Tuesday, March 12, 2019

Housing Market in Malaysia

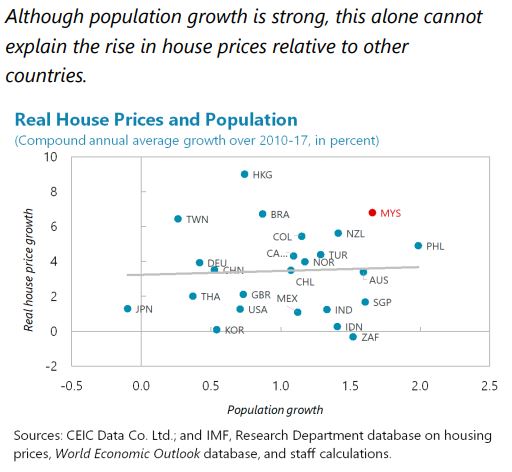

From the IMF’s latest report on Malaysia:

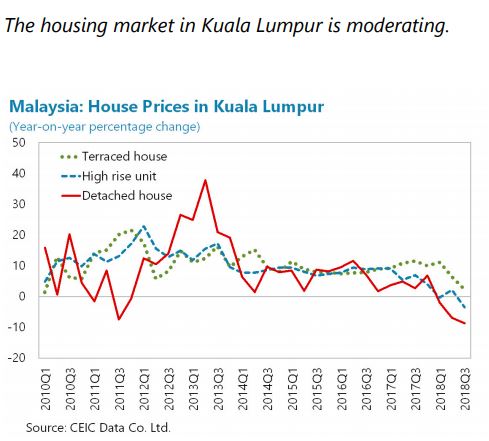

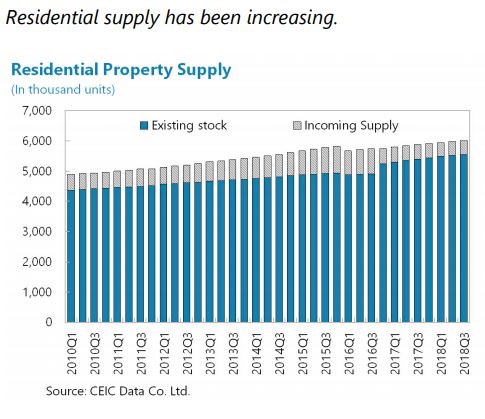

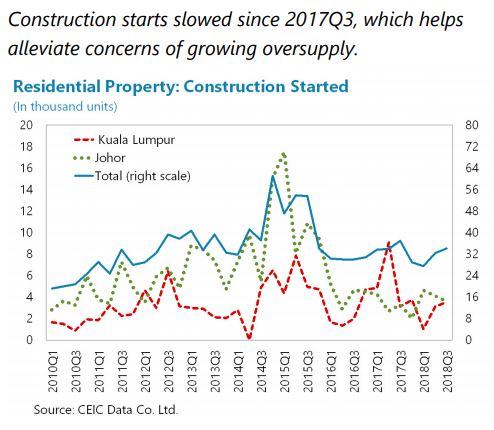

“The authorities continue to closely monitor risks emanating from the housing market, although the risks are deemed manageable (…). House price growth has declined from 6.5 percent in 2017 to 3 percent in 2018H1, and the volume of transactions has also declined. The number of unsold housing units that have been completed or are currently under construction is increasing and is mostly concentrated in high-rise buildings. Banks’ direct exposure to developers remain small and is closely monitored by the BNM. According to BNM stress tests, potential bank losses originating from a possible sharp real estate price adjustment and shocks to income and interest rates are small relative to the banks’ capital buffers. The BNM, MOF, and Ministry of Housing and Local Government have introduced new measures that help reduce the cost of property or of contracting a mortgage loan, with the objective to strengthen the demand for housing and facilitate leasing, and therefore gradually reduce the supply overhang. The impact of these measures should be evaluated on an ongoing basis to ensure effectiveness and correct potential distortions.

