Saturday, September 17, 2022

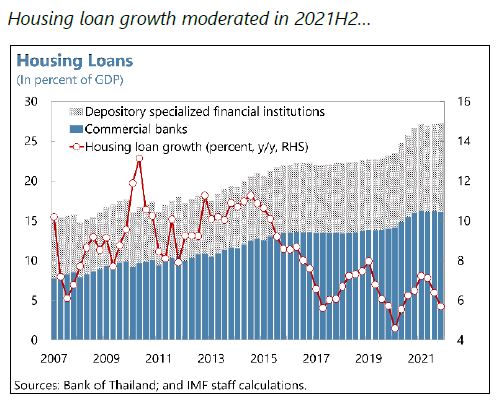

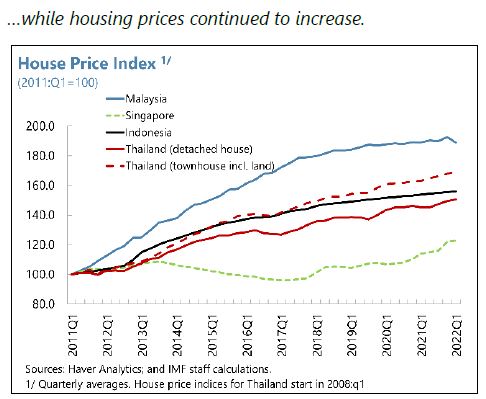

Housing Market in Thailand

Posted by at 8:05 AM

Labels: Global Housing Watch

Friday, September 16, 2022

Housing View – September 16, 2022

Conferences:

- International Conference on Real Estate Development and Management on February 1th to 4th, 2023 – Ankara University

On cross-country:

- The World’s Hottest Housing Markets Are Facing a Painful Reset. Frothy property markets are poised for double-digit price declines as consumers face mounting financial pressures. – Bloomberg

- A Global Housing Bust Looms – Bloomberg

- Asia Real Estate Prices Cool in Early Sign of Global Slowdown. Countries including New Zealand and China saw declines in the second quarter, even as prices continued to climb in most places around the world. – Bloomberg

- Real estate booms are behind Europe’s productivity divergence – VoxEU

On the US—developments on house prices and rent:

- If You Want to Know Where US Inflation Is Heading, Look at Rents. Housing costs play big role in measures of underlying prices. Rent may be close to topping out, but won’t cool any time soon – Bloomberg

- How the ‘Rise of the Rest’ Became the ‘Rise of the Rents’. The pandemic helped spread the sky-high housing prices of coastal hubs to other cities across the US. Here’s why it happened. – Bloomberg

- San Francisco Home Prices Slide in Stark Turn for Costly City. Brokerages show values falling 7% in the past year as higher mortgage rates and work-from-home issues crush demand. – Bloomberg

- Paul Krugman: Apartment rents peaking? More important than people may realize for economic policy, because rents — market rents and imputed rents on owner-occupied housing — are key drivers of all measures of core inflation 1/ – Twitter

On the US—other developments:

- Housing market to see ‘significant amount of weakness ahead,’ Goldman says – Yahoo Finance

- The Fed Is Driving an Unusual Contradiction in the Housing Market – Barron’s

- Current State of the Housing Market – Calculated Risk

- 2nd Look at Local Housing Markets in August. Sales and New Listings Down Sharply Year-over-year – Calculated Risk

- Housing inflation is dead. But high housing prices live on – FT

- 1st Look at Local Housing Markets in August. Sales and New Listings Down Sharpy Year-over-year – Calculated Risk

- How Not to Blow Up the Housing Market – American Action Forum

- Median Price of a New Age-Restricted Home Up to $472,000 – NAHB

- Housing Slowdown Puts Damper on Rent-Backed Bonds. Sales of single-family rental-backed bonds to decelerate. Strong rental market is still a positive for the sector – Bloomberg

- Mortgage Equity Withdrawal Still Strong in Q2. Homeowners now relying on Home Equity lines to extract equity – Calculated Risk

- Will the Fed really sell its mortgage bonds next year? Predictability and principles should win – FT

