vulnerabilities are compounded by survey-based evidence that points to high price-to-income ratios in various cities.

These vulnerabilities could potentially lead to a broader credit crunch among developers, raising risks

of a downside scenario engulfing the wider real estate sector:• Developer funding pressures could spill over to property prices if housing demand slumps or distressed developers are forced to sell inventories at a discount, reinforcing contagion within the sector.

• Falling prices and increasing construction delays could halt pre-sales and trigger a sharp retrenchment of housing demand by households generally, further amplifying financial stress for property developers.

• At this point, the financial system might be affected, causing credit supply to contract for developers and households alike. While banks’ loan exposure to Evergrande is not systemic, lending to real estate firms represents 7 percent of total lending, residential mortgages are another 21 percent, and a large share of other bank loans are collateralized by property. In addition, banks are highly exposed to non-bank financial institutions, which in turn hold large exposures to developers and other land-exposed firms. Trusts, a type of NBFI, have financed between 16-22 percent of the rapidly growing real estate investment in China over the last four years.

A sharper-than-expected slowdown in the property sector could trigger a wide range of adverse effects on aggregate demand, with feedback loops to the financial sector. Domestically, this could include a sharp retrenchment of real estate investment, which in 2020 accounted for an estimated 8.7 percent of GDP. This would have knock-on effects on other private investment as the real estate sector accounts for 11 percent of total purchases of intermediate materials. Moreover, local governments may be forced into unwanted fiscal consolidation as revenues from land sales fall. And a sustained fall in house prices would likely weigh on private consumption, through weaker income and employment (construction represents 13 percent of total employment) and wealth effects (80 percent of households own their homes).

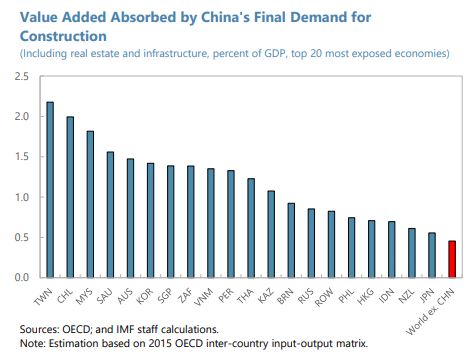

A sudden slowdown in China’s growth would create spillovers through trade and commodity prices. Model-based simulations of a decline in investment in China due to financial stress suggest that a one percent decline in China’s output lowers growth in the rest of the world by about one-tenth of a percent (Dizioli and others, 2016). While real estate investment is less trade-intensive than other investment, direct and indirect trade exposures from the rest of the world are still sizeable. Foreign value added in China’s construction sector (including both real estate and infrastructure) accounts for 0.5 percent of global (excl. China) GDP, with larger exposures for some Asian and commodity exporting economies. China’s final demand in the construction sector absorbs a sizeable fraction of global value added in basic metals (14 percent), mining (6 percent) and oil and chemicals (5 percent) sectors

Financial spillovers would mostly operate via a deterioration in global risk appetite. While direct nonresidents’ holdings of Chinese financial assets have grown in recent years as a result of the inclusion of China in global benchmark indexes, with property developers being active issuers in offshore bond markets (US$200 billion of outstanding bonds), direct exposures to China remain relatively small. However, given strong trade related spillovers, global risk appetite would likely be affected, which could lead to tighter financial conditions, especially in emerging markets (GFSR, Apr, 2016). The policy response to property developer stress necessarily involves difficult trade-offs. In the short term, authorities have the policy space and tools to limit disorderly spillovers within the financial sector and lessen any adverse impact on the economy. The timing and extent of support, however, must balance the need to avert destabilizing confidence shocks with the imperative to minimize backtracking in efforts to curb moral hazard and contain leverage. Key elements of a policy response should include:

• Guarding against systemic contagion: For now, the priority should be to contain large-scale spillovers to housing demand and economic activity while still allowing market forces to reduce vulnerabilities. This requires intensifying risk monitoring efforts, strengthening the central government’s coordinating role in policy responses, and facilitating the restructuring of troubled developers while ensuring the timely completion of pre-sold housing inventories.

