Thursday, January 27, 2022

Housing Market in Czech Republic

From IMF’s latest report on Czech Republic:

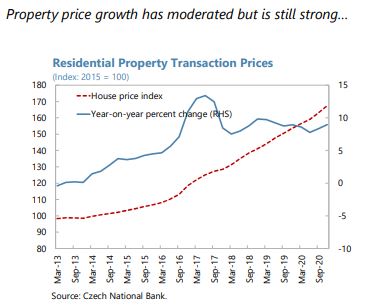

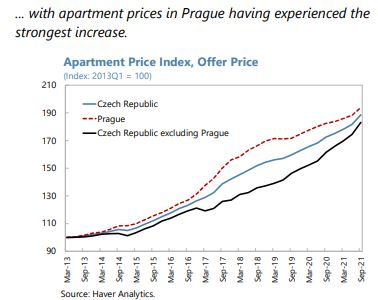

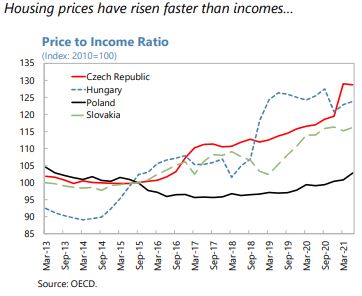

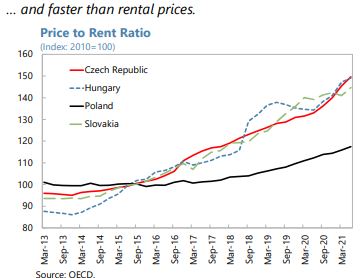

“Amid robust mortgage credit growth, property price-growth significantly accelerated from already elevated levels stretching valuations and worsening affordability. Property prices grew by about 8½ percent in 2020, down from about 9¼ percent in 2019, but accelerated to 14½ percent y-o-y in 2021:Q2. The Czech Republic has experienced one of the highest property price appreciation rates in the EU, reaching a cumulative growth rate of about 54 percent in the five years prior to 2021. The CNB estimates property prices to be overvalued by 25 percent on average (as of mid-2021). The steep property price increase has deteriorated affordability as reflected in price-to-income and price-to-rent ratios.

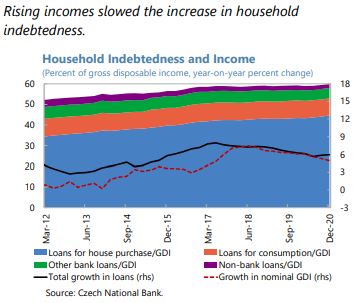

Macrofinancial vulnerabilities due to increasing risk-taking by lenders amid growing household leverage and high and rapidly rising property valuations warrant close monitoring. Although aggregate household indebtedness is still low compared to other EU countries, it increased robustly by 2½ percentage points to 34 percent of GDP during 2020. Fast increases in property prices, amid loosening credit standards and macroprudential policy during the pandemic, resulted in households/lenders taking larger and riskier mortgages (…). Significant increases in risk taking, in an environment of high and rapidly rising house prices, exposes households to price and interest rate shocks that could harm those who purchased in overvalued areas, who are highly levered, or low-income households—for which debt service is already burdensome. These vulnerabilities might be compounded by the large proportion of mortgages with fixation periods up to five years.

Recent developments warrant tightening prudential tools while deploying coordinated housing supply and tax policies. Properly calibrated income-based measures can improve risk taking incentives and support affordability. Staff welcomes the CNB’s decision in November 2021 (effective from April 2022) to tighten limits on mortgage loan ratios as follows: DTI (8.5), DSTI (45 percent) and LTV (80 percent). Close monitoring of market developments is necessary with a potential for further tightening down the road. Importantly, clear communication of macroprudential policy actions and adequate coordination of the overall policy mix are key to ensure a smooth stabilization. Proper calibration of macroprudential tools for lower risk groups—first-time home buyers and low-levered households—is warranted to safeguard proper access to financing. An improved risk-based prudential framework (Section D) could be combined with the macroprudential setup to facilitate calibration of these measures.

Housing Supply

Pre-existing housing supply shortages persisted throughout the pandemic, partly reinforced by temporary pauses in construction activity. A new construction law, aimed at simplifying the construction code and the reportedly cumbersome permitting process, through creation of a one-stopshop for construction companies, was adopted in July, 2021 but implementation of some of its provisions will take until 2023. The impact on the number of granted residential building permits has been limited so far.

Tax Policy

Revenues from property taxes are low in comparison to other countries and will further fall after the recent cancellation of the property transaction tax. Real estate property taxation should be based on current market valuations and not on floor space. While the recent reduction of the maximum deductible amount of mortgage interest from CZK 300,000 to CZK 150,000 per year starting in 2021 is welcome, this benefit could be eliminated completely as in other countries.

Staff welcomes the recent reform of the macroprudential framework that provides the CNB with the legal powers to implement macroprudential policy. In July 2021, the CNB was given powers to make macroprudential limits legally binding, which is consistent with international best practice.

Authorities’ Views

The authorities acknowledge the risks stemming from the heated property market and stand ready to tighten macroprudential policies as needed. They acknowledged the increasing risk taking by households amid high and rapid house price growth and stand committed to closely monitor market developments to decide on further policy actions. On the basis of new statutory powers, the CNB Bank Board decided on November 25, 2021 to reintroduce limits on DTI and DSTI ratios and to tighten the LTV limit.”

Posted by at 11:12 AM

Labels: Global Housing Watch

Subscribe to: Posts