Thursday, March 9, 2023

Housing Market in Netherlands

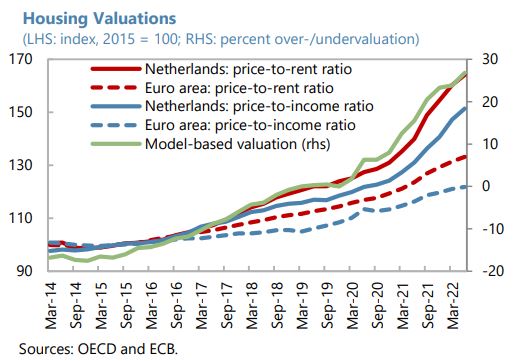

From the IMF’s latest report on Netherlands:

“Credit has grown at a robust pace, but the phase out of monetary accommodation has contributed to tighter financial conditions and the cooling of a buoyant housing market. Mortgage lending has expanded at a brisk rate (…), reflecting strong housing demand, yet prices for homes have recently started to decline, falling 2 percent below their July 2022 peak. Echoing the scaling back of monetary accommodation, interest rates for housing and corporate loans have started to rise from historic lows. At the same time, banks have tightened credit standards, primarily on the back of deteriorating risk perceptions due to an uncertain economic outlook.”

(…)

“The cooling of a richly valued housing market calls for ongoing alertness towards emerging strains and readiness to deploy existing buffers if needed. Recently flagging house price momentum accentuates vulnerabilities from a residential real estate sector deemed overvalued on a broad range of measures (…). Household indebtedness, at more than 100 percent of GDP, is among the highest in the euro area while a large part of assets is concentrated in (illiquid) pension and insurance claims (…). With house prices acting as a potential amplifier, this raises the risk of borrower distress in the event of an economic downturn, although the large share of fixed-rate mortgages (more than 90 percent of the total) and long maturities (typically 30 years) provides some comfort. Still, vulnerabilities are heightened by about a quarter of outstanding mortgages facing an interest rate reset in the coming five years, overextended balance sheets of recent home buyers, a prevalence of interest-only mortgages (around two fifths of the total), and debt service to income ratios (DSTIs) becoming more binding for new mortgages due to rising interest rates. In this context, maintaining minimum risk weight floors for mortgage loans (activated in January 2022) until December 1, 2024, is appropriate as it helps stabilize the housing cycle and preserves buffers that should be released to absorb credit losses in the event of a more severe housing market downturn. Likewise, efforts to increase awareness about the risks from interest-only lending among borrowers and lenders are welcome. Structurally, the Dutch housing market remains unbalanced, requiring determined policy intervention. Policy measures should strive to lessen incentives for households to live in highly leveraged, owner-occupied housing. The government’s program to address housing shortages and ensure affordability contain important elements to tackle underlying imbalances but means-testing for social housing eligibility could be strengthened and the need for expansive rent control should be re-evaluated.”

From the IMF’s latest report on Netherlands:

“Credit has grown at a robust pace, but the phase out of monetary accommodation has contributed to tighter financial conditions and the cooling of a buoyant housing market. Mortgage lending has expanded at a brisk rate (…), reflecting strong housing demand, yet prices for homes have recently started to decline, falling 2 percent below their July 2022 peak. Echoing the scaling back of monetary accommodation,

Posted by at 10:37 AM

Labels: Global Housing Watch

Housing Supply in the Netherlands: The Road to more Affordable Living

From the IMF’s latest report on Netherlands:

“With the supply of residential dwellings in the Netherlands having failed to live up to demand over the last decade, apprehension among the population about the availability of affordable housing has risen. Particularly spatial, regulatory, planning, environmental and supply chain constraints have kept a lid on construction. Recognizing the socio-economic challenges posed by inadequate housing supply, the government has embarked on an ambitious agenda with promising steps to boost the availability of affordable properties. To strengthen the traction of housing policies to reach its intended goals, a larger role for economic incentives and private sector involvement should be evaluated.”

From the IMF’s latest report on Netherlands:

“With the supply of residential dwellings in the Netherlands having failed to live up to demand over the last decade, apprehension among the population about the availability of affordable housing has risen. Particularly spatial, regulatory, planning, environmental and supply chain constraints have kept a lid on construction. Recognizing the socio-economic challenges posed by inadequate housing supply, the government has embarked on an ambitious agenda with promising steps to boost the availability of affordable properties.

