Thursday, January 27, 2022

Younger generations and the lost dream of homeownership

From a VoxEU post by Gonzalo Paz-Pardo:

“Homeownership among younger households has been decreasing in several major advanced economies. This column shows that increases in labour income inequality and uncertainty are key drivers of this trend. Confronted with high house prices and low, risky incomes, many young households cannot or do not want to risk making such a big, illiquid investment. As a result, they accumulate less wealth.

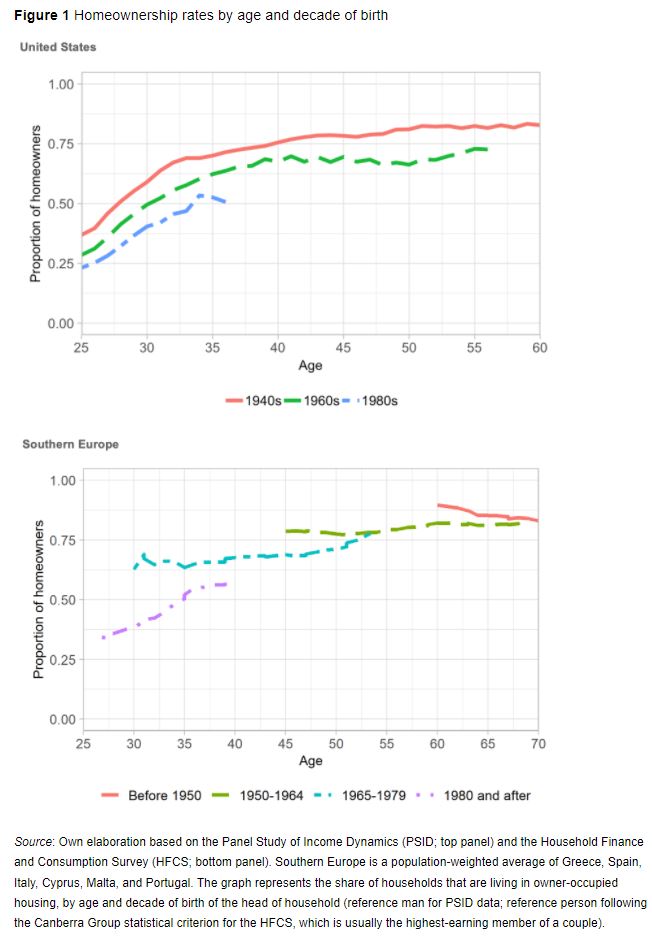

Figure 1 shows that, in the US, younger generations are less likely to be living in their own homes than older generations were at the same age. Among households headed up by someone born in the 1940s, 70% owned their homes by age 35. This figure dropped to 60% for those born in the 1960s and about 50% for the early ‘millennials’ born in the 1980s. In southern Europe, too, homeownership rates at age 35 have dropped – by over 10 percentage points when comparing those born from 1965 to 1979 with those born in the 1980s. At the same time, young people are taking longer to leave the parental home and live independently (Becker et al. 2008).

Homeownership is a frequent subject of political debate. Owning a house is crucial for the wealth accumulation of most households (Paz-Pardo 2021), and housing plays a role in a well-diversified portfolio (Chetty et al. 2017). Shutting young people out of housing markets may distort their marriage and childbearing decisions (Laeven and Popov 2017), and homeownership rates relate directly to the strength of local communities, social capital, and political engagement (Glaeser et al. 2002, Rohe et al. 2002).

What has driven these changes? To identify the key factors, I build a model of homeownership and portfolio choice over the life cycle with a rich structure of risks (Paz-Pardo 2021). According to the model, it’s not about younger generations not wanting to buy their homes anymore: changes in the economic environment fully explain the magnitude of the drop in homeownership rates.”

