Friday, September 2, 2022

Housing Market in Austria

From the IMF’s latest report on Austria:

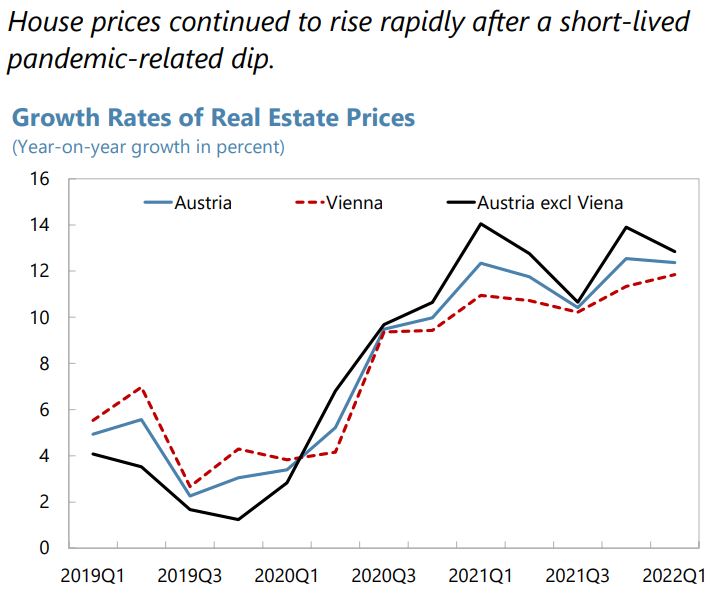

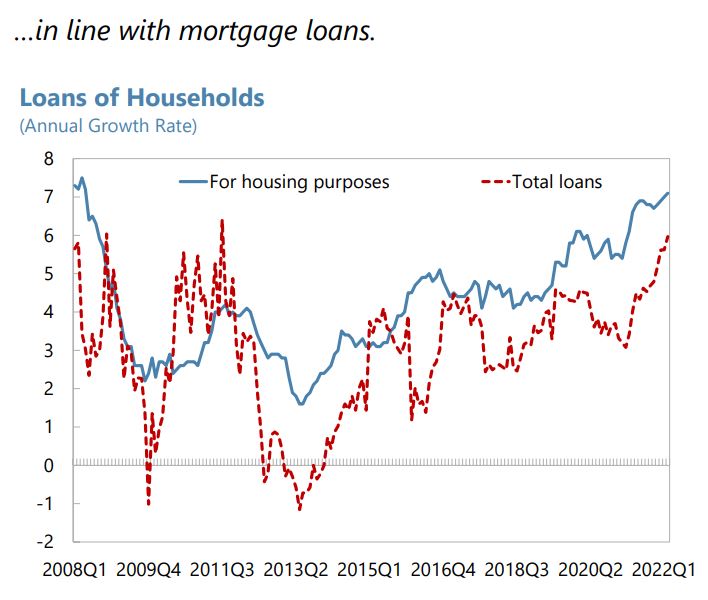

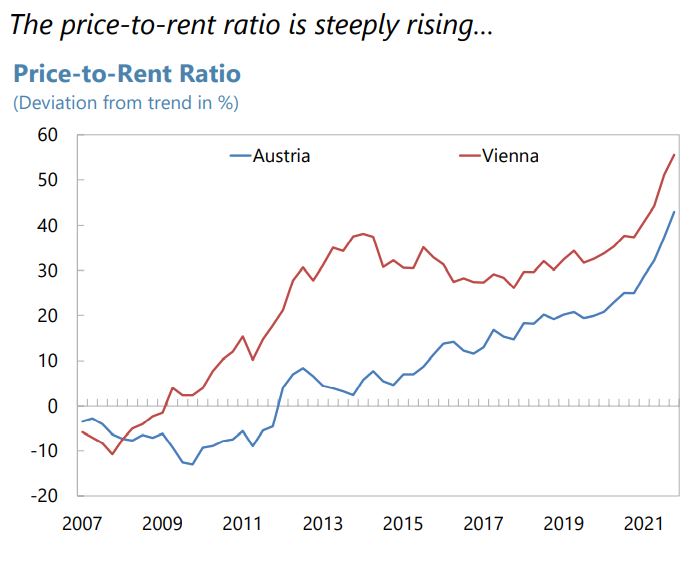

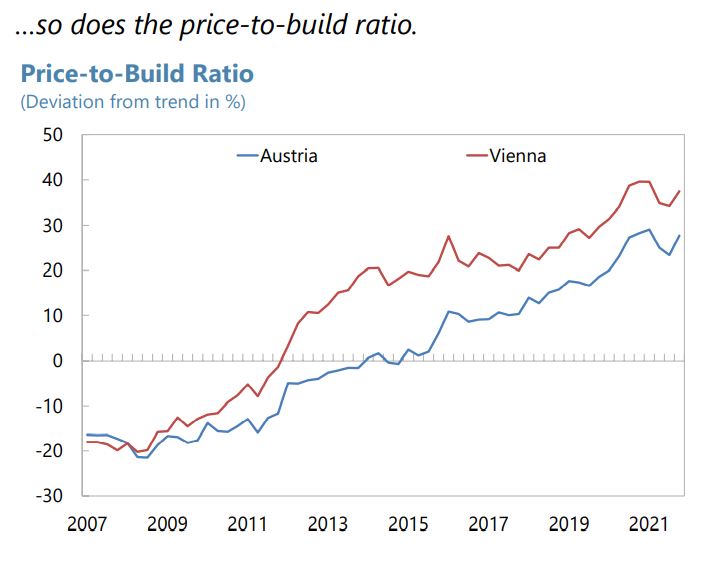

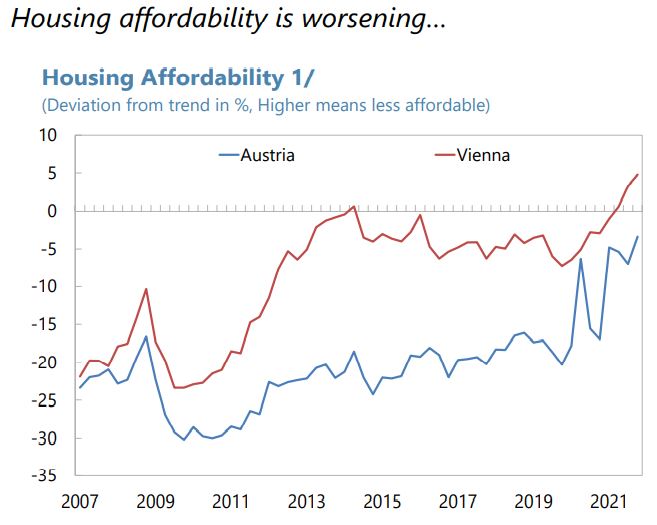

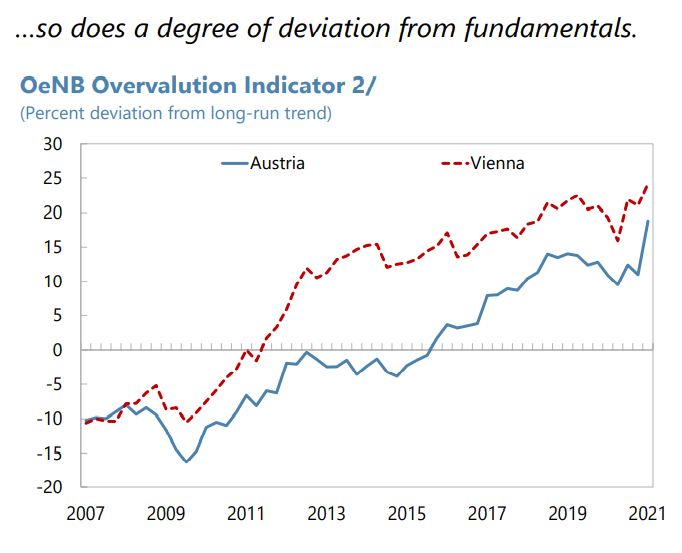

“The financial sector proved resilient during the pandemic but war- and housing-related risks have increased. (…) On the domestic front, house prices rose sharply and further deviated from fundamentals. Mortgage lending has risen considerably, much of which did not comply with Financial Market Stability Board (FMSB) recommendations on borrower-based limits.

(…)

Stricter enforcement of prudential guidelines is welcome, but a further tightening of borrower-based tools may be needed if housing-related systemic risks escalate. In response to risks from the residential real estate sector (RRE), the authorities—in line with staff recommendations—issued regulations to make binding upper limits for loan-to-value ratios (LTV), debt-service-to-income ratios (DSTI), and loan maturities, effective summer 2022. The existing guidance has also been adjusted to include a tighter upper DSTI limit for loans with variable rates. The authorities should carefully monitor the effectiveness of these measures and if vulnerabilities persist, additional macroprudential measures (such as a sectoral systemic risk buffer calibrated to RRE exposure) should be implemented. Depending on the evolution of the macroeconomic outlook and credit growth (currently slightly beyond prudential thresholds), the authorities could consider activating the counter-cyclical capital buffer (CCyB), which has thus far been kept at zero.

(…)

In the housing sector, the authorities plan to assess the effectiveness of the newly introduced legally binding borrower-based measures and stand ready to tighten further as needed. If the high credit growth does not fall to sustainable levels in the next 6-12 months, the authorities will have to consider activating the CCyB. The authorities stressed that retail deposits are adequately protected in the current DGSs. They deem that the mechanisms underpinning the conjoint solidarity and based on the principle of the DGS’s super seniority served financial stability appropriately in the liquidation of Sberbank Europe and recouping fully the outlays.”

Posted by at 12:20 PM

Labels: Global Housing Watch

Subscribe to: Posts