Friday, January 28, 2022

China: Downside Risks from Property Developer Stress

From the IMF’s latest report on China:

“One of China’s largest property developers, Evergrande, has begun restructuring talks with offshore creditors to alleviate rising financial stress following a tightening of regulations to rein in the highly-leveraged real estate sector. Funding pressures have since spread to other property developers, posing concerns of negative spillovers to the broader economy and global markets.2 The authorities have the policy space and tools to contain these risks but will have to balance difficult trade-offs between financial stability and moral hazard. Over the long term, deeper structural reforms are needed to comprehensively address the risks from China’s property market.

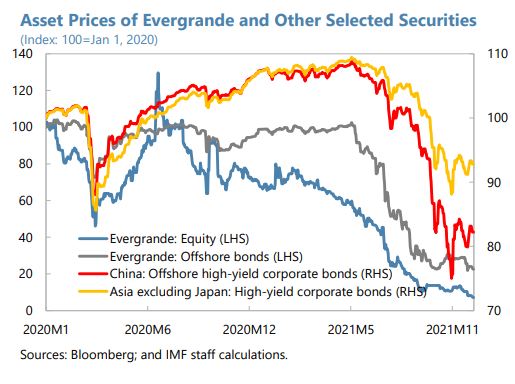

Evergrande, one of China’s largest property developers, has entered restructuring negotiations amid severe funding strains. With over US$300 billion in liabilities to creditors, suppliers, and households, the company’s bond prices are trading at distressed levels. So far, contagion has spread mostly to other financially weak developers and lower-rated corporates in China, with limited impact on higher-rated developers. Markets in and outside of China initially reacted strongly to Evergrande’s stress but subsequently stabilized following actions by the authorities to limit wider spillovers.

Evergrande’s troubles follow a broad regulatory campaign to rein in China’s highly leveraged real estate sector. Property plays a large role in both China’s economy and financial system, accounting for about a quarter of both total fixed investment and bank lending over the past 5 years before the pandemic. On the demand side, the property sector’s importance reflects massive household savings—linked, in part, to the inadequate social protection system (see Box 2)—and limited alternative investment options. After allowing private housing investment to function as a key countercyclical policy tool in the aftermath of the Global Financial Crisis, including through a significant run-up in leverage, the authorities have repeatedly sought to rein in the property sector owing to financial stability concerns. They redoubled these efforts after the initial recovery from last year’s national pandemic lockdown, including by imposing tougher restrictions on new funding for developers.

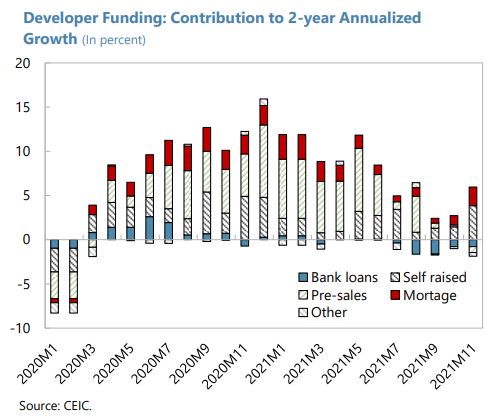

New controls on developer credit bring to the fore concerns over the potential for intra-sector contagion. Like Evergrande, many property developers are also highly leveraged, with weak earnings and liquidity. Many developers are also exposed to inadequately disclosed risks, like sizeable but opaque off balance sheet risks from guarantees and joint ventures. The sector’s growing dependence on pre-sales of unfinished housing as a source of funding—now over one-third, up from 25 percent in 2014—increases its vulnerability to sector-wide confidence shocks and runs.3 Some of this revenue is not properly escrowed, a risky practice which increases leverage and makes households creditors, despite their limited ability to monitor the risks of these loans. The failure to complete unfinished housing inventory by defaulting developers not only undermines consumer confidence, but also risks lowering households’ willingness to buy homes via pre-sales with other developers, propagating liquidity strains within the sector. These vulnerabilities are compounded by survey-based evidence that points to high price-to-income ratios in various cities.

These vulnerabilities could potentially lead to a broader credit crunch among developers, raising risks

of a downside scenario engulfing the wider real estate sector:• Developer funding pressures could spill over to property prices if housing demand slumps or distressed developers are forced to sell inventories at a discount, reinforcing contagion within the sector.

