Tuesday, August 8, 2017

Stabilizing the System of Mortgage Finance in the United States

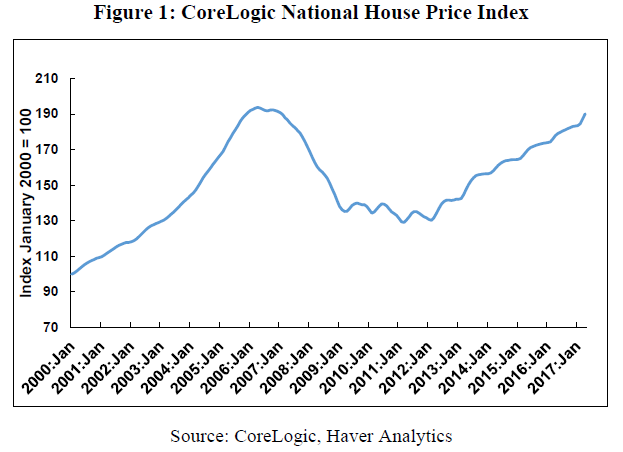

A new IMF Working Paper by Richard Koss says that “It has been over a decade since the peak of house prices in the US was attained, and while there has been a concerted regulatory response to the subsequent collapse, the two Government Sponsored Enterprises (GSEs) remain in conservatorship. While this action served to forestall a deeper crisis at the time, over the past several years risks related to the system of mortgage finance can be seen building across several dimensions that need to be addressed. While reforms to the GSEs are an important part of dealing with these concerns, this paper argues that broader changes need to be made across the entire mortgage landscape to stabilize the system, even before the final state of the GSEs is fully determined.”

Continue reading here.

A new IMF Working Paper by Richard Koss says that “It has been over a decade since the peak of house prices in the US was attained, and while there has been a concerted regulatory response to the subsequent collapse, the two Government Sponsored Enterprises (GSEs) remain in conservatorship. While this action served to forestall a deeper crisis at the time, over the past several years risks related to the system of mortgage finance can be seen building across several dimensions that need to be addressed.

Posted by at 4:12 PM

Labels: Global Housing Watch

Friday, August 4, 2017

Housing View – August 4, 2017

On cross-country:

- Housing in Euro Area – IMF

On the US:

- Why Has Regional Income Convergence in the U.S. Declined? – NBER

- 2017 Profile of International Activity in U.S. Residential Real Estate – National Association of Realtors

- Remarks of Melvin L. Watt at the National Association of Real Estate Brokers’ 70th Annual Convention – Federal Housing Finance Agency

- Matthew Desmond Q&A: Housing Insecurity Is a Problem We Need to ‘Out-Hate’ – Zillow

- Tenants Under Siege: Inside New York City’s Housing Crisis – The New York Review of Books

- Why is Moving to a New Home Worse for African-American and Hispanic Children than for White Children? – Harvard Joint Center for Housing Studies

- Housing Policy Should Prioritize Those With Greatest Need – Center on Budget and Policy Priorities

- Where Does Job Growth Outpace New Housing Construction? – National Association of Realtors

- The Sharing Economy and Housing Affordability: Evidence from Airbnb – SSRN

- Residential Rent Affordability across U.S. Metropolitan Areas – Federal Reserve Bank of Kansas City

- Mortgage Default in an Estimated Model of the U.S. Housing Market – Banco de México

- Understanding the Surge in Commercial Real Estate Lending – Federal Reserve Bank of Richmond

- Increase in Long Commutes Indicates More Residential Dispersion – New Geography

- The Great Train Robbery: Urban Transportation in the 21st Century – Chapman University

On other countries:

- [Australia] Quarterly Housing & Economic Review – July 2017 – CoreLogic

- [Canada] Vancouver plan to boost housing supply ignores city hall red tape – Fraser Institute

- Japan: Risks Emerging from Real Estate? – IMF

- [Singapore] Housing Market in Singapore – IMF

- [Turkey] Real estate purchases by foreigners drop in Turkey, despite generous incentives – Global Property Guide

- [United Kingdom] British homeowners move home half as frequently as Americans do – The Economist

- [United Kingdom] How the credit crunch transformed the UK housing market – Savills

- [United Kingdom] Making the Case for Affordable Housing on Public Land – New Economics Foundation

On cross-country:

- Housing in Euro Area – IMF

On the US:

- Why Has Regional Income Convergence in the U.S. Declined? – NBER

- 2017 Profile of International Activity in U.S. Residential Real Estate – National Association of Realtors