- U.S. Bancorp expects mortgages to be down 30%-35% in Q3 vs Q2 – Reuters

- Real Estate Listings With Flood Scores Shift Home-Shopper Habits. Redfin users who were shown home flood scores went on to view lower-risk properties, an experiment by the company found. – Bloomberg

- Regional Bank Heads See More Signs of Mortgage-Business Strain on Rates. U.S. Bancorp sees mortgage revenue falling as much as 35%. JPMorgan, Wells Fargo are cutting back their mortgage staffs – Bloomberg

- These Housing Markets Are Most at Risk of a Downturn, According to a New Report – Barron’s

- Q2 Update: Delinquencies, Foreclosures and REO. REO: lender Real Estate Owned – Calculated Risk

- U.S. mortgage interest rates top 6% for first time since 2008 – Reuters

On China:

- China Rolls Out Property Policies Across Nation to Fix Slump. At least 70 policies have been issued across cities in China. Cities are optimizing policies based on their own situation – Bloomberg

- Chinese Banks Lose a Mortgage Safety Net as Developers Slide Into Distress. Real-estate firms have written at least $300 billion in mortgage guarantees on uncompleted homes that they presold – Wall Street Journal

- Evergrande vows to restart all stalled property projects. Heavily indebted Chinese developer’s Hong Kong headquarters was seized last week – FT

- China’s ponzi-like property market is eroding faith in the state. Its meltdown could scarcely come at a worse time for Xi Jinping – The Economist

- Evergrande Vows to Resume Projects to Allay Boycott Concerns. Debt-laden developer to restart remaining 38 stalled projects. Unfinished homes have led buyers to boycott mortgages in China – Bloomberg

- Chinese Rush to Repay Mortgages Gains Momentum in Abrupt U-Turn. People are cashing in investment products to pay off mortgages as economic uncertainty and Covid-19 outbreaks cause them to rethink their finances. – Bloomberg

On other countries:

- [Australia] ‘A necessity’: housing prices force more Australians into share homes in midlife. The share-house demographic is skewing older. More people are renting and sharing – and they’re doing it longer – The Guardian

- [Australia] Rent is skyrocketing in Australia. Is Airbnb responsible for driving up prices? Experts say many factors are responsible for rising costs, and growth in short-term rentals may not be the main culprit – The Guardian

- [Australia] High-density development and better rent assistance key to addressing Australia’s housing crisis, economist says. Brendan Coates warns person’s future wealth is increasingly driven by ‘who their parents were rather than their talent’ – The Guardian

- [Finland] Finland’s housing market remains stable – Global Property Guide

- [Hong Kong] Recent Hong Kong homebuyers stand to lose millions as prices decline – some already have. Many people who bought homes over the past five years are now facing a loss – at least on paper – as prices continue to slide. Some owners who had to sell have taken significant losses – in one case to the tune of HK$5.85 million (US$745,334) – South China Morning Post

- [Ireland] Irish house price growth slows to 13% year-on-year in July – Reuters

- [New Zealand] House prices continue to slide from last year’s peak – RNZ

- [Singapore] Singapore’s modest house price growth – Global Property Guide

- [Singapore] Singapore Property Is Unaffordable, Six Out of 10 People Say. City-state’s real estate market defies gravity, fueling angst. Rising rates are having a limited impact on market: analyst – Bloomberg

- [South Korea] Korea’s Housing Market Falls Most Since Global Financial Crisis – Bloomberg

- [Sweden] Sweden’s Big Short Signals Trouble for European Real Estate. SBB is second-most shorted stock in Europe on debt concerns. Falling property values, refinancing woes pose downgrade risk – Bloomberg

- [United Kingdom] The great British housing wealth divide. The over-65s hold 47 per cent of housing equity and 7.4mn ‘extra’ bedrooms. Could the cost of living crisis change things? – FT

- [United Kingdom] Builders and estate agents braced for UK housing downturn. Protracted drop in activity and prices likely because of high inflation and low consumer confidence – FT

- [United Kingdom] Higher rents and utility bills pushing people into smaller homes, says Zoopla. Trend for cheaper flats and houses comes with increase in cost of living pressures – FT

