Friday, December 13, 2019

Housing View – December 13, 2019

On cross-country:

- Q3 2019: The global house price boom continues strong, especially in Europe, but sharp slowdown in North America, the Middle East and some parts of Asia-Pacific – Global Property Guide

- Prime Global Cities Index Q3 2019 – Knight Frank

On the US:

- Bold Predictions for 2020: Shrinking Homes and a More Stable Market – Zillow

- These Housing Markets Could Heat Up (Podcast) – Bloomberg

- Fix California’s Housing Crisis, Activists Say. But Which One? – Citylab

- A Modest Proposal: How Even Minimal Densification Could Yield Millions of New Homes – Zillow

- Mapping America’s Metropolitan Growth: Islands of Density in a Sea of No Growth – Zillow

- Home Purchase Sentiment Rebounds in November, Re-Approaches Survey High – FannieMae

- Home Equity in Retirement – Philadelphia Fed

- Owner-Occupancy Fraud and Mortgage Performance – Philadelphia Fed

- Opinion: To solve the problem of unaffordable entry-level housing, abolish single-family zoning – MarketWatch

- Vouchers can help the poor find homes. But landlords often won’t accept them. – VOX

- Fannie and Freddie Need Fixing — Urgently: A Response to Joe Nocera – Cato Liberty

- Release: New Carpenter Index developed by AEI Housing Center – American Enterprise Institute

- “Decommodifying” Housing and Other Magical Thinking – E21

- Tenants are winners in Manhattan’s oversupplied luxury home market – Financial Times

On other countries:

- [China] China’s Housing Market Goes the WeWork Way—and Thousands Get Evicted – Wall Street Journal

- [Israel] Does Location Matter? Evidence on Differential Mortgage Pricing in Israel – Bank of Israel

- [Lithuania] Lithuania’s modest house prices increase – Global Property Guide

- [Netherlands] Netherlands’ house price growth slowly decreasing – Global Property Guide

- [Norway] Norway’s financial stability as risk from household debt, property prices -regulator – Reuters

*Please note that Housing View will be on hiatus for the next three weeks.

On cross-country:

- Q3 2019: The global house price boom continues strong, especially in Europe, but sharp slowdown in North America, the Middle East and some parts of Asia-Pacific – Global Property Guide

- Prime Global Cities Index Q3 2019 – Knight Frank

On the US:

Posted by at 5:00 AM

Labels: Global Housing Watch

Tuesday, December 10, 2019

Top Ten Posts of 2019

As 2019 draws to a close, below is our list of the top ten blogs of the year.

- Housing Market in Sweden

- Housing View – January 3, 2019 [2019 AEA Annual Meeting Special Edition]

- Paul Cheshire on Urban Economics

- 2019 AEA’s papers on Inequality

- Housing Market in Malta

- 2019 AEA’s papers on Energy and Climate Change

- Housing Market in Finland

- Understanding Housing Supply: Views from Jenny Schuetz

- Inequality of Opportunity, Inequality of Income and Economic Growth

- Daniel Hamermesh: How Do People Spend Time?

Photo by Colton Duke

As 2019 draws to a close, below is our list of the top ten blogs of the year.

- Housing Market in Sweden

- Housing View – January 3, 2019 [2019 AEA Annual Meeting Special Edition]

- Paul Cheshire on Urban Economics

- 2019 AEA’s papers on Inequality

- Housing Market in Malta

- 2019 AEA’s papers on Energy and Climate Change

- Housing Market in Finland

- Understanding Housing Supply: Views from Jenny Schuetz

- Inequality of Opportunity,

Posted by at 11:17 AM

Labels: Uncategorized

Paul Volcker: 1927-2019

From Conversable Economist:

“Paul Volcker, who was chair of the Federal Reserve from August 1979 to August 1987.has died. He is generally credited, or in some cases blamed, for the set of monetary policies which both ended the inflationary period of the 1970s but also brought on the very deep double-dip recessions of 1980 and 1981-2. The New York Times obituary is here.

For an overview of those times and how Volcker perceived the choices he was facing, a useful starting point is “An Interview with Paul Volcker,” conducted by Martin Feldstein, which appeared in the Fall 2013 issue of the Journal of Economic Perspectives. Here’s a flavor:

It made a profound impression on me, if nobody else, that Arthur Burns titled his valedictory speech “The Anguish of Central Banking” (Burns 1979). That was a long lament about how, in the economic and political setting of the times, the Federal Reserve, and by extension presumably any central bank, could not exercise enough eserve, and by extension presumably any central bank, could not exercise enough restraint to keep inflation under control. It was a pretty sad story. If you were going to follow that line, you were going to give up, I guess. I didn’t think you could give up. If I was in that job, that was the challenge as the Chairman of the Federal Reserve. You inherit a certain challenge …

The favorite word at the time, which was very popular within the Federal Reserve, but I think popular in the academic community generally, was “gradualism.” I don’t quite remember them saying, “Don’t bring it down at all.”But instead, it was “Take it easy. It will be a job of, I don’t know, years, decades, whatever, and you can do it without hurting the economy.” I never thought that was realistic. The inflationary process itself brought so many dislocations, and stresses and strains that you were going to have a recession sooner or later.”

Continue reading here.

From Conversable Economist:

“Paul Volcker, who was chair of the Federal Reserve from August 1979 to August 1987.has died. He is generally credited, or in some cases blamed, for the set of monetary policies which both ended the inflationary period of the 1970s but also brought on the very deep double-dip recessions of 1980 and 1981-2. The New York Times obituary is here.