- Remarks of Melvin L. Watt at the National Association of Real Estate Brokers’ 70th Annual Convention – Federal Housing Finance Agency

- Matthew Desmond Q&A: Housing Insecurity Is a Problem We Need to ‘Out-Hate’

Posted by at 5:00 AM

Labels: Global Housing Watch

Tuesday, August 1, 2017

Bridging the Gap: Forecasting Interest Rates with Macro Trends

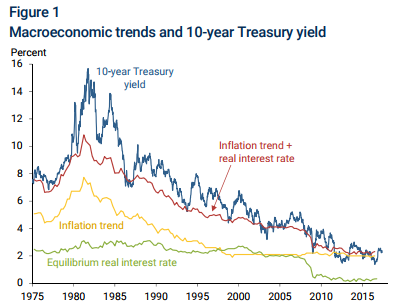

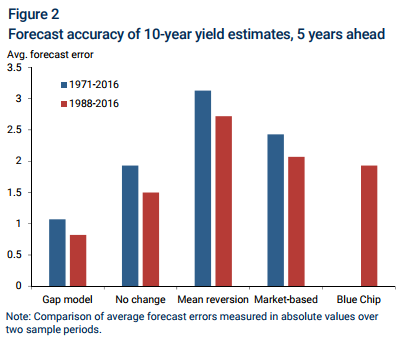

A new economic letter by Michael Bauer says that “Interest rates are inherently difficult to predict, and the simple random walk benchmark has proven hard to beat. But macroeconomics can help, because the long-run trend in interest rates is driven by the trend in inflation and the equilibrium real interest rate. When forecasting rates several years into the future, substantial gains are possible by predicting that the gap between current interest rates and this long-run trend will close with increasing forecast horizon. This evidence suggests that accounting for macroeconomic trends is important for understanding, modeling, and forecasting interest rates.”

Continue reading here.

A new economic letter by Michael Bauer says that “Interest rates are inherently difficult to predict, and the simple random walk benchmark has proven hard to beat. But macroeconomics can help, because the long-run trend in interest rates is driven by the trend in inflation and the equilibrium real interest rate. When forecasting rates several years into the future, substantial gains are possible by predicting that the gap between current interest rates and this long-run trend will close with increasing forecast horizon.

Posted by at 9:49 AM

Labels: Forecasting Forum

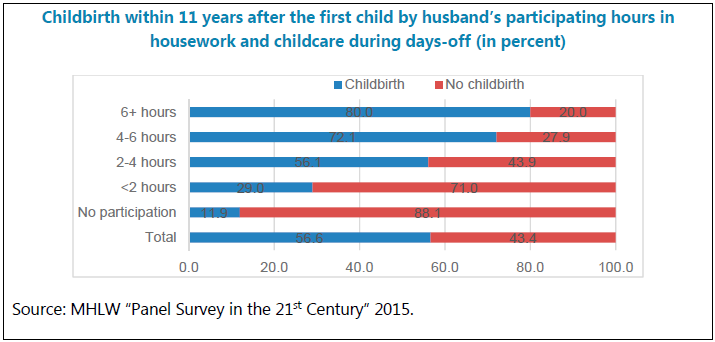

Japan’s Lifetime Employment and Gender Inequality

A new IMF report finds that “Societal attitudes in which males contribute to household work could be a powerful lever both to increase female labor force participation, and increase fertility. If women can get more child rearing support from their husbands, it would be easier for them to continue to work. However, with 85 percent of full-time employees working overtime, it is difficult in reality to share the childcare burdens among a working couple if both of them have regular works. Men’s commitment to house work and family responsibilities can have a significant impact on fertility. Data suggests that the more time spent by a husband in house work and childcare, the higher the changes that couples will have a second child.”

Continue reading here.

A new IMF report finds that “Societal attitudes in which males contribute to household work could be a powerful lever both to increase female labor force participation, and increase fertility. If women can get more child rearing support from their husbands, it would be easier for them to continue to work. However, with 85 percent of full-time employees working overtime, it is difficult in reality to share the childcare burdens among a working couple if both of them have regular works.