- [United Kingdom] UK Consumer Confidence Drop Feeds Concern About House Prices. YouGov survey shows first negative reading since 2020 lockdown. Outlook for house prices plummets with rising mortgage rates – Bloomberg

Conferences:

- International Conference on Real Estate Development and Management on February 1th to 4th, 2023 – Ankara University

On cross-country:

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, September 9, 2022

Housing View – September 9, 2022

On cross-country:

- Global house prices display surprising resilience in Q2. Global housing markets wrongfooted us this quarter with housing markets displaying relative resilience. – Knight Frank

- Curtains drawing on runaway rise in global house prices: Reuters poll – Reuters

- City house prices outperform national housing markets in Q2. City prices stole a march on their national counterparts in Q2 2022, although neither saw the sudden downturn that many anticipated. – Knight Frank

- Crypto real estate: the property market built on digital assets. Agents want to tap a growing pool of buyers looking to convert their cryptocurrency into bricks and mortar – FT

On the US—developments on house prices and rent:

- US Consumers See Home Prices Falling for First Time Since 2020. Fannie Mae survey shows 0.4% decline in price expectations. Expected rental price growth slides most in data back to 2010 – Bloomberg

- June 2022 Case-Shiller Results & Forecast: Moving Towards Rebalance – Zillow

- Will House Prices Decline Nationally? – Calculated Risk

- Lawler: Are “National” Home Prices Already Falling? – Calculated Risk

- The Sharp Slowdown in Year-over-year House Price Growth – Calculated Risk

- Apartment inflation – The Grumpy Economist

On the US—other developments:

- Why the Housing Market Is Not in Recession. Housing sales are falling in response to rising interest rates, but the real estate market is not in a recession, according to Wharton’s Fernando Ferreira. He explains why the persistent lack of supply will continue to put pressure on homebuyers. – Wharton

- Are Mortgages Becoming More Affordable? – St. Louis Fed

- Why housing is the key to the next Fed pivot. The US faces a perfect storm of rising financing costs, squeezed demand and increased supply – FT

- Shift to Working from Home Diminished Large Cities’ Productivity Premium – Dallas Fed

- California Fights Its NIMBYs. Laws to encourage more development and denser housing don’t do much good if no one enforces them. As the state political calculus shifts, Gavin Newsom is trying to change that. – New York Times

- Housing Innovation Faces Many Barriers – Cato Institute

- California Fights Its NIMBYs. Laws to encourage more development and denser housing don’t do much good if no one enforces them. As the state political calculus shifts, Gavin Newsom is trying to change that. – New York Times

- Affordable-Housing Projects Derailed as Developers Struggle for Financing. Rising interest rates, inflation and supply-chain issues lead to delays in development – Wall Street Journal

- US mortgage lenders are starting to go bankrupt — how this one factor could be triggering the worst surge of failures since 2008 – Yahoo

- August 2022 Monthly Housing Market Trends Report – Realtor

- Share of Smaller Lots Record High Amid Pandemic – NAHB

- Black Knight Mortgage Monitor: “Total market leverage was just 42% of mortgaged homes’ values, the lowest on record”. “Tappable equity is now down 5% in the last two months” – Calculated Risk

- High Home Prices, Mortgage Rates Weighing on Housing Sentiment – Fannie Mae

- How We Know California’s New Rent Control Law Will Make Its Housing Shortage Worse. Rent controls propose using government regulation to solve the symptom—high prices—of a problem—a shortage of housing—which government regulation created in the first place. – FEE

- Homebuilder Comments in August: Increased Incentives Helping Sales. “Construction cycle time has improved” – Calculated Risk

On China:

- Evergrande crisis deepens as lender seizes headquarters. World’s most indebted property developer defaulted on loan and twice failed to sell Hong Kong building – FT

- Chinese city to start building stalled housing projects amid mortgage boycott – Reuters

- Beijing’s Debts Come Due. How a Burst Real-Estate Bubble Threatens China’s Economy – Foreign Affairs

- As China’s property crisis grows, can nationalisation help rebalance its economy? Developers’ debt crisis raises concerns about health of banks, local governments’ fiscal viability, impact of falling property prices on consumption and economic growth. China can look to US experience where partial nationalisation of troubled assets, financial institutions helped restore financial stability, boost economic recovery – South China Morning Post