As systemic risks from the housing market dissipate, the residency-based differentiation in the real estate measures introduced in 2014 should be gradually phased out. Given banks’ sizable exposure to mortgage lending and to the construction industry, a real estate market price correction, through a reduction in household and corporate wealth, and these agents’ debt servicing capacity, could have a significant impact on growth and financial stability as NPLs rise. During 2012–13, the Malaysian House Price Index (MHPI) grew by a cumulative 24 percent, well-above its long-run annual average of 6 percent and, in 2014, amid further significant price increases, the number of transactions by non-citizens surged by 30 percent (…). The measures introduced in 2014 helped cool down the market (cutting growth in property purchases by non-citizens by over 50 percent in 2015 and by another 38.9 percent in 2016, and slowing the growth rate of MHPI to 9.4 and 7.4 percent in 2014 and 2015, respectively), avoid significant price adjustments, and reduce the rate of future debt build-up, thus reducing the probability of systemic distress. In the absence of a capital inflow surge for the time-being, but still high household leverage, gradually removing the residency-based differentiation in both measures is recommended as systemic risk dissipates. Carefully calibrated changes to the measures could have the additional benefits of helping to reduce the excess supply of high-end housing where nonresident buyers are concentrated and thereby the probability of a sharp downward price correction. Should the activity in certain segments again threaten financial stability, the authorities may consider macroprudential measures that target the specific segments, without a differentiated treatment of non-residents.”

From the IMF’s latest report on Malaysia:

“The authorities continue to closely monitor risks emanating from the housing market, although the risks are deemed manageable (…). House price growth has declined from 6.5 percent in 2017 to 3 percent in 2018H1, and the volume of transactions has also declined. The number of unsold housing units that have been completed or are currently under construction is increasing and is mostly concentrated in high-rise buildings.

Posted by at 9:20 AM

Labels: Global Housing Watch

Friday, March 8, 2019

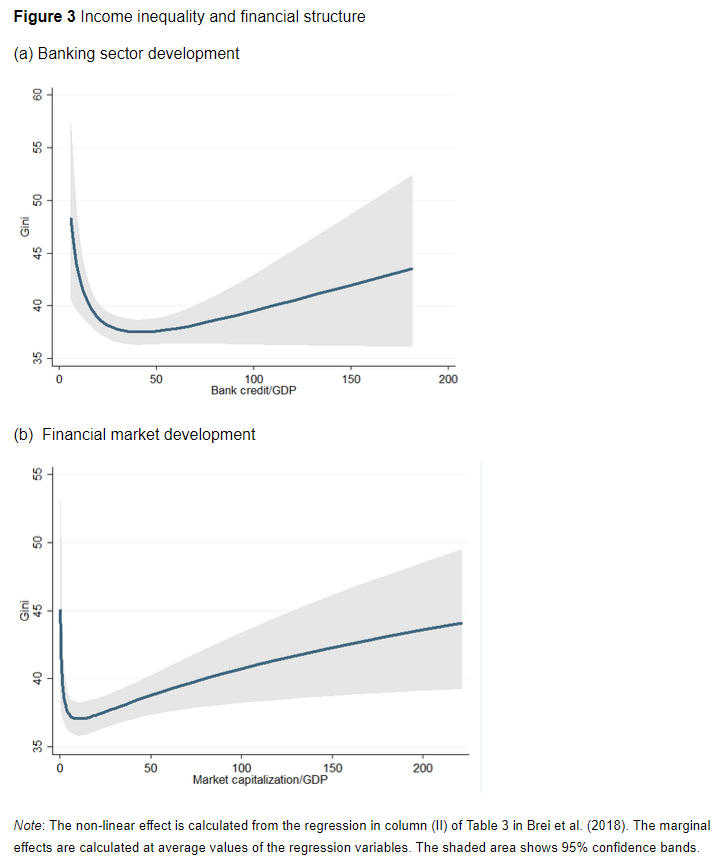

How finance affects income inequality

From a new VOX post:

“There is mounting evidence that income inequality and disparities in wealth have been rising in advanced economies in the recent decades. Using data on advanced and emerging economies, this column investigates the link between an economy’s financial structure – that is, the mix of bank-provided versus market-provided funds – and income inequality. Results show that the relationship is not monotonic. More finance reduces income inequality up to a point, but beyond that point inequality rises, especially if finance is expanded via market-based financing.”

