Thursday, December 16, 2021

WHO Analyzes Trends in Global Healthcare Expenditure

The latest report by World Health Organization, Global expenditure on health: Public spending on the rise? (2021), highlights interesting statistics about expenditure in high income, low income, and low middle-income countries on primary healthcare, the correlation between government spending and out-of-pocket expenditure, trends in public investment patterns, etc. It analyzes data over a 20 year period, from 2000 until 2019, and provides crucial policy insights alongside recent developments.

“Overall, global spending on health has doubled in real terms over the past two decades, reaching US$ 8.5 trillion in 2019 and 9.8% of GDP (up from 8.5% in 2000). Spending on health remained highly unequal—and more unequal than the distribution of global GDP. High income countries accounted for nearly 80% of global spending on health (with the United States of America alone accounting for more than 40%), and their average spending per capita was more than four times the average GDP per capita of low income countries. In countries for which data were available, about half of health spending went towards primary health care (PHC), representing about 3% of GDP on average. Nearly half of PHC spending was funded by private sources, the same as for non-PHC services. Among the low income countries for which data were available, about one-third of PHC spending came from external aid and one-fifth came from government sources, whereas the composition was reversed for non-PHC spending. Further analysis from a set of low and middle income countries indicates that the share of PHC spending that went to infectious diseases was significantly higher than the share that went to noncommunicable diseases and injuries.”

Click here to access the full report.

The latest report by World Health Organization, Global expenditure on health: Public spending on the rise? (2021), highlights interesting statistics about expenditure in high income, low income, and low middle-income countries on primary healthcare, the correlation between government spending and out-of-pocket expenditure, trends in public investment patterns, etc. It analyzes data over a 20 year period, from 2000 until 2019, and provides crucial policy insights alongside recent developments.

“Overall, global spending on health has doubled in real terms over the past two decades,

Posted by at 10:11 AM

Labels: Inclusive Growth

PODCAST: The Challenges of Macroeconomic Forecasting in the Era of COVID

“Economic forecasting is rarely easy. This is especially true in the current environment, as the relationship between economic activity and public health metrics such as the percentage of people vaccinated, or the number of COVID cases, remains far from predictable.

Key macroeconomic questions remain. Is higher inflation likely to persist, or will it prove transitory? Will businesses be able to boost productivity despite the tight labor market, and supply chain disruptions? And what are some of the most useful metrics to assess economic recovery in the current environment?

This week on EconoFact Chats, Julia Coronado discusses these questions, and offers her perspective on which metrics best indicate the health of the economy.”

To know more click here.

“Economic forecasting is rarely easy. This is especially true in the current environment, as the relationship between economic activity and public health metrics such as the percentage of people vaccinated, or the number of COVID cases, remains far from predictable.

Key macroeconomic questions remain. Is higher inflation likely to persist, or will it prove transitory? Will businesses be able to boost productivity despite the tight labor market, and supply chain disruptions? And what are some of the most useful metrics to assess economic recovery in the current environment?

Posted by at 8:47 AM

Labels: Forecasting Forum

Wednesday, December 15, 2021

Pensions at a Glance: Challenges of Ageing Populations

OECD’s latest report, Pensions at a Glance (2021), discusses in detail the financial pressures arising out of rapidly ageing global populations. Although life expectancy gains in old age have slowed since 2010, the pace of ageing is projected to be fast over the next two decades. The size of the working-age population is projected to fall by more than one‑quarter by 2060 in most Southern, Central and Eastern European countries as well as in Japan and Korea.

Pension finances deteriorated during the pandemic due to lost contributions, and shortfalls have been mainly covered by state budgets. The report emphasizes the fact that the biggest long-term challenge for pensions continues to be providing financially and socially sustainable pensions in the future. Many countries have introduced automatic adjustment mechanisms (AAM- adjusting retirement ages, benefit levels and contribution rates and using an automatic balancing mechanism) in their pension systems that change pension system parameters, such as pension ages, benefits or contribution rates when demographic, economic or financial indicators change. Putting pensions systems on a solid footing for the future will require painful policy decisions.

Click here to read the full report.

OECD’s latest report, Pensions at a Glance (2021), discusses in detail the financial pressures arising out of rapidly ageing global populations. Although life expectancy gains in old age have slowed since 2010, the pace of ageing is projected to be fast over the next two decades. The size of the working-age population is projected to fall by more than one‑quarter by 2060 in most Southern, Central and Eastern European countries as well as in Japan and Korea.