For an overview of those times and how Volcker perceived the choices he was facing,

Posted by at 11:04 AM

Labels: Profiles of Economists

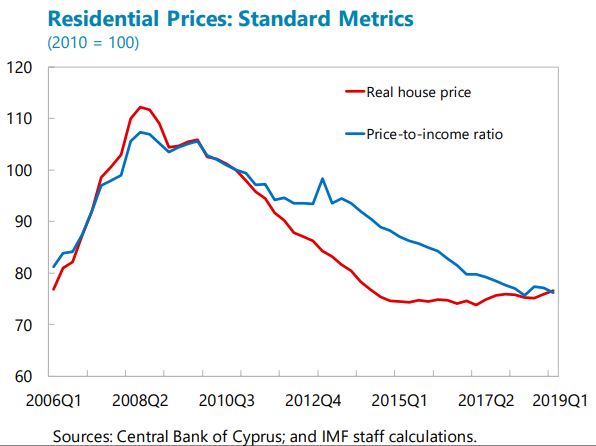

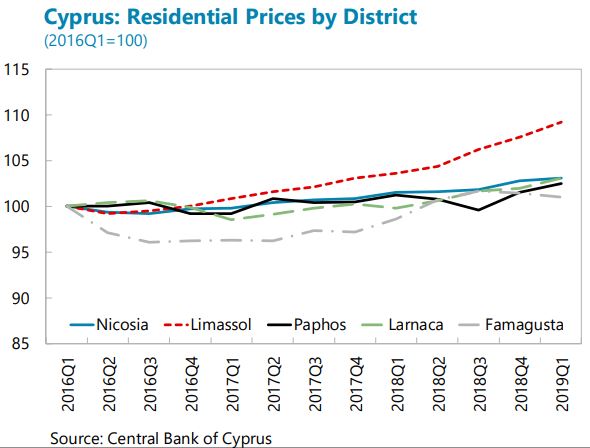

Housing Market in Cyprus

From the IMF’s latest report on Cyprus:

“Property prices are rising gradually but unevenly across markets (…). Rising demand for housing and business offices is being met with increasing supply from new construction, as evidenced by the rising issuance of building permits, and release of repossessed collateral properties by banks. Real estate holdings by banks, CACs and investment funds have also increased. Overall residential prices grew by 2.7 percent (yoy) in 2019:Q1 while sales transactions rose by nearly 6 percent during 2018.14 The property market remains highly segmented, however, with higher price increases observed primarily in a growing luxury segment in some coastal areas (e.g., Limassol), fueled by the CIP-linked demand from non-residents, with limited spillovers to other segments so far. Rents have been rising rapidly—17 percent in 2018— mainly driven by the growing demand from foreign students and lagging supply of rental property investments, prompting the authorities to increase rental and housing subsidies and a range of incentives for developers to increase supplies of affordable housing and rental properties.

Macro-financial risks from the property market appear limited now but warrant close monitoring. While the sales of repossessed collateral properties by banks and CACs could potentially depress prices, downward pressures from such sales have not been evident in any market segments. However, it is important to continue monitoring sectoral and regional real estate market developments, considering the segmented nature of the market. Macroprudential measures tailored to the market segment should be undertaken if warranted, e.g. if the luxury sales become associated with rapid credit growth or high loan-to-value ratios. On the supervisory front, continued monitoring is needed on the large holdings of repossessed real estate by banks and CACs, to discourage and limit the risk of excessive holding of foreclosed properties. Also, the increased real estate holding by investment funds warrants close monitoring to mitigate risks related to liquidity mismatches. Supervisory tools, in particular Pillar 2 requirements and explicit bank-specific objectives, should continue to be used to discourage excessive holding of foreclosed properties by banks.”

From the IMF’s latest report on Cyprus:

“Property prices are rising gradually but unevenly across markets (…). Rising demand for housing and business offices is being met with increasing supply from new construction, as evidenced by the rising issuance of building permits, and release of repossessed collateral properties by banks. Real estate holdings by banks, CACs and investment funds have also increased. Overall residential prices grew by 2.7 percent (yoy) in 2019:Q1 while sales transactions rose by nearly 6 percent during 2018.14 The property market remains highly segmented,

Posted by at 11:01 AM

Labels: Global Housing Watch

Monday, December 9, 2019

China’s Productivity Convergence and Growth Potential—A Stocktaking and Sectoral Approach

Interesting research paper by Min Zhu , Longmei Zhang and Daoju Peng:

“China’s growth potential has become a hotly debated topic as the economy has reached an income level susceptible to the “middle-income trap” and financial vulnerabilities are mounting after years of rapid credit expansion. However, the existing literature has largely focused on macro level aggregates, which are ill suited to understanding China’s significant structural transformation and its impact on economic growth. To fill the gap, this paper takes a deep dive into China’s convergence progress in 38 industrial sectors and 11 services sectors, examines past sectoral transitions, and predicts future shifts. We find that China’s productivity convergence remains at an early stage, with the industrial sector more advanced than services. Large variations exist among subsectors, with high-tech industrial sectors, in particular the ICT sector, lagging low-tech sectors. Going forward, ample room remains for further convergence, but the shrinking distance to the frontier, the structural shift from industry to services, and demographic changes will put sustained downward pressure on growth, which could slow to 5 percent by 2025 and 4 percent by 2030. Digitalization, SOE reform, and services sector opening up could be three major forces boosting future growth, while the risks of a financial crisis and a reversal in global integration in trade and technology could slow the pace of convergence.”

Interesting research paper by Min Zhu , Longmei Zhang and Daoju Peng:

“China’s growth potential has become a hotly debated topic as the economy has reached an income level susceptible to the “middle-income trap” and financial vulnerabilities are mounting after years of rapid credit expansion. However, the existing literature has largely focused on macro level aggregates, which are ill suited to understanding China’s significant structural transformation and its impact on economic growth.

Posted by at 1:57 PM

Labels: Inclusive Growth

Subscribe to: Posts