[…]

“Making causal inference is a challenge here. The link between finance and income inequality can go either way. More finance can lead to more income inequality, but more inequality may also foster the development of banks and specialised financial services. A common identification strategy employs instruments that are correlated with the financial structure but not correlated with income inequality. Following the literature, in a recent paper (Brei et al. 2018) we instrument the development of banks and financial markets by their initial values, legal origin, societal fractionalisation, and the location of countries (relative to the Equator). Furthermore, we control for other determinants of income inequality, including the degree of education, industrial specialisation, and inflation.

The main results of our regression analysis are represented in Figure 3. Both higher bank activity and higher market activity translate initially into lower income inequality. However, this pattern reverses beyond a certain threshold. The trajectories of income inequality, once the threshold is reached, differ for bank-based versus market-based financial development. Specifically, the subsequent rise in income inequality is much steeper in market-based financial systems. This suggests that the development of financial markets over the last decades could have produced an increase in income inequality. ”

From a new VOX post:

“There is mounting evidence that income inequality and disparities in wealth have been rising in advanced economies in the recent decades. Using data on advanced and emerging economies, this column investigates the link between an economy’s financial structure – that is, the mix of bank-provided versus market-provided funds – and income inequality. Results show that the relationship is not monotonic. More finance reduces income inequality up to a point,

Posted by at 1:49 PM

Labels: Inclusive Growth

Housing View – March 8, 2019

On the US:

- Oregon’s new rent control law is only a band-aid on the state’s housing woes – Brookings

- Trickle-down housing economics – Northwestern University

- Slicing New York’s Housing Pie – New York Times

- Lens, Manville Shape Discussion of How Housing Can Be Coupled to Transit – Citylab

- Protect First Time Buyers and Taxpayers. Let the “Patch” Expire – American Enterprise Institute

- Boston Wants to Flip More Market-Rate Apartments into Affordable Housing – Next City

- Real Time Economics: More Americans Are Buying a Home Again – Wall Street Journal

- Climate change is hurting coastal real estate values. Oh, we’re losing ocean fish, too –Los Angeles Times

- Ask the Economist with Skylar Olsen – DSNews

- The Affordable Housing Crisis Across The U.S.: ‘Where We Call Home,’ Part 1 – wbur

- Oregon, the Rent Control State – Wall Street Journal

- Housing Affordability for Renters Index: Local Perspective and Migration – Urban Institute

- Three differences between black and white homeownership that add to the housing wealth gap – Urban Institute

- Housing Finance At A Glance: A Monthly Chartbook, February 2019 – Urban Institute

- How student debt may foster homeownership – University of Chicago

- Cheaper Housing Options Boost Homeownership in Some U.S. Metros – Bloomberg

- Redfin: These housing markets give low-income families a better shot at the American Dream – HousingWire

On other countries:

- [Australia] The Housing Market and the Economy – Reserve Bank of Australia

- [Australia] Australian House Prices Provide Food for Doves and Hawks – Bloomberg

- [Australia] Here Are the Winners From Australia’s Property-Market Downturn – Bloomberg

- [China] Chinese Banks Will Rise or Fall With the Property Market – Wall Street Journal

- [Luxembourg] No end in sight for upward housing market spiral in Luxembourg – Financial Times

- [Netherlands] As Amsterdam Overheats, Investors See Rent Cap Scaring off Money – Bloomberg

- [Portugal] Portugal’s housing market is strengthening – Global Property Guide

- [Thailand] Thailand’s modest house price rises – Global Property Guide

- [United Kingdom] Some of Britain’s wealthiest areas hit by house price drops of up to 25 percent – Global Property Guide