Posted by at 9:44 AM

Labels: Inclusive Growth

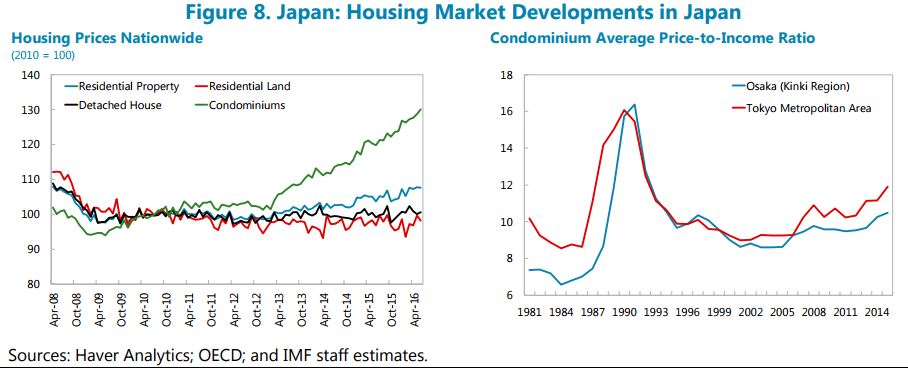

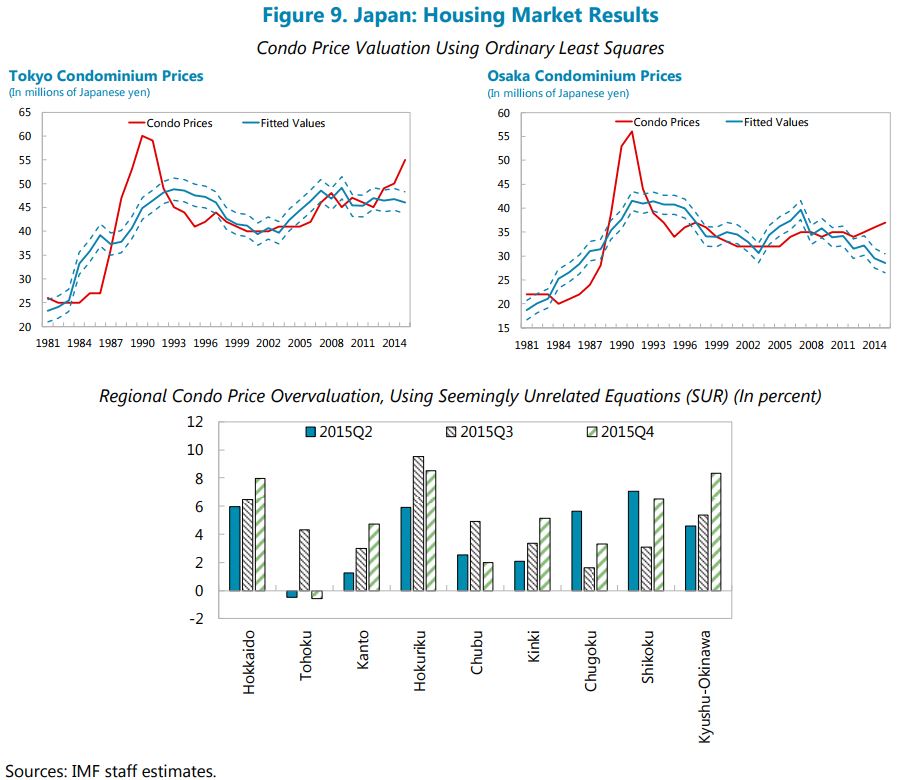

Japan: Risks Emerging from Real Estate?

From a new IMF report on Japan:

“Housing prices have been on the rise in some geographic areas and market segments, despite the declining population. Condominium prices have increased by 23 percent at the national level since 2013 (Figure 8). Historically low mortgage rates and recent changes in the inheritance tax are contributing to demand pressures, with little response in the number of new houses put on the market. Some overheating in the housing market is also indirectly suggested by house price-to-income ratios. Growth in real estate loans has been higher than other loans and the amount outstanding by domestic and Shinkin banks reached a record high at end-December 2016 (FSR, April 2017).”

“Condominium prices appear to be moderately overvalued in Tokyo, Osaka, and several outer regions. While results should be interpreted with caution given data limitations and model uncertainty, an econometric analysis using city data shows that condominium prices in Tokyo and Osaka started exceeding values predicted by fundamentals in 2013, suggesting an overvaluation in the 15−20 percent range. A regional analysis also indicates that condominium prices may be moderately above their equilibrium values, with the degree of overvaluation in the 5−10 percent range (Figure 9).”

From a new IMF report on Japan:

“Housing prices have been on the rise in some geographic areas and market segments, despite the declining population. Condominium prices have increased by 23 percent at the national level since 2013 (Figure 8). Historically low mortgage rates and recent changes in the inheritance tax are contributing to demand pressures, with little response in the number of new houses put on the market. Some overheating in the housing market is also indirectly suggested by house price-to-income ratios.

Posted by at 9:22 AM

Labels: Global Housing Watch

Subscribe to: Posts