• Dealing with escalating risk: if large-scale spillovers to housing markets threaten economic and financial stability, bolder steps will be needed including government backstops for liquidity provision to stressed developers and guarantee mechanisms for completion of presold housing. These measures should be temporary and subject to strict safeguards to minimize moral hazard (see below). Decisive macroeconomic easing would protect against shortfalls in aggregate demand.

• Addressing structural shortcomings. As soon as risks recede, ensuring property sector risks decline to safer levels will require curbing risks from pre-sales practices, introducing property taxes, and other measures to ease investment-related housing demand and reduce local government incentives to boost property markets.”

From the IMF’s latest report on China:

“One of China’s largest property developers, Evergrande, has begun restructuring talks with offshore creditors to alleviate rising financial stress following a tightening of regulations to rein in the highly-leveraged real estate sector. Funding pressures have since spread to other property developers, posing concerns of negative spillovers to the broader economy and global markets.2 The authorities have the policy space and tools to contain these risks but will have to balance difficult trade-offs between financial stability and moral hazard.

Posted by at 12:09 PM

Labels: Global Housing Watch

Jobs, Africa, and the shift towards services

Source: VoxEU CEPR

“The servicification of economic activity occurring across Africa has implications for the continent’s future. Using per capita nightlight luminosity as a proxy for economic development, this column finds a strong positive association between higher-skill services and economic growth that varies according to geography, institutions, technology, and market conditions. Data on the structure of employment in African economies reveal significant shifts in the composition of employment towards services across and within countries, and towards growth in service-related occupations across all sectors of the economy.”

The authors present new data on the composition of jobs in the services sector at the sub-national level in a sample of 13 African countries, describe how this has changed over time, and explain how employment in services correlates with indicators of economic development commonly used in the literature. Throughout their sample, they find that the share of agriculture in total employment declined through the decades but was offset by an equivalent increase in the share of services. They go on to dig deeper into aspects like characteristics of service sector employees and differing capacities of different services in supporting workers’ productivity.

Source: VoxEU CEPR

“The servicification of economic activity occurring across Africa has implications for the continent’s future. Using per capita nightlight luminosity as a proxy for economic development, this column finds a strong positive association between higher-skill services and economic growth that varies according to geography, institutions, technology, and market conditions. Data on the structure of employment in African economies reveal significant shifts in the composition of employment towards services across and within countries,

Posted by at 11:09 AM

Labels: Inclusive Growth

Housing View – January 28, 2022

On cross-country:

- Younger generations and the lost dream of homeownership – VoxEU

- Why skyscrapers are so short – Works in progress

On the US:

- How credit conditions affect housing prices — lessons from the ’00s. How might credit conditions affect this year’s housing market? A look to the past can offer some clues. – MIT

- The housing boom isn’t over yet, predicts a top analyst who sees a 12% increase this year – AEI

- A Typical U.S. Home Is Now Valued at $320,662 — 20% More Than a Year Ago. Low inventory and unrelenting demand are continuing to fuel price growth in the American real estate market. – Bloomberg

- Volatility of lumber prices hits high not seen since end of World War II — why home buyers should be concerned. Fluctuations in the prices of building supplies are complicating construction of new homes – Market Watch

- Transcript: Inventory Vanishing and Bidding Wars Exploding in Crazy U.S. Housing Market – Bloomberg

- A Typical U.S. Home Is Now Valued at $320,662 — 20% More Than a Year Ago. Low inventory and unrelenting demand are continuing to fuel price growth in the American real estate market. – Bloomberg

- Real Estate Is Emerging as a Hedge Against Roaring Inflation. Those seeking alternative investments from stocks and bonds may turn to the housing market, but that strategy still presents risks. – Bloomberg

