Friday, March 1, 2019

Housing Market in Malta

From the IMF’s latest report on Malta:

“Rapidly rising house prices and rents may eventually pose financial stability risks while putting some vulnerable households at risk of poverty. Policies that help mitigate the rapid increase of house prices and make rents more affordable while strengthening households and banks’ balance sheets should be encouraged.

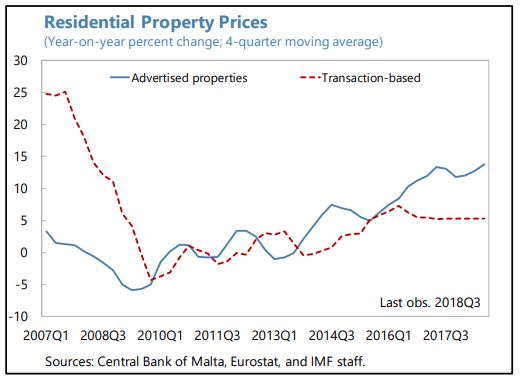

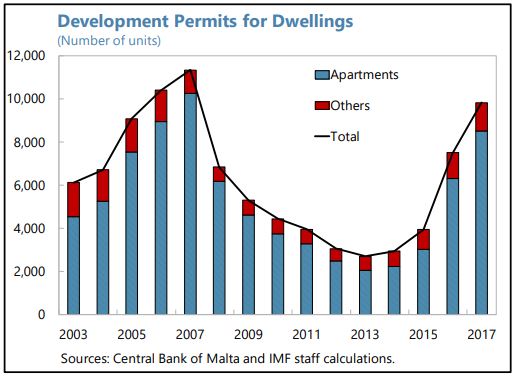

Strong demand for housing has continued to push up property prices. While some signs of overvaluation have started to emerge, recent house price trends can largely be explained by fundamentals such as e.g., strong immigration flows, rising disposable income, portfolio rebalancing towards property investment and a delayed supply response. Other factors such as the extension of the first-time home-buyer stamp duty relief, the reduced tax rate on rental income, surging demand for tourist accommodation and, for the high-end segment, the IIP may also have played a role (but are not directly controlled for in the empirical analysis conducted in Annex I).

Banks’ exposure to housing-market-related risks is high and increasing, and the introduction of macroprudential measures should proceed as planned. All the more so that households’ indebtedness is relatively high, low income households are vulnerable to housing price corrections and flexible interest rate on mortgages are prevalent.7 Against this backdrop, recent efforts to close data gaps (loan-level data collection) and the planned introduction of borrowerbased macroprudential measures such as caps to loan-to-value (LTV) ratios at origin, stressed debt service-to-income (DSTI) limits, and amortization requirements are steps in the right direction (see text table).

To be more effective, the new borrower-based measures could be refined in due course and exemptions to the LTV limit could be narrowed. To avoid excessive risk concentration, speed limits should be defined in terms of the total value of new loans, not in terms of the number of new loans, and speed limits for loans against secondary and buy-to-let properties, the likely most speculative segment, should be lowered as soon as concerns about any initial disruptions dissipate. Finally, the scope of the new borrower-based measures should be extended to also cover non-bank mortgage loans.

Rapidly rising housing costs are affecting vulnerable households. The government recently relaxed the eligibility requirements for rent subsidies, but the scheme should be periodically reviewed to ensure it remains targeted on low-income households. Further efforts should also be envisaged to accelerate the provision of social housing, including by fiscally incentivizing private investments.

Authorities’ Views

Rapidly rising property prices are viewed by the authorities as mainly reflecting economic fundamentals. Inflows of foreign labor and higher income in general are fueling housing demand. The authorities also see the impact of tax benefits for first and second-time home buyers, the reduced tax rate on rental income and the IIP as marginal. They stressed that the planned borrower-based macroprudential measures were carefully calibrated to have minimal market impact upon their introduction. The authorities have agreed that there is room for refinement, in due course, and emphasized that they can easily recalibrate the measures to mitigate financial stability risks emanating from the housing market in a timely and effective manner. The authorities also recognize the growing importance of making housing more affordable for vulnerable households. They emphasized the progressive nature of the new rent subsidy scheme. Projects are underway to increase the stock of social and affordable housing.”

Posted by at 10:52 AM

Labels: Global Housing Watch

Subscribe to: Posts