Monday, January 24, 2022

Fair and Inclusive Markets: Why Fostering Dynamism Matters

Source: VoxEU CEPR

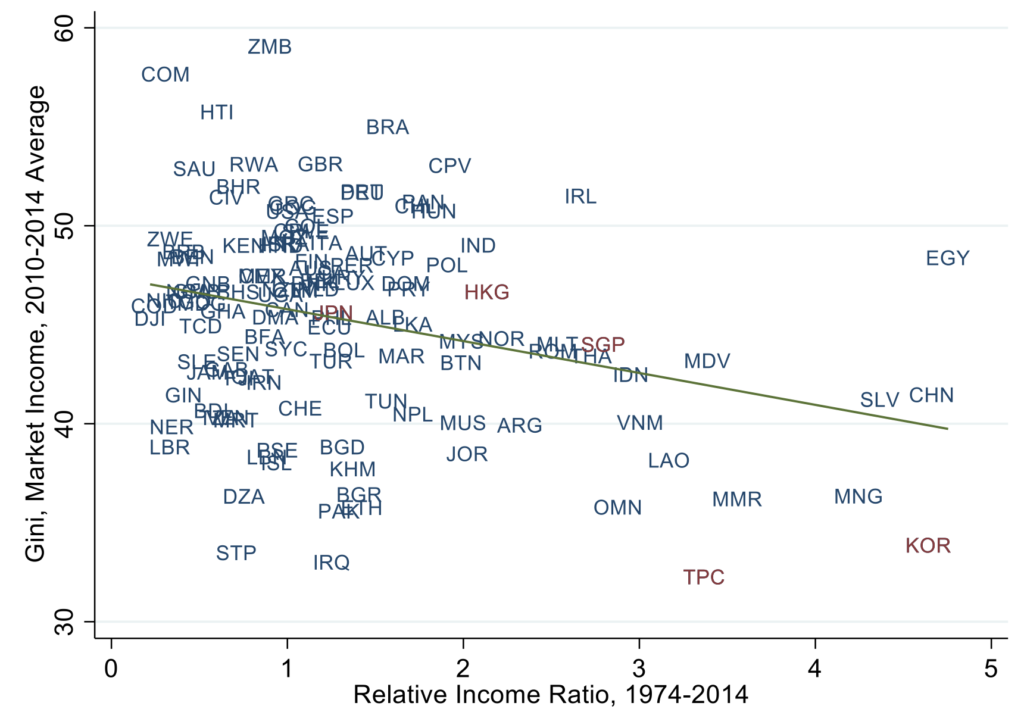

“Rising inequality and firms’ market power pose challenges to the aims of inclusive growth and shared prosperity. Nevertheless, growth and equity need not be mutually exclusive. This column argues that economic dynamism is crucial for achieving sustained growth and more equal market outcomes (Figure 1). It shows that countries that experienced faster growth over the last four decades have lower market inequality in the 2010s. Policy should be aimed at supporting sophisticated export industries, fostering innovation and creative destruction, and promoting competition.“

Figure 1: Relationship between long-run economic growth and market inequality (1974-2014)

Source: VoxEU CEPR

“Rising inequality and firms’ market power pose challenges to the aims of inclusive growth and shared prosperity. Nevertheless, growth and equity need not be mutually exclusive. This column argues that economic dynamism is crucial for achieving sustained growth and more equal market outcomes (Figure 1). It shows that countries that experienced faster growth over the last four decades have lower market inequality in the 2010s. Policy should be aimed at supporting sophisticated export industries,

Posted by at 12:58 PM

Labels: Inclusive Growth

Want to make better forecasts? Here are two traps to avoid

New post from livewire by JOEY MUI of Merlon Capital

“The problem with precision

Most forecasts begin with a starting point which is often anchored to current data. Forecasters tend to modestly extrapolate up or down from this level. This tendency to stick close to current conditions, or consensus views, limits a forecaster’s ability to comprehend the full range of possibilities or the impacts of more extreme circumstances.

Research by the International Monetary Fund explored the ability of economists to predict recessions between 1992 to 2014. It was a disaster. Economists consistently failed to predict a recession in GDP by a significant margin. Even as conditions deteriorated, economists stubbornly anchored their forecasts to the preceding non-recessionary period and adjusted their predictions downwards too little, too late.”

Click here to read more.

New post from livewire by JOEY MUI of Merlon Capital

“The problem with precision

Most forecasts begin with a starting point which is often anchored to current data. Forecasters tend to modestly extrapolate up or down from this level. This tendency to stick close to current conditions, or consensus views, limits a forecaster’s ability to comprehend the full range of possibilities or the impacts of more extreme circumstances.

Research by the International Monetary Fund explored the ability of economists to predict recessions between 1992 to 2014.

Posted by at 7:57 AM

Labels: Forecasting Forum

Data Sources Compendium [Updated]

From Econbrowser:

“Update of The Data Will Set You Free (in preparation for a new semester!)

In an era of easily accessible databases, am constantly amazed that people write stuff that is easily falsifiable. Or ask me for the “raw” data when it’s freely available via a aggregating database I’ve provided the hyperlink (most galling is when they then accuse me of misquoting data sources).

Just to remind the frequent commenters on this blog, freely available and documented data available here:

St. Louis Fed economic database Thousands of time series on economic activity, in an easily downloadable form.

IMF International Financial Statistics

IMF World Economic Outlook databases.

