Tuesday, March 12, 2019

Housing Market in Malaysia

From the IMF’s latest report on Malaysia:

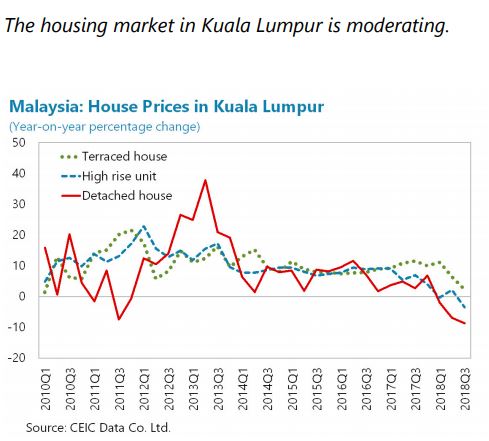

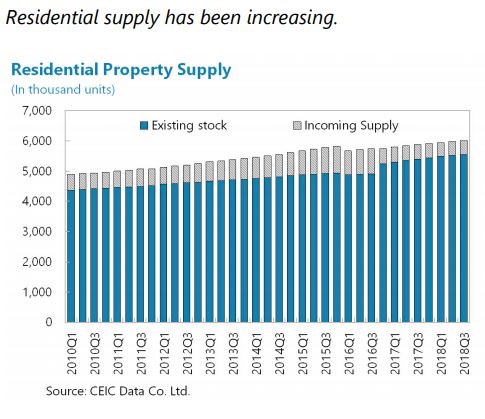

“The authorities continue to closely monitor risks emanating from the housing market, although the risks are deemed manageable (…). House price growth has declined from 6.5 percent in 2017 to 3 percent in 2018H1, and the volume of transactions has also declined. The number of unsold housing units that have been completed or are currently under construction is increasing and is mostly concentrated in high-rise buildings. Banks’ direct exposure to developers remain small and is closely monitored by the BNM. According to BNM stress tests, potential bank losses originating from a possible sharp real estate price adjustment and shocks to income and interest rates are small relative to the banks’ capital buffers. The BNM, MOF, and Ministry of Housing and Local Government have introduced new measures that help reduce the cost of property or of contracting a mortgage loan, with the objective to strengthen the demand for housing and facilitate leasing, and therefore gradually reduce the supply overhang. The impact of these measures should be evaluated on an ongoing basis to ensure effectiveness and correct potential distortions.

As systemic risks from the housing market dissipate, the residency-based differentiation in the real estate measures introduced in 2014 should be gradually phased out. Given banks’ sizable exposure to mortgage lending and to the construction industry, a real estate market price correction, through a reduction in household and corporate wealth, and these agents’ debt servicing capacity, could have a significant impact on growth and financial stability as NPLs rise. During 2012–13, the Malaysian House Price Index (MHPI) grew by a cumulative 24 percent, well-above its long-run annual average of 6 percent and, in 2014, amid further significant price increases, the number of transactions by non-citizens surged by 30 percent (…). The measures introduced in 2014 helped cool down the market (cutting growth in property purchases by non-citizens by over 50 percent in 2015 and by another 38.9 percent in 2016, and slowing the growth rate of MHPI to 9.4 and 7.4 percent in 2014 and 2015, respectively), avoid significant price adjustments, and reduce the rate of future debt build-up, thus reducing the probability of systemic distress. In the absence of a capital inflow surge for the time-being, but still high household leverage, gradually removing the residency-based differentiation in both measures is recommended as systemic risk dissipates. Carefully calibrated changes to the measures could have the additional benefits of helping to reduce the excess supply of high-end housing where nonresident buyers are concentrated and thereby the probability of a sharp downward price correction. Should the activity in certain segments again threaten financial stability, the authorities may consider macroprudential measures that target the specific segments, without a differentiated treatment of non-residents.”

Posted by at 9:20 AM

Labels: Global Housing Watch

Subscribe to: Posts