- Illinois Homeowners Can Now Remove Racist Clauses From Their Property Deeds. With a new law, Illinois joins over a dozen states that have made it easier to remove racial restrictive covenants, which were used to bar people of certain races from buying homes. – New York Times

- New Report Shows a Surging Rental Market, Starkly Divided by Race and Renter Incomes – Harvard Joint Center for Housing Studies

- The US home construction boom is excluding a big group of Americans – Quartz

- Kevin Erdmann was right – Econlib

- How subprime lending emerged in minority neighbourhoods – London School of Economics

- Florida’s West Coast Cities Top WSJ/Realtor.com’s Housing Index. Naples led the fourth-quarter rankings, as the Sunshine State attracted home buyers looking to work remotely near the beach – Wall Street Journal and Realtor

- Zillow’s Open Market Home Price Appreciation Forecasting Methodology – Zillow

- What It Will Take to Sustainably Increase the Homeownership Rate? – Harvard Joint Center for Housing Studies

- With Housing Prices Spiking Everywhere, Where Is It Cheaper To Rent vs. Buy? – Realtor

On China

- Beijing Will Save Housing Projects, but Not Necessarily Developers. To head off a deepening housing downturn, Beijing is backpedaling a bit on tough leverage rules. That might not be enough to save weaker developers. – Wall Street Journal

- China cuts mortgage lending rate for first time in two years. Beijing introduces measure amid property sector liquidity crisis and consumption slowdown – FT

- China property sector could see “significant” policy easing -BNP Paribas – Reuters

- China Weighs Breaking Up Evergrande to Contain Property Crisis – Bloomberg

- China’s Private Cities – Marginal Revolution

On other countries:

- [Canada] This Red-Hot Housing Market Is Betting Interest Rates Will Never Rise. Canadian homeowners’ gamble could backfire if rates increase more than one percentage point. – Bloomberg

- [Ireland] Why Ireland’s housing bubble burst – Works in progress

- [Netherlands] The Netherlands’ house price rises accelerating – Global Property Guide

- [New Zealand] New Zealand’s bipartisan housing reforms offer a model to other countries – Brookings

- [Taiwan] Taiwan’s housing market remains buoyant – Global Property Guide

- [United Kingdom] U.K. Property Sellers Keep Upper Hand as Supply Squeeze Persists – Bloomberg

- [United Kingdom] What’s next for the housing market in 2022? – Lloyds Banking Group

- [United Kingdom] The plight of the UK’s first-time buyers. The immediate pressures of the pandemic may have eased, but prospective homeowners must now contend with record prices and a looming cost of living crisis – FT

On cross-country:

- Younger generations and the lost dream of homeownership – VoxEU

- Why skyscrapers are so short – Works in progress

On the US:

- How credit conditions affect housing prices — lessons from the ’00s. How might credit conditions affect this year’s housing market? A look to the past can offer some clues. – MIT

- The housing boom isn’t over yet,

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, January 27, 2022

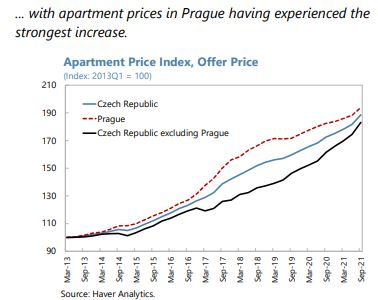

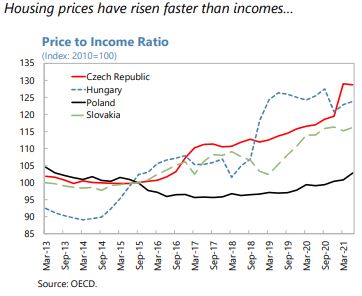

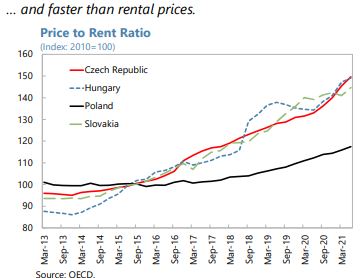

Housing Market in Czech Republic

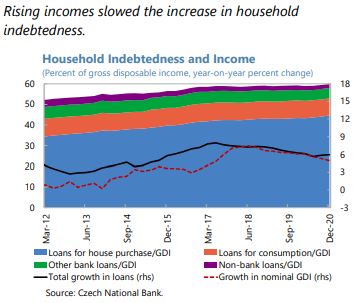

From IMF’s latest report on Czech Republic:

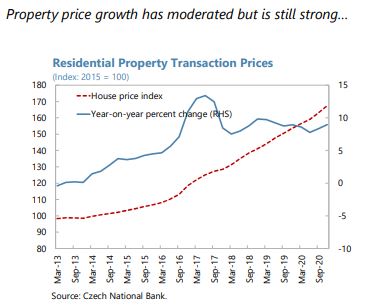

“Amid robust mortgage credit growth, property price-growth significantly accelerated from already elevated levels stretching valuations and worsening affordability. Property prices grew by about 8½ percent in 2020, down from about 9¼ percent in 2019, but accelerated to 14½ percent y-o-y in 2021:Q2. The Czech Republic has experienced one of the highest property price appreciation rates in the EU, reaching a cumulative growth rate of about 54 percent in the five years prior to 2021. The CNB estimates property prices to be overvalued by 25 percent on average (as of mid-2021). The steep property price increase has deteriorated affordability as reflected in price-to-income and price-to-rent ratios.

Macrofinancial vulnerabilities due to increasing risk-taking by lenders amid growing household leverage and high and rapidly rising property valuations warrant close monitoring. Although aggregate household indebtedness is still low compared to other EU countries, it increased robustly by 2½ percentage points to 34 percent of GDP during 2020. Fast increases in property prices, amid loosening credit standards and macroprudential policy during the pandemic, resulted in households/lenders taking larger and riskier mortgages (…). Significant increases in risk taking, in an environment of high and rapidly rising house prices, exposes households to price and interest rate shocks that could harm those who purchased in overvalued areas, who are highly levered, or low-income households—for which debt service is already burdensome. These vulnerabilities might be compounded by the large proportion of mortgages with fixation periods up to five years.

Recent developments warrant tightening prudential tools while deploying coordinated housing supply and tax policies. Properly calibrated income-based measures can improve risk taking incentives and support affordability. Staff welcomes the CNB’s decision in November 2021 (effective from April 2022) to tighten limits on mortgage loan ratios as follows: DTI (8.5), DSTI (45 percent) and LTV (80 percent). Close monitoring of market developments is necessary with a potential for further tightening down the road. Importantly, clear communication of macroprudential policy actions and adequate coordination of the overall policy mix are key to ensure a smooth stabilization. Proper calibration of macroprudential tools for lower risk groups—first-time home buyers and low-levered households—is warranted to safeguard proper access to financing. An improved risk-based prudential framework (Section D) could be combined with the macroprudential setup to facilitate calibration of these measures.

Housing Supply

Pre-existing housing supply shortages persisted throughout the pandemic, partly reinforced by temporary pauses in construction activity. A new construction law, aimed at simplifying the construction code and the reportedly cumbersome permitting process, through creation of a one-stopshop for construction companies, was adopted in July, 2021 but implementation of some of its provisions will take until 2023. The impact on the number of granted residential building permits has been limited so far.

Tax Policy

Revenues from property taxes are low in comparison to other countries and will further fall after the recent cancellation of the property transaction tax. Real estate property taxation should be based on current market valuations and not on floor space. While the recent reduction of the maximum deductible amount of mortgage interest from CZK 300,000 to CZK 150,000 per year starting in 2021 is welcome, this benefit could be eliminated completely as in other countries.