On other countries:

- [Australia] Era of through-the-roof house prices in Australia set to end: Reuters poll – Reuters

- [Australia] As rates rise, housing markets show no sign of distress – Financial Review

- [Cambodia] Cambodia’s house prices in freefall – Global Property Guide

- [Canada] Canada house prices set for sharp fall in 2023; BoC to hike 75 bps on Sept 7 – Reuters

- [Canada] Vancouver home sales slumped in August as higher rates shift market – Bloomberg

- [France] France Weighs Revising Mortgage Rules to Support Lending. Le Maire says regulators could lift cap on home loan rates. Finance ministry in talks with Bank of France on the matter – Bloomberg

- [India] Rate hikes unlikely to dent housing demand in India, Bengaluru to lead price rises – Reuters

- [Ireland] Examining the response of house prices to supply using a Markov regime switching approach: The case of the Irish housing market – ESRI

- [Mexico] Mexican housing must become denser, better planned – study – Reuters

- [New Zealand] Boom turns to gloom as higher interest rates hit New Zealand housing – Reuters

- [New Zealand] New Zealand house prices continue to plunge, as national average falls below $1m. Downturn is entrenched across the country, but fears that falling prices and rising interest rates will hit borrowers have been played down – The Guardian

- [New Zealand] New Zealand’s house prices rising strongly, despite falling demand – Global Property Guide

- [Sweden] Stockholm’s ‘Housing for All’ Is Now Just for the Few. Soaring demand for rent-controlled housing in the Swedish capital has left many residents at the mercy of an expensive, sometimes dangerous sublet market. – Bloomberg

- [United Arab Emirates] POLL Dubai housing market outlook dims on increase in borrowing costs – Reuters

- [United Kingdom] UK housing is on shaky foundations. Era of rock bottom interest rates, elevated demand and ample government support is drawing to a close – FT

- [United Kingdom] Is owning a second home unethical? A philosopher reflects. With the UK’s woefully undersupplied housing market, buying a holiday home in some areas has become a controversial act – FT

- [United Kingdom] Coming UK house price plunge has a silver lining. You may not benefit, but your children could – FT

- [United Kingdom] UK house prices rise at annual rate of 10% despite steeper mortgage costs. Double-digit growth for 10th successive month surpasses economists’ expectations of slowdown – FT

- [United Kingdom] UK House Prices Forecast to Stall Next Year as Rents Continue Rising – FT

- [United Kingdom] UK housebuilders’ shares tumble on gloomy house price predictions. HSBC expects value of average British home to drop 7.5% with central London falling further – FT

- [United Kingdom] Startup Wants to Chart Path to More Equitable Urban Development. OneCity says its digital-mapping app can help planners create housing that better serves the needs of the poor. – Bloomberg

- [United Kingdom] UK House Prices Rise Led By Surge in London, Halifax Says – Bloomberg

On cross-country:

- Global house prices display surprising resilience in Q2. Global housing markets wrongfooted us this quarter with housing markets displaying relative resilience. – Knight Frank

- Curtains drawing on runaway rise in global house prices: Reuters poll – Reuters

- City house prices outperform national housing markets in Q2. City prices stole a march on their national counterparts in Q2 2022, although neither saw the sudden downturn that many anticipated.

Posted by at 5:00 AM

Labels: Global Housing Watch

Saturday, September 3, 2022

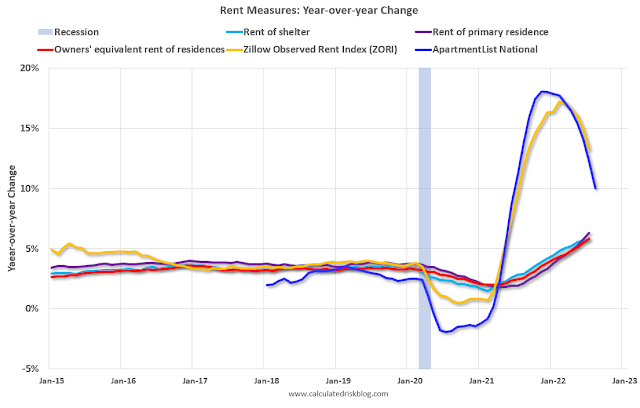

Apartment inflation

From the Grumpy Economist:

“This beautiful graph comes from calculatedriskblog.com. (Courtesy Andy Atkeson who used it in a nice discussion of a great paper by Ivan Werning at the Minneapolis Fed Foundations of Monetary Policy conference.)