From a VoxEU post by Gonzalo Paz-Pardo:

“Homeownership among younger households has been decreasing in several major advanced economies. This column shows that increases in labour income inequality and uncertainty are key drivers of this trend. Confronted with high house prices and low, risky incomes, many young households cannot or do not want to risk making such a big, illiquid investment. As a result, they accumulate less wealth.

Figure 1 shows that,

Posted by at 10:51 AM

Labels: Global Housing Watch

Wednesday, January 26, 2022

Housing Market in France

From the IMF’s latest report on France:

“Risks from real estate markets require continued vigilance. Over the last decade, household debt grew steadily from just below 60 percent to over 100 percent of disposable income and debt service to disposable income (DSTI) has increased. The deterioration reflects in part the need for higher debt to cover increasing housing prices, resulting in higher LTVs. Consequently, in 2019, the ESRB issued a warning related to medium-term vulnerabilities in the real estate sector, citing higher prices, weaker lending standards, elevated household debt, and rapid mortgage lending growth in France. While supervisory action by the High Council for Financial Stability (HCSF) has capped the deterioration in lending standards, low interest rates, a relatively inelastic housing supply and increased demand for home renovations continued to fuel real estate price growth in 2020 and 2021.

Several features in France can attenuate risks from market corrections to mortgage defaults, but banks’ profits could be at risk. Household repayment risks are contained because, among other factors, mortgage interest rates are fixed, and employment losses are protected by unemployment insurance. Banks are partially protected from potential losses predominantly through mortgage insurance, and borrowers’ legal obligations. However, profit margins on housing loans are estimated to be nil or even negative since 2017. Thus, the large volume of mortgages with long residual maturity and low fixed interest rate creates a persistent risk to bank profitability, which would intensify with selected defaults or increased funding costs of banks.

(…)

To limit excessive risk-taking by banks, borrower-based measures should be maintained and expanded. To shield banks from loan losses, the HCSF issued recommendations (declared legally binding as of January 1, 2022) that banks must limit mortgage length to 25 years and DSTI to 35 percent (up from 33 percent in the guidance)—with up to 20 percent of new mortgage loans excluded primarily for owner-occupied housing. As a result, banks have actively adjusted their lending practices, with falling DSTI. As of August 2021, the banking sector was within the flexibility margin. However, fueled by low interest rates and a relatively inelastic housing supply, house prices continued to increase and mortgage debt-to income remains elevated, reflecting the need to cover increasing housing prices. In addition, downside risks from structural factors remain, such as weak banking sector profitability due to persistently low rates and high cost-to-income ratios, banks’ high market risk exposure, wholesale funding risk, cyber security, and climate change risks. If these trends continue, fine tuning existing borrower-based measures or deploying complementary measures, such as the now available (sectoral) systemic risk buffer, may become appropriate to more broadly limit excessive risk-taking.”

From the IMF’s latest report on France:

“Risks from real estate markets require continued vigilance. Over the last decade, household debt grew steadily from just below 60 percent to over 100 percent of disposable income and debt service to disposable income (DSTI) has increased. The deterioration reflects in part the need for higher debt to cover increasing housing prices, resulting in higher LTVs. Consequently, in 2019, the ESRB issued a warning related to medium-term vulnerabilities in the real estate sector,

Posted by at 10:07 AM

Labels: Global Housing Watch

Keeping Public Debt Sustainable in an Equitable Way

Source: CESifo

In a new paper (2022), economists Davide Furceri, Prakash Loungani, Jonathan D. Ostry, and Pietro Pizzuto write about the challenges of ensuring sustainable levels of debt in the face of threats of rising inequality, low growth, and high unemployment, posed by the COVID-19 crisis.

