Thursday, March 9, 2023

Housing Market in Netherlands

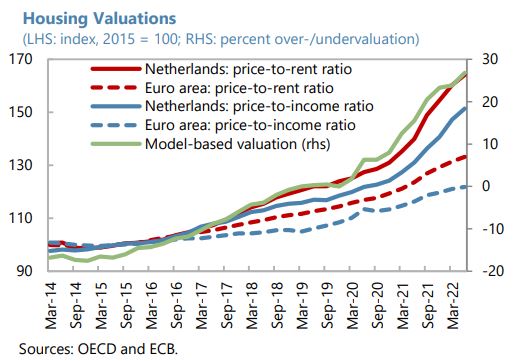

From the IMF’s latest report on Netherlands:

“Credit has grown at a robust pace, but the phase out of monetary accommodation has contributed to tighter financial conditions and the cooling of a buoyant housing market. Mortgage lending has expanded at a brisk rate (…), reflecting strong housing demand, yet prices for homes have recently started to decline, falling 2 percent below their July 2022 peak. Echoing the scaling back of monetary accommodation, interest rates for housing and corporate loans have started to rise from historic lows. At the same time, banks have tightened credit standards, primarily on the back of deteriorating risk perceptions due to an uncertain economic outlook.”

(…)

“The cooling of a richly valued housing market calls for ongoing alertness towards emerging strains and readiness to deploy existing buffers if needed. Recently flagging house price momentum accentuates vulnerabilities from a residential real estate sector deemed overvalued on a broad range of measures (…). Household indebtedness, at more than 100 percent of GDP, is among the highest in the euro area while a large part of assets is concentrated in (illiquid) pension and insurance claims (…). With house prices acting as a potential amplifier, this raises the risk of borrower distress in the event of an economic downturn, although the large share of fixed-rate mortgages (more than 90 percent of the total) and long maturities (typically 30 years) provides some comfort. Still, vulnerabilities are heightened by about a quarter of outstanding mortgages facing an interest rate reset in the coming five years, overextended balance sheets of recent home buyers, a prevalence of interest-only mortgages (around two fifths of the total), and debt service to income ratios (DSTIs) becoming more binding for new mortgages due to rising interest rates. In this context, maintaining minimum risk weight floors for mortgage loans (activated in January 2022) until December 1, 2024, is appropriate as it helps stabilize the housing cycle and preserves buffers that should be released to absorb credit losses in the event of a more severe housing market downturn. Likewise, efforts to increase awareness about the risks from interest-only lending among borrowers and lenders are welcome. Structurally, the Dutch housing market remains unbalanced, requiring determined policy intervention. Policy measures should strive to lessen incentives for households to live in highly leveraged, owner-occupied housing. The government’s program to address housing shortages and ensure affordability contain important elements to tackle underlying imbalances but means-testing for social housing eligibility could be strengthened and the need for expansive rent control should be re-evaluated.”

Posted by at 10:37 AM

Labels: Global Housing Watch

Subscribe to: Posts