On the US:

- Oregon’s new rent control law is only a band-aid on the state’s housing woes – Brookings

- Trickle-down housing economics – Northwestern University

- Slicing New York’s Housing Pie – New York Times

- Lens, Manville Shape Discussion of How Housing Can Be Coupled to Transit – Citylab

- Protect First Time Buyers and Taxpayers. Let the “Patch” Expire – American Enterprise Institute

- Boston Wants to Flip More Market-Rate Apartments into Affordable Housing – Next City

- Real Time Economics: More Americans Are Buying a Home Again – Wall Street Journal

- Climate change is hurting coastal real estate values.

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, March 1, 2019

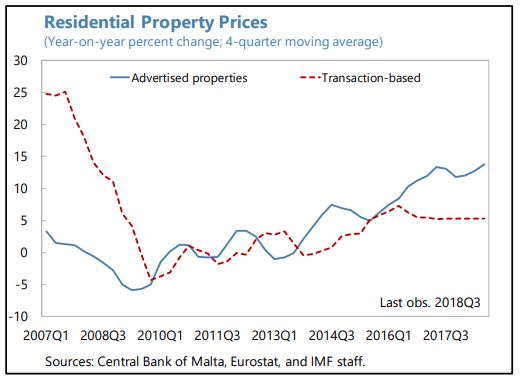

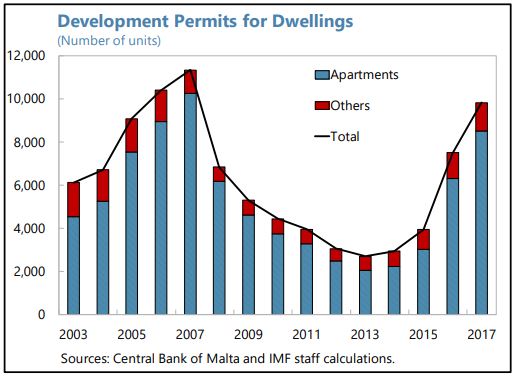

Housing Market in Malta

From the IMF’s latest report on Malta:

“Rapidly rising house prices and rents may eventually pose financial stability risks while putting some vulnerable households at risk of poverty. Policies that help mitigate the rapid increase of house prices and make rents more affordable while strengthening households and banks’ balance sheets should be encouraged.

Strong demand for housing has continued to push up property prices. While some signs of overvaluation have started to emerge, recent house price trends can largely be explained by fundamentals such as e.g., strong immigration flows, rising disposable income, portfolio rebalancing towards property investment and a delayed supply response. Other factors such as the extension of the first-time home-buyer stamp duty relief, the reduced tax rate on rental income, surging demand for tourist accommodation and, for the high-end segment, the IIP may also have played a role (but are not directly controlled for in the empirical analysis conducted in Annex I).

Banks’ exposure to housing-market-related risks is high and increasing, and the introduction of macroprudential measures should proceed as planned. All the more so that households’ indebtedness is relatively high, low income households are vulnerable to housing price corrections and flexible interest rate on mortgages are prevalent.7 Against this backdrop, recent efforts to close data gaps (loan-level data collection) and the planned introduction of borrowerbased macroprudential measures such as caps to loan-to-value (LTV) ratios at origin, stressed debt service-to-income (DSTI) limits, and amortization requirements are steps in the right direction (see text table).

To be more effective, the new borrower-based measures could be refined in due course and exemptions to the LTV limit could be narrowed. To avoid excessive risk concentration, speed limits should be defined in terms of the total value of new loans, not in terms of the number of new loans, and speed limits for loans against secondary and buy-to-let properties, the likely most speculative segment, should be lowered as soon as concerns about any initial disruptions dissipate. Finally, the scope of the new borrower-based measures should be extended to also cover non-bank mortgage loans.