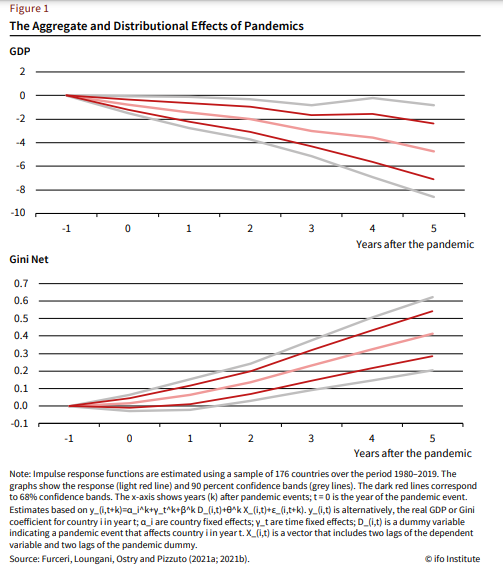

Studying five major epidemics since the 2000s, they demonstrate that real GDP falls in the aftermath of a pandemic while inequality (as measured by the Gini coefficient) shoots up (Figure 1). Subsequently, they discuss the role of fiscal policy in managing inequality and the need to avoid hastening or prolonging generous support beyond need using appropriate policy measures.

Source: CESifo

In a new paper (2022), economists Davide Furceri, Prakash Loungani, Jonathan D. Ostry, and Pietro Pizzuto write about the challenges of ensuring sustainable levels of debt in the face of threats of rising inequality, low growth, and high unemployment, posed by the COVID-19 crisis.

Studying five major epidemics since the 2000s, they demonstrate that real GDP falls in the aftermath of a pandemic while inequality (as measured by the Gini coefficient) shoots up (Figure 1).

Posted by at 9:53 AM

Labels: Inclusive Growth

Tuesday, January 25, 2022

Book Review- Desperately Seeking Shahrukh

By: Vrinda Saxena

‘I think we know very little about the changing lives of young women in India because we have stopped studying them for who they are. We know the heroines- the ones who fought against all odds and became leaders, and we know the victims. But the real change is taking place in between- the ordinary women who are dressing differently, who are spending more hours in school than ever before, who are reshaping the rules at home in their marriages, in their relationships with peers, in their relationships with their in-laws and their relationships with the working world.’

– Yamini Aiyar, President, Centre for Policy Research

For the book ‘Desperately Seeking Sharukh’ (2021)

Jostling between datasets and academic theories, summary measures and aggregates, the journey to tap into the elusive story of gender and deprivation in India has not been an easy task for economists through the ages. Perhaps, in what could be loosely referred to as a case of inferential statistics, author and World Bank economist Shrayana Bhattacharya has captured stories of diverse women across various social and economic strata of the country to paint a larger picture of the state of affairs in her book, Desperately Seeking Sharukh: India’s Lonely Young Women and the Search for Intimacy and Independence.

In Bhattacharya’s own words, the book uses the “construct” of the Hindi film actor, Shahrukh Khan, as a research device to closely peer into the personal lives of migrant women, domestic workers, corporate and public servants, and even urban non-working women. For nearly 14 arduous years from 2006 onwards, she broached conversations with her research respondents, acquaintances, and strangers on mutual love for the actor, realizing over time how each discussion was deeper than just a description of his work and off-stage persona but a close peek into women’s own aspirations and changing beliefs. The reader gets an up-close glimpse into how Indian women perceive work, wages, social mobility, economic aspirations, employment, and other seemingly personal issues, like intimacy, loneliness, bargaining power within families, dignity, etc.