The central lines that don’t move so much are the average rent. This is the quantity used by the Bureau of Labor Statistics to compute the consumer price index. The blue and yellow lines are the rent of new leases.

The first thing this informs is the economic theory of “sticky prices.” Apartment rents are a classic “sticky price;” the rent is fixed in dollar terms for a year. So, landlords deciding how much rent to charge, and people deciding how much they’re willing to pay, balance rents now vs. higher rents in the future. If everyone believes that inflation will be 10% over the next year, then it makes sense to raise the rent 5% now, and to pay the 5% higher rent, because the savings at the end of the year balance the cost in the beginning. (Obviously, the economics are much more subtle than this, but you get the idea.) And Voila’, you see it.

The graph also says there is some predictability and nomentum to inflation. Inflation should not be a surprise to forecasters. If you see rents on new leases much above average rents, it’s a pretty good bet that average rents will be rising in the future! This kind of phenomenon may be under exploited in formal inflation forecasting.

And, on the continuing speculation whether inflation will go away with interest rates still substantially below current inflation, the graph does seem a leading indicator that the rational expectations model is winning.”

From the Grumpy Economist:

“This beautiful graph comes from calculatedriskblog.com. (Courtesy Andy Atkeson who used it in a nice discussion of a great paper by Ivan Werning at the Minneapolis Fed Foundations of Monetary Policy conference.)

The central lines that don’t move so much are the average rent. This is the quantity used by the Bureau of Labor Statistics to compute the consumer price index.