Rapidly rising housing costs are affecting vulnerable households. The government recently relaxed the eligibility requirements for rent subsidies, but the scheme should be periodically reviewed to ensure it remains targeted on low-income households. Further efforts should also be envisaged to accelerate the provision of social housing, including by fiscally incentivizing private investments.

Authorities’ Views

Rapidly rising property prices are viewed by the authorities as mainly reflecting economic fundamentals. Inflows of foreign labor and higher income in general are fueling housing demand. The authorities also see the impact of tax benefits for first and second-time home buyers, the reduced tax rate on rental income and the IIP as marginal. They stressed that the planned borrower-based macroprudential measures were carefully calibrated to have minimal market impact upon their introduction. The authorities have agreed that there is room for refinement, in due course, and emphasized that they can easily recalibrate the measures to mitigate financial stability risks emanating from the housing market in a timely and effective manner. The authorities also recognize the growing importance of making housing more affordable for vulnerable households. They emphasized the progressive nature of the new rent subsidy scheme. Projects are underway to increase the stock of social and affordable housing.”

From the IMF’s latest report on Malta:

“Rapidly rising house prices and rents may eventually pose financial stability risks while putting some vulnerable households at risk of poverty. Policies that help mitigate the rapid increase of house prices and make rents more affordable while strengthening households and banks’ balance sheets should be encouraged.

Strong demand for housing has continued to push up property prices. While some signs of overvaluation have started to emerge,

Posted by at 10:52 AM

Labels: Global Housing Watch

A profile of Branko Milanovic, a leading scholar of inequality

Chris Wellisz profiles Branko Milanovic, a leading scholar of inequality for the March 2019 issue of Finance & Development:

“As a child growing up in Communist Yugoslavia, Branko Milanovic witnessed the protests of 1968, when students occupied the campus of the University of Belgrade and hoisted banners reading “Down with the Red bourgeoisie!”

Milanovic, who now teaches economics at the City University of New York, recalls wondering whether his own family belonged to that maligned group. His father was a government official, and unlike many Yugoslav kids at the time, Milanovic had his very own bedroom—a sign of privilege in a nominally classless society. Mostly he remembers a sense of excitement as he and his friends loitered around the edge of the campus that summer, watching the students sporting red Karl Marx badges.

“I think that the social and political aspects of the protests became clearer to me later,” Milanovic says in an interview. Even so, “1968 was, in many ways, a watershed year” in an intellectual journey that has seen him emerge as a leading scholar of inequality. Decades before it became a fashion in economics, inequality would be the subject of his doctoral dissertation at the University of Belgrade.

Today, Milanovic is best known for a breakthrough study of global income inequality from 1988 to 2008, roughly spanning the period from the fall of the Berlin Wall—which spelled the beginning of the end of Communism in Europe—to the global financial crisis.

The 2013 article, cowritten with Christoph Lakner, delineated what became known as the “elephant curve” because of its shape (see chart). It shows that over the 20 years that Milanovic calls the period of “high globalization,” huge increases in wealth were unevenly distributed across the world. The middle classes in developing economies—mainly in Asia—enjoyed a dramatic increase in incomes. So did the top 1 percent of earners worldwide, or the “global plutocrats.” Meanwhile, the lower middle classes in advanced economies saw their earnings stagnate.

The elephant curve’s power lies in its simplicity. It elegantly summarizes the source of so much middle class discontent in advanced economies, discontent that has turbocharged the careers of populists from both extremes of the political spectrum and spurred calls for trade barriers and limits on immigration.”

Continue reading here.

Chris Wellisz profiles Branko Milanovic, a leading scholar of inequality for the March 2019 issue of Finance & Development:

“As a child growing up in Communist Yugoslavia, Branko Milanovic witnessed the protests of 1968, when students occupied the campus of the University of Belgrade and hoisted banners reading “Down with the Red bourgeoisie!”

Milanovic, who now teaches economics at the City University of New York, recalls wondering whether his own family belonged to that maligned group.

Posted by at 10:44 AM

Labels: Inclusive Growth

Subscribe to: Posts