As a case in point, the book’s first composite character- an upper-class working woman residing in an Indian metro, with a fine education and a well-paying job- peruses over the perils of succeeding in a predominantly male corporate setup, building one’s own fortune in the absence of land and generational wealth like a true “middle class”, and the freedom and perils of not pegging one’s identity to men or marriage. Brilliantly putting it into context, Bhattacharya equips the reader with 6 frameworks within which “middle class” has been defined by economists and how deep the income and wealth inequality fault lines run in the country. Where women’s access to education and employment are as strongly guarded as their ability to access public spaces and even entertainment- in that India she follows the lives of some women who managed to break through from a few shackles but get held back on others. The “hidden tax”, as economist Sendhil Mullainathan terms it, by refusing to acknowledge women’s economic successes or social ostracization forms the underlying theme of many such stories. One is left to ponder then if all the loneliness and unrequited emotional labor women perform in their personal relationships are not personal misgivings but the gift of a structurally unequal society! Besides, not only does this inequality maim women’s minds and bodies but spills over to numbers and data that economists love most. Bhattacharya takes the reader on a very thought-provoking journey into the lives of women who are majorly, if not solely, invested severely into performing unpaid care work for families but are ironically never accounted for in the economy. This and other ways official data upholds patriarchal dominance by neglecting home-based workers and informal laborers hits you hard each time the same data is invoked as the sole basis on which an understanding of deprivation hinges.

Shahrukh- the superstar who publicly claimed his rags to riches story, publicly admitted to building from scratch and battling feelings like loneliness and anxiety, and also publicly acknowledged the important role women played in his real-life aside from the reel life where his romances are categorized as more ‘interactive’ than of all others, is the combining glue for this oeuvre. Female fans who were interviewed displayed analogous revolutions in their own lives- from sacrificing traditional marriages and roles of damsels in distress for the joys and trials of independent economic life, reclaiming their right over consumption of entertainment and education, or even something that may seem as trivial as making a ‘pilgrimage’ to their icon’s bungalow without male company (yes, in India that is a big deal!).

Thus, in “seeking” Shahrukh, the many women who feature in this book show how with the help of technology, the economic liberalization of India in the 1990s, and the advent of social media India’s young women are slowly departing from the idea of marrying their Shahrukh(s) to becoming their own Shahrukh(s).

Discussions on cultural beliefs, aspirations, norms, and the things that catch the fancy of communities elude very many narratives of the development and evolution of emerging markets. This book fits right in to bandage that void. From the way urban, working women mirrored their fantasies of companionship that is more emotionally and financially equal to rural and immigrant women’s windows into the world outside, this book communicates the changing everyday dynamics of women’s engagement in economies by deconstructing a superstar’s fandom. Pardon me if my review does not appear academic enough- for even the book is not. It steers clear of any dry statement of facts and figures but rather attempts to put them into perspective and uncover the three-dimensional story behind.

By: Vrinda Saxena

‘I think we know very little about the changing lives of young women in India because we have stopped studying them for who they are. We know the heroines- the ones who fought against all odds and became leaders, and we know the victims. But the real change is taking place in between- the ordinary women who are dressing differently, who are spending more hours in school than ever before,

Posted by at 1:59 PM

Labels: Book Reviews, Inclusive Growth

The triple impact of school closures on educational inequality

Source: VoxEU CEPR

“Education, then, beyond all other devices of human origin, is the great equalizer of the conditions of men, the balance wheel of the social machinery.”

-Horace Mann, 1848

Quite ironically, however, the pandemic-induced school closures and other aspects of remote education pose the threat of deep and long-lasting inequalities. This column argues that channels operating through schools, peer effects, and parental investments have all contributed to massively growing educational inequality during the Covid-19 crisis. Among 9th graders, children from low-income neighborhoods in the US are predicted to suffer a learning loss equivalent to almost half a point on the four-point GPA scale, whereas children from high-income neighborhoods remain unscathed.

Source: VoxEU CEPR

“Education, then, beyond all other devices of human origin, is the great equalizer of the conditions of men, the balance wheel of the social machinery.”

-Horace Mann, 1848

Quite ironically, however, the pandemic-induced school closures and other aspects of remote education pose the threat of deep and long-lasting inequalities. This column argues that channels operating through schools, peer effects, and parental investments have all contributed to massively growing educational inequality during the Covid-19 crisis.

Posted by at 1:52 PM

Labels: Inclusive Growth

Subscribe to: Posts