Posted by at 9:38 AM

Labels: Inclusive Growth

Tuesday, December 14, 2021

The State of Economic Opportunity in America

The recent McKinsey American Opportunity Survey (2021) highlights interesting observations about American beliefs on the availability of economic opportunity, obstacles, and the path ahead to create a more inclusive economy. A sample of 25,109 adults aged 18 and older from the continental United States, Alaska, and Hawaii was interviewed online in English and Spanish. Excerpts from the report’s findings:

“Americans report that their financial situations have deteriorated over the past year, and at the time of our survey, only half of all respondents reported being able to cover their living expenses for more than two months in the event of job loss. Americans reported facing numerous barriers to economic opportunity and inclusion—among them, inadequate access to health insurance and physical and mental healthcare, as well as to affordable childcare. Moreover, many respondents said that they feel their very identity limits their access to jobs and to fair recognition and reward for their work.

Yet amid the challenges, our survey also revealed optimism. First- and second-generation immigrant respondents were among the most optimistic respondents about economic opportunity. Black and Hispanic/Latino respondents were also among the most optimistic respondents, despite being more likely to report barriers to opportunity.”

Click here to read the full report.

The recent McKinsey American Opportunity Survey (2021) highlights interesting observations about American beliefs on the availability of economic opportunity, obstacles, and the path ahead to create a more inclusive economy. A sample of 25,109 adults aged 18 and older from the continental United States, Alaska, and Hawaii was interviewed online in English and Spanish. Excerpts from the report’s findings:

“Americans report that their financial situations have deteriorated over the past year, and at the time of our survey,

Posted by at 1:11 PM

Labels: Inclusive Growth

Monday, December 13, 2021

China’s Coming Property Correction: A Managed Soft Landing

From MacroPolo:

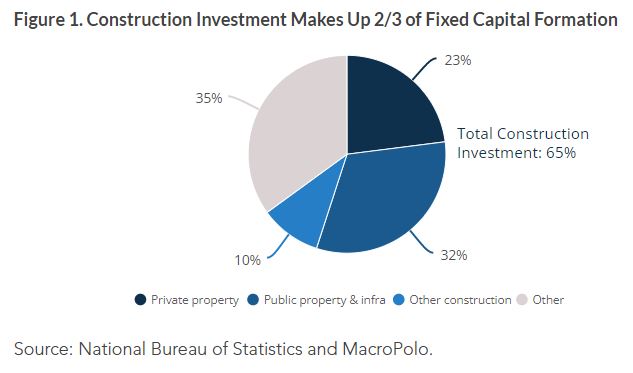

“With China’s Evergrande moving into what appears to be a managed default process, as we had previously anticipated, it’s time to look at the future of the property sector. Even without the Evergrande crisis, the property sector is bound to see a correction. The crisis simply made the writing on the wall clearer. Such a correction means that China’s notoriously outsized investment-driven model will have to be “right-sized.”

The right-sizing of investment, which mainly refers to fixed-capital formation that makes up about 43% of GDP, will inevitably hurt growth (see Figure 1). Getting a handle on the magnitude of the growth impact, therefore, will be key to any analysis of China’s economic future. To do so requires examining construction-related investment, which is composed mainly of private property investment and local government investment (including public housing and infrastructure).

Our baseline scenario assumes a 30% decline in private property construction through 2025. In total construction volume terms, that means a correction from 100 million units to roughly 70 million units. Such a correction will lead to annual property sales falling from 15% to 10% of GDP by 2025, which is basically the same level as in 2010. In other words, China intends to roll back the decade of rapid property sector growth in the next five years.

As a result, local government investment, which is basically public spending on infrastructure that depends largely on land revenue derived from private property investment, will likely decline by 3% of GDP over the same period. Combined with the property correction, we expect overall construction investment to be down by 6% of GDP.”

From MacroPolo:

“With China’s Evergrande moving into what appears to be a managed default process, as we had previously anticipated, it’s time to look at the future of the property sector. Even without the Evergrande crisis, the property sector is bound to see a correction. The crisis simply made the writing on the wall clearer. Such a correction means that China’s notoriously outsized investment-driven model will have to be “right-sized.”

The right-sizing of investment,

Posted by at 8:10 AM

Labels: Global Housing Watch

Subscribe to: Posts