Staff welcomes the recent reform of the macroprudential framework that provides the CNB with the legal powers to implement macroprudential policy. In July 2021, the CNB was given powers to make macroprudential limits legally binding, which is consistent with international best practice.

Authorities’ Views

The authorities acknowledge the risks stemming from the heated property market and stand ready to tighten macroprudential policies as needed. They acknowledged the increasing risk taking by households amid high and rapid house price growth and stand committed to closely monitor market developments to decide on further policy actions. On the basis of new statutory powers, the CNB Bank Board decided on November 25, 2021 to reintroduce limits on DTI and DSTI ratios and to tighten the LTV limit.”

From IMF’s latest report on Czech Republic:

“Amid robust mortgage credit growth, property price-growth significantly accelerated from already elevated levels stretching valuations and worsening affordability. Property prices grew by about 8½ percent in 2020, down from about 9¼ percent in 2019, but accelerated to 14½ percent y-o-y in 2021:Q2. The Czech Republic has experienced one of the highest property price appreciation rates in the EU, reaching a cumulative growth rate of about 54 percent in the five years prior to 2021.

Posted by at 11:12 AM

Labels: Global Housing Watch

African history through the lens of economics

From a VoxEU post by Nathan Nunn, Stelios Michalopoulos, Elias Papaioannou, and Léonard Wantchékon:

“Since the 2000s, a vibrant stream of research on African political economy and economic history has emerged that has produced a plethora of insights and has uncovered the shadow that Africa’s past casts on contemporary economic, social, and political development. This column introduces a free online course on “African History through the Lens of Economics”, which will bring together the considerable volume of work in the economics literature of the past decades. The course is open to students with a background and interest in economics, political science, history, cultural anthropology, and psychology.

Views about Africa are, were, and most likely will continue to be highly polarising. Some economists, finance professionals, multinational executives, global entrepreneurs, and businesspeople are bullish, as there are investment opportunities in infrastructure, manufacturing, and technology, coupled with a young population that is increasingly more educated and confident. However, many are less optimistic, concerned about misgovernance, conflict, weak state capacity, corruption and poor infrastructure. Pessimists point to Africa’s dark past, including the atrocities and exploitation during colonisation, and the slave trades.

In 2000, The Economist called Africa “the hopeless continent”. A decade later, after strong growth and institutional advancement, it renamed it “the hopeful continent”. A few years later, in 2016, the magazine described it in more nuanced terms as a land of “1.2 billion opportunities” – a reference to the potential market that its huge population constituted. Economics research has followed a similar train. In the 1970s, 1980s, and 1990s, only a handful of papers were published outside specialised outlets. But, since the 2000s, a vibrant stream of research on African political economy and economic history has emerged. The new economic history approach departs greatly from prevailing thinking in important ways.

First, scholars realised that ill-conceived, post-independence urban-rural agriculture and trade policies, authoritarianism, conflict, corruption, and lack of structural transformation (the foci of pre-2000 studies) often had deep roots stemming from colonial extraction, enslavement, the artificial design of country borders, underinvestment, and cash-crop specialisation during colonisation.

Second, the new economics research became more interdisciplinary. For example, applied research started scrutinising influential ideas proposed by historians, political scientists, sociologists, and even cultural anthropologists.

Third, the studies began moving beyond purely economic outcomes and drivers of development. They examined, for example, the origins and the implications of the vast differences in social capital, civicism, cultural preferences, and values. This more evolutionary approach to economic history has led to a fruitful dialogue between economics and the other social sciences; albeit one not without tension.”

From a VoxEU post by Nathan Nunn, Stelios Michalopoulos, Elias Papaioannou, and Léonard Wantchékon:

“Since the 2000s, a vibrant stream of research on African political economy and economic history has emerged that has produced a plethora of insights and has uncovered the shadow that Africa’s past casts on contemporary economic, social, and political development. This column introduces a free online course on “African History through the Lens of Economics”,

Posted by at 10:54 AM

Labels: Macro Demystified

Subscribe to: Posts