Posted by at 8:56 AM

Labels: Global Housing Watch

Friday, September 2, 2022

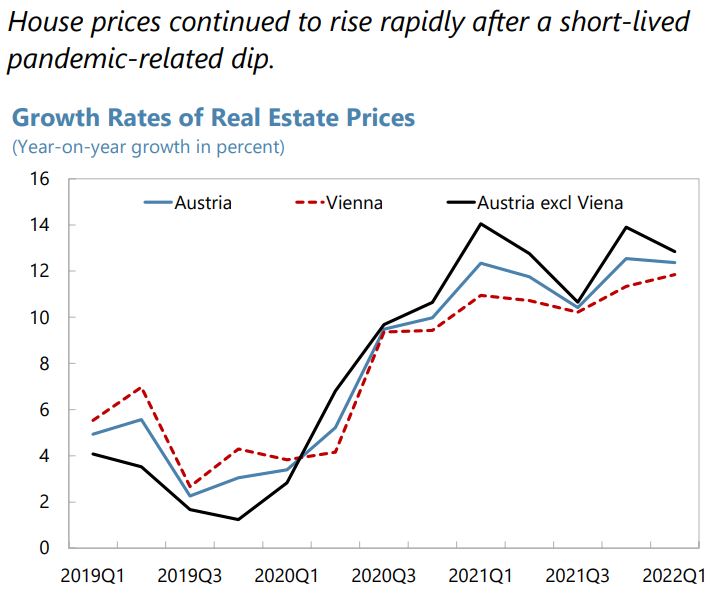

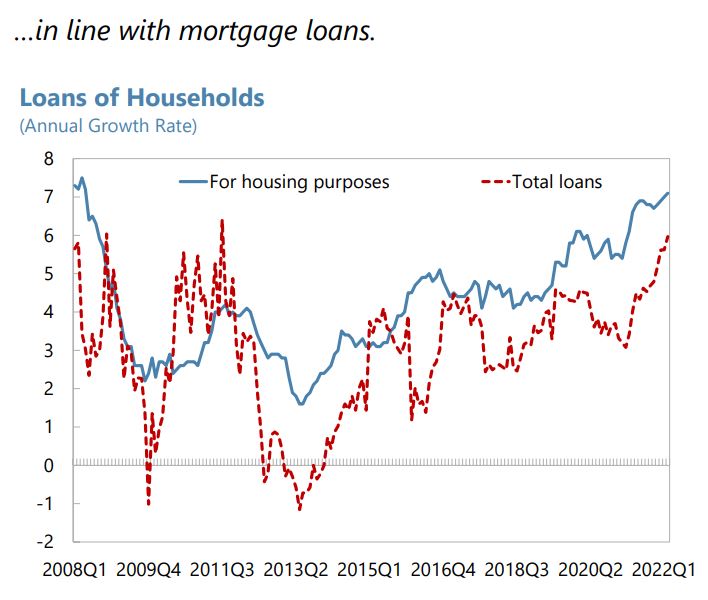

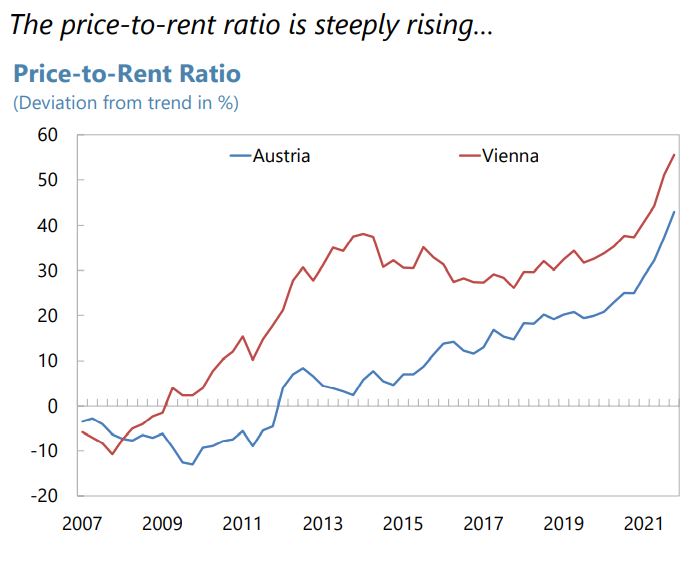

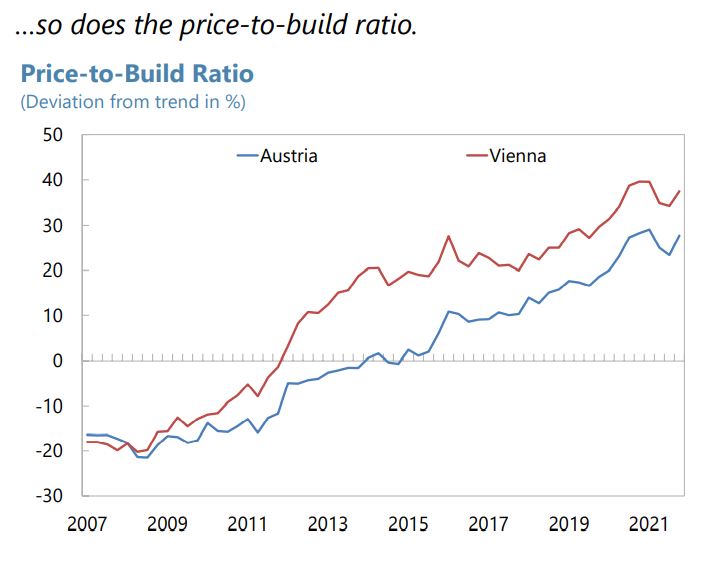

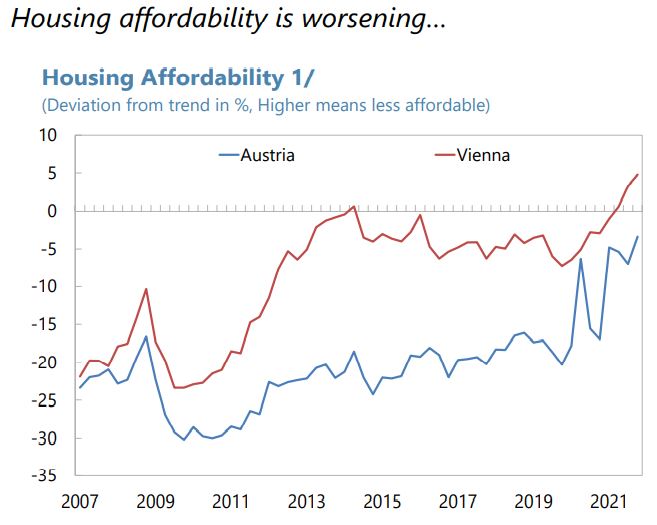

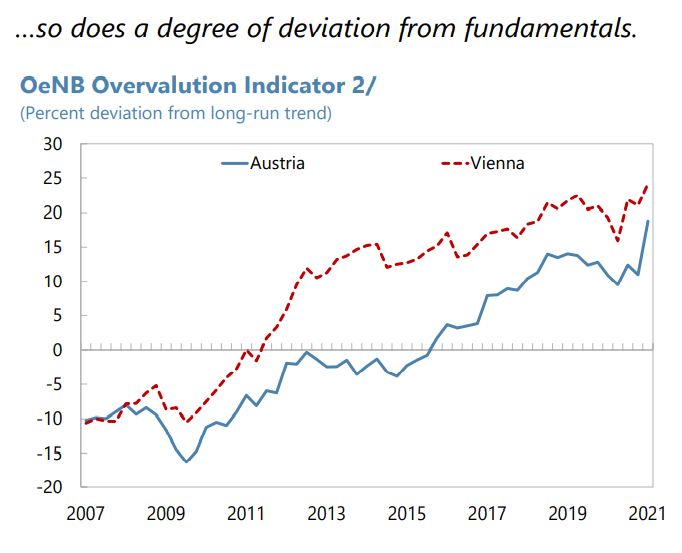

Housing Market in Austria

From the IMF’s latest report on Austria:

“The financial sector proved resilient during the pandemic but war- and housing-related risks have increased. (…) On the domestic front, house prices rose sharply and further deviated from fundamentals. Mortgage lending has risen considerably, much of which did not comply with Financial Market Stability Board (FMSB) recommendations on borrower-based limits.

(…)

Stricter enforcement of prudential guidelines is welcome, but a further tightening of borrower-based tools may be needed if housing-related systemic risks escalate. In response to risks from the residential real estate sector (RRE), the authorities—in line with staff recommendations—issued regulations to make binding upper limits for loan-to-value ratios (LTV), debt-service-to-income ratios (DSTI), and loan maturities, effective summer 2022. The existing guidance has also been adjusted to include a tighter upper DSTI limit for loans with variable rates. The authorities should carefully monitor the effectiveness of these measures and if vulnerabilities persist, additional macroprudential measures (such as a sectoral systemic risk buffer calibrated to RRE exposure) should be