Thursday, March 2, 2023

Housing Market in Belgium

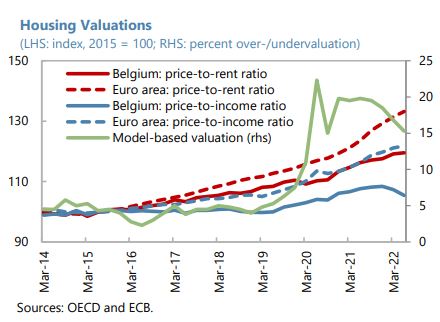

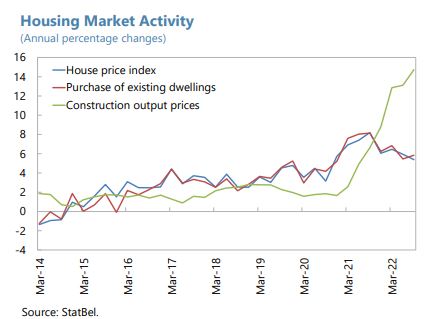

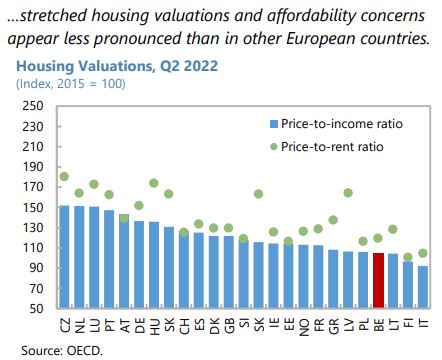

From the IMF’s latest report on Belgium:

“Cooling of the housing market, which has been characterized by elevated prices, calls for heightened vigilance and release of buffers, if needed. Although valuations are not as stretched as elsewhere in Europe, model-based estimates point to some overvaluation. Bank mortgage exposures are relatively high, and debt-service-to-income ratios are somewhat elevated. Risks are mitigated by prevalence of mortgages with full-recourse provisions that amortize fully over the maturity of the loan and by a high share of fixed-rate and longer-term (>15 years) loans. A sectoral systemic risk buffer (SSyRB) against housing-related exposures introduced in May 2022 and tighter LTV limits imposed by prudential guidelines since 2020 provide additional comfort. Moreover, aggregate liquid assets of households exceed mortgage debt (…), potentially cushioning the impact of deteriorating income prospects on debt servicing capacity. Still, the recent slowdown of house-price momentum, potentially heralding a sharper market turn, deserves careful monitoring and SSyRB deployment, if needed. Despite limited use, strict eligibility criteria, and adequate provisioning, reactivating mortgage moratoria for October 2022-March 2023 to cushion energy-crisis impacts was inappropriate, as it may delay timely bank-borrower engagement to address debt-servicing challenges. NBB efforts to gather housing stock energy efficiency information to allow for better assessment of collateral values and risks are welcome and should continue, particularly given emerging stratification of house prices based on sustainability considerations.”

Posted by at 10:16 AM

Labels: Global Housing Watch

Subscribe to: Posts