Wednesday, January 26, 2022

Housing Market in France

From the IMF’s latest report on France:

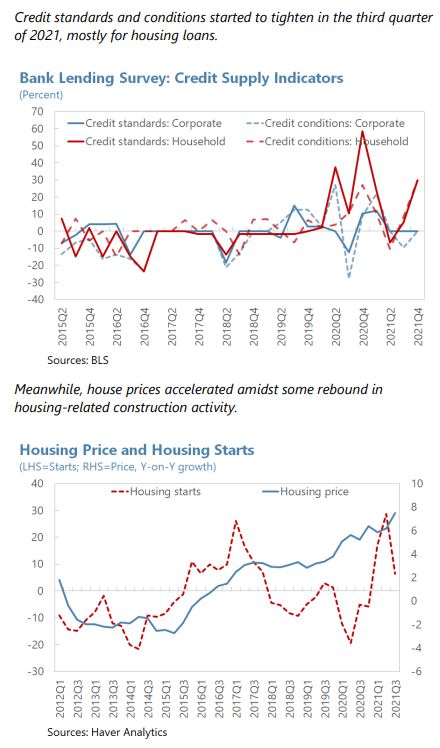

“Risks from real estate markets require continued vigilance. Over the last decade, household debt grew steadily from just below 60 percent to over 100 percent of disposable income and debt service to disposable income (DSTI) has increased. The deterioration reflects in part the need for higher debt to cover increasing housing prices, resulting in higher LTVs. Consequently, in 2019, the ESRB issued a warning related to medium-term vulnerabilities in the real estate sector, citing higher prices, weaker lending standards, elevated household debt, and rapid mortgage lending growth in France. While supervisory action by the High Council for Financial Stability (HCSF) has capped the deterioration in lending standards, low interest rates, a relatively inelastic housing supply and increased demand for home renovations continued to fuel real estate price growth in 2020 and 2021.

Several features in France can attenuate risks from market corrections to mortgage defaults, but banks’ profits could be at risk. Household repayment risks are contained because, among other factors, mortgage interest rates are fixed, and employment losses are protected by unemployment insurance. Banks are partially protected from potential losses predominantly through mortgage insurance, and borrowers’ legal obligations. However, profit margins on housing loans are estimated to be nil or even negative since 2017. Thus, the large volume of mortgages with long residual maturity and low fixed interest rate creates a persistent risk to bank profitability, which would intensify with selected defaults or increased funding costs of banks.

(…)

To limit excessive risk-taking by banks, borrower-based measures should be maintained and expanded. To shield banks from loan losses, the HCSF issued recommendations (declared legally binding as of January 1, 2022) that banks must limit mortgage length to 25 years and DSTI to 35 percent (up from 33 percent in the guidance)—with up to 20 percent of new mortgage loans excluded primarily for owner-occupied housing. As a result, banks have actively adjusted their lending practices, with falling DSTI. As of August 2021, the banking sector was within the flexibility margin. However, fueled by low interest rates and a relatively inelastic housing supply, house prices continued to increase and mortgage debt-to income remains elevated, reflecting the need to cover increasing housing prices. In addition, downside risks from structural factors remain, such as weak banking sector profitability due to persistently low rates and high cost-to-income ratios, banks’ high market risk exposure, wholesale funding risk, cyber security, and climate change risks. If these trends continue, fine tuning existing borrower-based measures or deploying complementary measures, such as the now available (sectoral) systemic risk buffer, may become appropriate to more broadly limit excessive risk-taking.”

Posted by at 10:07 AM

Labels: Global Housing Watch

Subscribe to: Posts