implemented. Depending on the evolution of the macroeconomic outlook and credit growth (currently slightly beyond prudential thresholds), the authorities could consider activating the counter-cyclical capital buffer (CCyB), which has thus far been kept at zero.

(…)

In the housing sector, the authorities plan to assess the effectiveness of the newly introduced legally binding borrower-based measures and stand ready to tighten further as needed. If the high credit growth does not fall to sustainable levels in the next 6-12 months, the authorities will have to consider activating the CCyB. The authorities stressed that retail deposits are adequately protected in the current DGSs. They deem that the mechanisms underpinning the conjoint solidarity and based on the principle of the DGS’s super seniority served financial stability appropriately in the liquidation of Sberbank Europe and recouping fully the outlays.”

From the IMF’s latest report on Austria:

“The financial sector proved resilient during the pandemic but war- and housing-related risks have increased. (…) On the domestic front, house prices rose sharply and further deviated from fundamentals. Mortgage lending has risen considerably, much of which did not comply with Financial Market Stability Board (FMSB) recommendations on borrower-based limits.

(…)

Stricter enforcement of prudential guidelines is welcome, but a further tightening of borrower-based tools may be needed if housing-related systemic risks escalate.

Posted by at 12:20 PM

Labels: Global Housing Watch

Subscribe to: Posts