Posted by at 10:28 AM

Labels: Global Housing Watch

Wednesday, March 8, 2023

Income and emotional well-being: A conflict resolved

Matthew A. Killingsworth, Daniel Kahneman, and Barbara Mellers explore the relationship between income and emotional well-being.

“Using dichotomous questions about the preceding day, [Kahneman and Deaton, Proc. Natl. Acad. Sci. U.S.A. 107, 16489–16493 (2010)] reported a flattening pattern: happiness increased steadily with log(income) up to a threshold and then plateaued. Using experience sampling with a continuous scale, [Killingsworth, Proc. Natl. Acad. Sci. U.S.A. 118, e2016976118 (2021)] reported a linear-log pattern in which average happiness rose consistently with log(income).”

Read more here.

Matthew A. Killingsworth, Daniel Kahneman, and Barbara Mellers explore the relationship between income and emotional well-being.

“Using dichotomous questions about the preceding day, [Kahneman and Deaton, Proc. Natl. Acad. Sci. U.S.A. 107, 16489–16493 (2010)] reported a flattening pattern: happiness increased steadily with log(income) up to a threshold and then plateaued. Using experience sampling with a continuous scale, [Killingsworth, Proc. Natl. Acad. Sci. U.S.A. 118, e2016976118 (2021)] reported a linear-log pattern in which average happiness rose consistently with log(income).”

Posted by at 9:43 AM

Labels: Inclusive Growth, Macro Demystified

Friday, March 3, 2023

Housing View – March 3, 2023

On cross-country:

- Threat of global housing slide looms amid rising rates – Dallas Fed

- ‘The risk of a deep housing slide persists’: Dallas Fed says downturn in U.S. and German housing markets could affect the rest of the world – Market Watch

- How low will house prices go? Lessons from UK, US, Europe and elsewhere – The Guardian

On the US—developments on house prices, rent, permits and mortgage:

- U.S. mortgage interest rates jump to highest level since November – MBA – Reuters

- US to Cut Mortgage Insurance Costs for Some New Homeowners. Program seeks to ease soaring borrowing costs that hurt demand. Vice President Harris to announce the program on Wednesday – Bloomberg

- Mortgage applications plummet as rates jump – Axios

- That 3% Mortgage Just Keeps Getting Better. As the Fed pushes interest rates higher, homeowners who secured ultra-cheap loans during the pandemic can invest in low-risk Treasuries that earn enough to significantly offset the cost of their homes. – Bloomberg

- Measures of Shelter in the CPI and PCE price indexes Still Increasing – Calculated Risk

- Case-Shiller: National House Price Index “Decline Continued” to 5.8% year-over-year increase in December – Calculated Risk

- Freddie Mac House Price Index Declines for 7th Consecutive Month in January. 37 States and D.C. have seen price declines Seasonally Adjusted – Calculated Risk

- U.S. house price inflation cools further in December – Reuters

- A Tight Labor Market Could Keep Rent Inflation Elevated – Kansas City Fed

- Year-over-year Rent Growth Continues to Decelerate. Expect YoY Rents to Slow Further – Calculated Risk

On the US—other developments:

- America’s property market suggests recession is on the way. As developers find clever ways to cut mortgage rates, the Fed may fight back – The Economist

- Checking in on the U.S. Housing Market. Activity is normalizing along with rates. Builders’ prudence on hiring during the boomlet is now shielding the job market. – The Overshoot

- Will US Housing Crash The Economy? Maybe it’s different this time. – Bloomberg

- How homebuilders are luring buyers back – Axios

- New Home Sales Increase to 670,000 Annual Rate in January – NAHB

- New Home Sales Up in January but Higher Rates Signal Further Weakness – NAHB

- Lawler: AMH Net Seller of Existing Single-Family Homes, “Investor” Home Purchases Plunged – Calculated Risk

- America’s Housing Market Has Flipped But Not Flopped. A dearth of supply of existing homes is leading to a boom in building, despite sky-high mortgage rates. – Bloomberg

- U.S. pending home sales post largest gain in 2-1/2 years in January – Reuters

- The frozen housing market. And what it means for the economy – FT

- The Age Gap in Mortgage Access – Philadelphia Fed

- Financial Benefits Motivated Homebuying During the Pandemic, More So Than Space or Location Preferences – Fannie Mae

- How Is Digitalization Transforming How People Find and Finance Housing? – Harvard Joint Center for Housing Studies

- Private Residential Spending Falls Slightly in January – NAHB

On other countries:

- [Germany] Germany home prices to sink nearly 6% this year – Reuters

- [Hong Kong] Hong Kong home prices end seven-month decline with 0.6% rise in January – Reuters

