Saturday, January 29, 2022

The informal sector: Compounding the damage of Covid-19

Source: VoxEU CEPR

The informal sector, which accounts for nearly one-third of the GDP and employment in emerging and developing economies (EMDEs), has not only been the worst affected by the Covid-19 pandemic but is now also threatening to dampen economic recovery. Three features of the informal sector have compounded the damage of Covid-19 on activity: (i) their predominant presence in the service sector, (ii) limited savings and access to social safety nets, and (iii) the lack of effective policy support (Ohnsorge and Yu 2021).

This column assesses the impact of the pandemic on job losses in the informal sector of both manufacturing and service sectors of EMDEs and the impact of support policies rolled out by governments. Thus, recommendations call for facilitating access to finance for small firms, adopting cash transfer programs in the short run for countries with larger poor populations (Furceri, Loungani, Ostry, and Pizzuto, 2020), and using technology to reach the poor and informal workers.

Source: VoxEU CEPR

The informal sector, which accounts for nearly one-third of the GDP and employment in emerging and developing economies (EMDEs), has not only been the worst affected by the Covid-19 pandemic but is now also threatening to dampen economic recovery. Three features of the informal sector have compounded the damage of Covid-19 on activity: (i) their predominant presence in the service sector, (ii) limited savings and access to social safety nets,

Posted by at 1:27 PM

Labels: Inclusive Growth

Friday, January 28, 2022

The Financialization of Housing in Europe

From a new report by Daniela Gabor and Sebastian Kohl:

“Over the past decades, institutional landlords – from real estate companies like the German giant Vonovia to private equity companies like Blackstone, or pension funds like ABP, the Dutch pension fund for government and education employees – have minted EUR 40bn of Berlin’s houses into assets that they rent out. This is roughly double the combined value of London’s and Amsterdam’s institutionally owned houses and it is a trend that has accelerated since the COVID19 pandemic. Europe’s residential real estate has become an attractive asset class for investors worldwide, supported by a range of government policies that are ostensibly aimed at homeowners: support for housing markets pushes up house prices and reduces affordability for citizens, whereas income support for rent-paying households ensures stable returns for investors.

In response, citizens across Europe – from Berlin to Dublin and Madrid – have mobilized to pressure governments into taking action. From rent controls to better regulation or even expropriation of institutional landlords, the political tide seems to be turning against a decades-old phenomenon known as the financialization of housing. A mega-trend across housing markets everywhere, it can be understood as (1) the disproportionate growth of housing finance relative to the underlying housing economy or (2) the turn to Housing as an Asset Class (HAC), captured by the increasing for-profit and financial orientation of actors in housing markets, and encouraged in Europe by a broad range of European-level financial legislation.

In this report, we explore the growing importance of institutional landlords such as Blackstone, focusing in particular on the mechanisms through which European legislation has accommodated their strategies to transform housing into asset classes. We use data from the private provider Preqin to map the complex financial ecosystem behind private equity landlords. We then propose a set of reforms that would de financialize housing for the public good.”

From a new report by Daniela Gabor and Sebastian Kohl:

“Over the past decades, institutional landlords – from real estate companies like the German giant Vonovia to private equity companies like Blackstone, or pension funds like ABP, the Dutch pension fund for government and education employees – have minted EUR 40bn of Berlin’s houses into assets that they rent out. This is roughly double the combined value of London’s and Amsterdam’s institutionally owned houses and it is a trend that has accelerated since the COVID19 pandemic.

Posted by at 12:31 PM

Labels: Global Housing Watch

Robots and Firm Investment

From a NBER paper by Efraim Benmelech and Michal Zator:

“Automation technologies, and robots in particular, are thought to be massively displacing workers and transforming the future of work. We study firm investment in automation using cross-country data on robotization as well as administrative data from Germany with information on firm-level automation decisions. Our findings suggest that the impact of robots on firms has been limited. First, investment in robots is small and highly concentrated in a few industries, accounting for less than 0.30% of aggregate expenditures on equipment. Second, recent increases in robotization do not resemble the explosive growth observed for IT technologies in the past, and are driven mostly by catching-up of developing countries. Third, robot adoption by firms endogenously responds to labor scarcity, alleviating potential displacement of existing workers. Fourth, firms that invest in robots increase employment, while total employment effect in exposed industries and regions is negative, but modest in magnitude. We contrast robots with other digital technologies that are more widespread. Their importance in firms’ investment is significantly higher, and their link with labor markets, while sharing some similarities with robots, appears markedly different.”