• Falling prices and increasing construction delays could halt pre-sales and trigger a sharp retrenchment of housing demand by households generally, further amplifying financial stress for property developers.

• At this point, the financial system might be affected, causing credit supply to contract for developers and households alike. While banks’ loan exposure to Evergrande is not systemic, lending to real estate firms represents 7 percent of total lending, residential mortgages are another 21 percent, and a large share of other bank loans are collateralized by property. In addition, banks are highly exposed to non-bank financial institutions, which in turn hold large exposures to developers and other land-exposed firms. Trusts, a type of NBFI, have financed between 16-22 percent of the rapidly growing real estate investment in China over the last four years.

A sharper-than-expected slowdown in the property sector could trigger a wide range of adverse effects on aggregate demand, with feedback loops to the financial sector. Domestically, this could include a sharp retrenchment of real estate investment, which in 2020 accounted for an estimated 8.7 percent of GDP. This would have knock-on effects on other private investment as the real estate sector accounts for 11 percent of total purchases of intermediate materials. Moreover, local governments may be forced into unwanted fiscal consolidation as revenues from land sales fall. And a sustained fall in house prices would likely weigh on private consumption, through weaker income and employment (construction represents 13 percent of total employment) and wealth effects (80 percent of households own their homes).

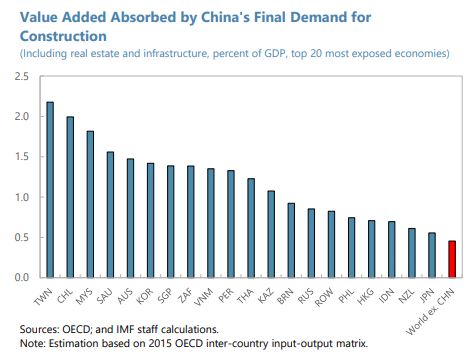

A sudden slowdown in China’s growth would create spillovers through trade and commodity prices. Model-based simulations of a decline in investment in China due to financial stress suggest that a one percent decline in China’s output lowers growth in the rest of the world by about one-tenth of a percent (Dizioli and others, 2016). While real estate investment is less trade-intensive than other investment, direct and indirect trade exposures from the rest of the world are still sizeable. Foreign value added in China’s construction sector (including both real estate and infrastructure) accounts for 0.5 percent of global (excl. China) GDP, with larger exposures for some Asian and commodity exporting economies. China’s final demand in the construction sector absorbs a sizeable fraction of global value added in basic metals (14 percent), mining (6 percent) and oil and chemicals (5 percent) sectors

Financial spillovers would mostly operate via a deterioration in global risk appetite. While direct nonresidents’ holdings of Chinese financial assets have grown in recent years as a result of the inclusion of China in global benchmark indexes, with property developers being active issuers in offshore bond markets (US$200 billion of outstanding bonds), direct exposures to China remain relatively small. However, given strong trade related spillovers, global risk appetite would likely be affected, which could lead to tighter financial conditions, especially in emerging markets (GFSR, Apr, 2016). The policy response to property developer stress necessarily involves difficult trade-offs. In the short term, authorities have the policy space and tools to limit disorderly spillovers within the financial sector and lessen any adverse impact on the economy. The timing and extent of support, however, must balance the need to avert destabilizing confidence shocks with the imperative to minimize backtracking in efforts to curb moral hazard and contain leverage. Key elements of a policy response should include:

• Guarding against systemic contagion: For now, the priority should be to contain large-scale spillovers to housing demand and economic activity while still allowing market forces to reduce vulnerabilities. This requires intensifying risk monitoring efforts, strengthening the central government’s coordinating role in policy responses, and facilitating the restructuring of troubled developers while ensuring the timely completion of pre-sold housing inventories.

• Dealing with escalating risk: if large-scale spillovers to housing markets threaten economic and financial stability, bolder steps will be needed including government backstops for liquidity provision to stressed developers and guarantee mechanisms for completion of presold housing. These measures should be temporary and subject to strict safeguards to minimize moral hazard (see below). Decisive macroeconomic easing would protect against shortfalls in aggregate demand.

• Addressing structural shortcomings. As soon as risks recede, ensuring property sector risks decline to safer levels will require curbing risks from pre-sales practices, introducing property taxes, and other measures to ease investment-related housing demand and reduce local government incentives to boost property markets.”

Posted by at 12:09 PM

Labels: Global Housing Watch

Subscribe to: Posts