- [United Kingdom] Rising UK Rents Will Cushion Any Drop in House Prices. The cost to society of a dysfunctional housing market, as young aspiring buyers are thwarted while landlords saving for retirement are penalized, is rising. – Bloomberg

- [United Kingdom] UK’s Soaring Mortgage Costs Mean It’s Cheaper to Rent a Home. Capital Economics says average mortgage tops £1,000 a month. Renting probably will become more expensive next year – Bloomberg

- [United Kingdom] England’s new housing supply likely to fall to lowest level in decades, study says. Home Builders Federation warns planning policy changes will result in government meeting less than half its annual target – The Guardian

- [United Kingdom] House building set to slump in England, warns trade body. Number of new properties completed each year could fall to 110,000 says Home Builders Federation – FT

- [United Kingdom] Three years on: how the pandemic reshaped the UK housing market – Lloyds Banking Group

- [United Kingdom] UK house prices suffer biggest fall in more than a decade as higher interest rates bite. Nationwide figures show a greater than expected 1.1% drop in year to February – FT

On cross-country:

- Threat of global housing slide looms amid rising rates – Dallas Fed

- ‘The risk of a deep housing slide persists’: Dallas Fed says downturn in U.S. and German housing markets could affect the rest of the world – Market Watch

- How low will house prices go? Lessons from UK, US, Europe and elsewhere – The Guardian

On the US—developments on house prices,

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, March 2, 2023

Housing Market in Belgium

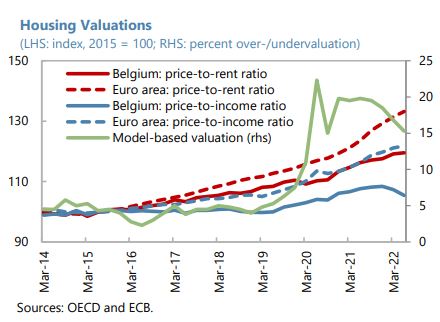

From the IMF’s latest report on Belgium:

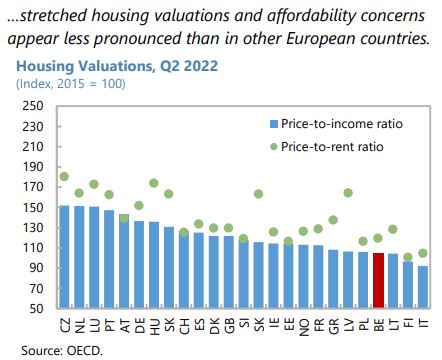

“Cooling of the housing market, which has been characterized by elevated prices, calls for heightened vigilance and release of buffers, if needed. Although valuations are not as stretched as elsewhere in Europe, model-based estimates point to some overvaluation. Bank mortgage exposures are relatively high, and debt-service-to-income ratios are somewhat elevated. Risks are mitigated by prevalence of mortgages with full-recourse provisions that amortize fully over the maturity of the loan and by a high share of fixed-rate and longer-term (>15 years) loans. A sectoral systemic risk buffer (SSyRB) against housing-related exposures introduced in May 2022 and tighter LTV limits imposed by prudential guidelines since 2020 provide additional comfort. Moreover, aggregate liquid assets of households exceed mortgage debt (…), potentially cushioning the impact of deteriorating income prospects on debt servicing capacity. Still, the recent slowdown of house-price momentum, potentially heralding a sharper market turn, deserves careful monitoring and SSyRB deployment, if needed. Despite limited use, strict eligibility criteria, and adequate provisioning, reactivating mortgage moratoria for October 2022-March 2023 to cushion energy-crisis impacts was inappropriate, as it may delay timely bank-borrower engagement to address debt-servicing challenges. NBB efforts to gather housing stock energy efficiency information to allow for better assessment of collateral values and risks are welcome and should continue, particularly given emerging stratification of house prices based on sustainability considerations.”

From the IMF’s latest report on Belgium:

“Cooling of the housing market, which has been characterized by elevated prices, calls for heightened vigilance and release of buffers, if needed. Although valuations are not as stretched as elsewhere in Europe, model-based estimates point to some overvaluation. Bank mortgage exposures are relatively high, and debt-service-to-income ratios are somewhat elevated. Risks are mitigated by prevalence of mortgages with full-recourse provisions that amortize fully over the maturity of the loan and by a high share of fixed-rate and longer-term (15 years) loans.

Posted by at 10:16 AM

Labels: Global Housing Watch

Subscribe to: Posts