From a NBER paper by Efraim Benmelech and Michal Zator:

“Automation technologies, and robots in particular, are thought to be massively displacing workers and transforming the future of work. We study firm investment in automation using cross-country data on robotization as well as administrative data from Germany with information on firm-level automation decisions. Our findings suggest that the impact of robots on firms has been limited. First, investment in robots is small and highly concentrated in a few industries,

Posted by at 12:17 PM

Labels: Macro Demystified

Understanding the Resurgence of the SOEs in China: Evidence from the Real Estate Sector

From a NBER paper by Hanming Fang, Jing Wu, Rongjie Zhang and Li-An Zhou:

“We advance a novel hypothesis that China’s recent anti-corruption campaign may have contributed to the recent resurgence of the state-owned enterprises (SOEs) in China as an unintended consequence. We explore the nexus between the anti-corruption campaign and the SOE resurgence by presenting supporting evidence from the Chinese real estate sector, which is notorious for pervasive rent-seeking and corruption. We use a unique data set of land parcel transactions merged with firm-level registration information and a difference-in-differences empirical design to show that, relative to the industrial land parcels which serve as the control, the fraction of residential land parcels purchased by SOEs increased significantly relative to that purchased by private developers after the anti-corruption campaign. This finding is robust to a set of alternative specifications. We interpret the findings through the lens of a model where we show, since selling land to private developers carries the stereotype that the city official may have received bribes, even the “clean” local officials will become more willing to award land to SOEs despite the presence of more efficient competing private developers. We find evidence consistent with the model predictions.”

From a NBER paper by Hanming Fang, Jing Wu, Rongjie Zhang and Li-An Zhou:

“We advance a novel hypothesis that China’s recent anti-corruption campaign may have contributed to the recent resurgence of the state-owned enterprises (SOEs) in China as an unintended consequence. We explore the nexus between the anti-corruption campaign and the SOE resurgence by presenting supporting evidence from the Chinese real estate sector, which is notorious for pervasive rent-seeking and corruption.

Posted by at 12:15 PM

Labels: Global Housing Watch

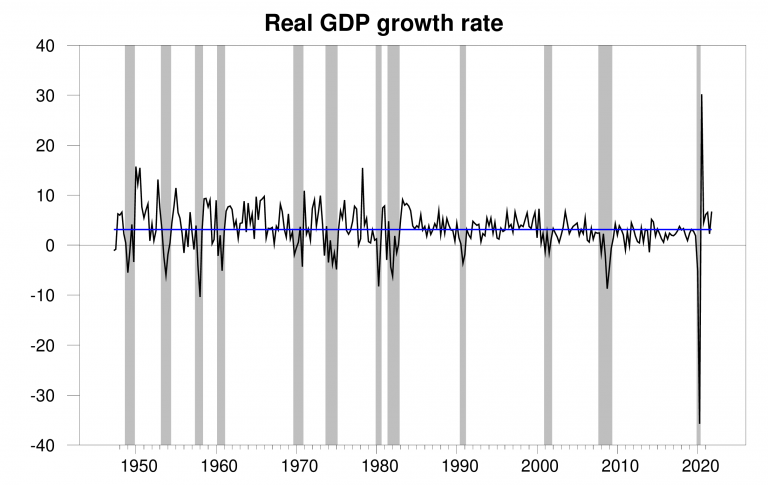

GDP almost back to potential

From Econbrowser:

“The Bureau of Economic Analysis announced today that seasonally adjusted U.S. real GDP grew at a 6.9% annual rate in the fourth quarter, more than twice the average growth rate the U.S. has seen since World War II.

The new data put the Econbrowser recession indicator index at 1.2%, historically a very low value and signalling an unambiguous continuation of the economic expansion. The number posted today (1.2%) is an assessment of the situation of the economy in the previous quarter (namely 2021:Q3). We use the one-quarter lag to allow for data revisions and to gain better precision. This index provides the basis for an automatic procedure that we have been implementing for 15 years for assigning dates for the first and last quarters of economic recessions. As we announced a year ago, the COVID recession ended in the second quarter of 2020. The NBER Business Cycle Dating Committee subsequently made the same announcement in July.

Continue reading here.

From Econbrowser:

“The Bureau of Economic Analysis announced today that seasonally adjusted U.S. real GDP grew at a 6.9% annual rate in the fourth quarter, more than twice the average growth rate the U.S. has seen since World War II.

The new data put the Econbrowser recession indicator index at 1.2%, historically a very low value and signalling an unambiguous continuation of the economic expansion.

Posted by at 12:13 PM

Labels: Macro Demystified

Subscribe to: Posts