World Bank World Development Indicators.

DBnomics (a “European FRED”)

YCharts Macro and equity market data series.

ino.com Futures data.

Federal Reserve Board data Monetary, financial and output data collected by the Nation’s central bank.

Bureau of Economic Analysis, Dept. of Commerce Data on GDP and components (the national income and product accounts) as well as other macroeconomic data.

Bureau of the Census, Dept. of Commerce Data on the characteristics of the US population US firms, as well as other data.

Bureau of Labor Statistics, Dept. of Labor Data on wages, prices, productivity, and employment and unemployment rates.

Energy Information Agency, Dept. of Energy Data on energy (electricity, gas, petroleum) production, consumption and prices.

Economic Report of the President, various years. The back portion of this annual publication contains about 70 tables of government economic data.

Economic Indicators CEA and JEC Compilation of economic data in tabular form.

Economic Time Series page A large collection of economic time series.

NBER Data Specialized economic databases created by economists associated with the National Bureau of Economic Research.

Netherlands Bureau for Economic Policy Analysis World Trade Monitor

World Bank, A Global Database of Inflation.

Jordà-Schularick-Taylor Macrohistory Database

Usually I cite FRED or BEA and/or BLS via FRED, or from the above data sources. In certain cases, I have written papers using specialized data sources. Below are links to those data sources.”

Continue reading here.

From Econbrowser:

“Update of The Data Will Set You Free (in preparation for a new semester!)

In an era of easily accessible databases, am constantly amazed that people write stuff that is easily falsifiable. Or ask me for the “raw” data when it’s freely available via a aggregating database I’ve provided the hyperlink (most galling is when they then accuse me of misquoting data sources).

Posted by at 7:07 AM

Labels: Macro Demystified

Sunday, January 23, 2022

Kevin Erdmann was right

From Econlib:

“Back in 2009-10, I did a number of posts criticizing the theory that rising house prices in the early 2000s represented a “bubble”. In one post, I pointed to an article in The Economist that criticized Eugene Fama, and bragged that they had presciently foreseen the housing bubble. In fact, the specific predictions they cited (from an 2003 advertisement for The Economist, since deleted) turned out to be almost entirely wrong, indeed wildly off base.

The Economist did not take kindly to my post:

Mr Sumner disagrees. He seems to think it’s funny that The Economists pent much of the last decade warning that, globally, home prices were rising in a troubling manner. Contrarianism is fun and all, but this strikes me as an odd way to process the experiences that led us to this point.

I would note that Free Exchange seemed to enjoy making fun of Fama’s views.

Now The Economist has seen the light:

Perhaps it is just a matter of time before the house of cards collapses. But as a recent paper by Gabriel Chodorow-Reich of Harvard University and colleagues explains, what might appear to be a housing bubble may in fact be the product of fundamental economic shifts. The paper shows that the monumental house-price increases in America in the early to mid-2000s were largely a consequence of factors such as urban revitalisation, growing preferences for city living and rising wage premia for educated workers in cities. By 2019 American real house prices had pretty much regained their pre-financial-crisis peak, further evidence that the mania of the mid-2000s was perhaps not quite so mad after all.

Fundamental forces may once again explain why house prices today are so high—and why they may endure. Three of them stand out: robust household balance-sheets; people’s greater willingness to spend more on their living arrangements; and the severity of supply constraints.”

From Econlib:

“Back in 2009-10, I did a number of posts criticizing the theory that rising house prices in the early 2000s represented a “bubble”. In one post, I pointed to an article in The Economist that criticized Eugene Fama, and bragged that they had presciently foreseen the housing bubble. In fact, the specific predictions they cited (from an 2003 advertisement for The Economist, since deleted) turned out to be almost entirely wrong,

Posted by at 2:19 PM

Labels: Global Housing Watch

Paul Krugman and Tyler Cowen on the housing boom

From Marginal Revolution:

“Paul Krugman is coming very close to admitting a) “real estate bubble” was not the best formulation, and b) Kevin Erdmann was right.”

Tweets from Paul Krugman:

“Aha. An economic mystery solved, I think (with a suggestion from Charlie Steindel). I’ve been noting that we’re currently seeing a surge in real house prices up to 2000s-bubble levels 1/

But the 2000s bubble was geographically very uneven: prices surged in cities with strict zoning, but not in places where developers were free to sprawl => elastic housing supply. This time the price rise is across the board, in fact in some cases higher in sprawl areas 2/

Eg Atlanta v Boston, on a log scale so you can see proportional differences: Boston >> Atlanta last time, if anything Atlanta > Boston now 3/

What’s going on? The answer surely involves weak supply response 4/

And that in turn points to our old friend disrupted supply chains, which have made construction very expensive 5/

Suggests that prices may eventually fall in smaller/less zoned cities, once houses can be built in large numbers 6/”

From Marginal Revolution:

“Paul Krugman is coming very close to admitting a) “real estate bubble” was not the best formulation, and b) Kevin Erdmann was right.”

Tweets from Paul Krugman:

“Aha. An economic mystery solved, I think (with a suggestion from Charlie Steindel). I’ve been noting that we’re currently seeing a surge in real house prices up to 2000s-bubble levels 1/

But the 2000s bubble was geographically very uneven: prices surged in cities with strict zoning,

Posted by at 2:06 PM

Labels: Global Housing Watch

Subscribe to: Posts