Tuesday, August 1, 2017

Bridging the Gap: Forecasting Interest Rates with Macro Trends

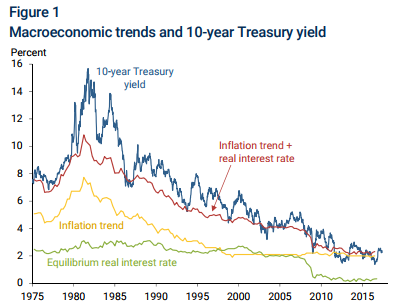

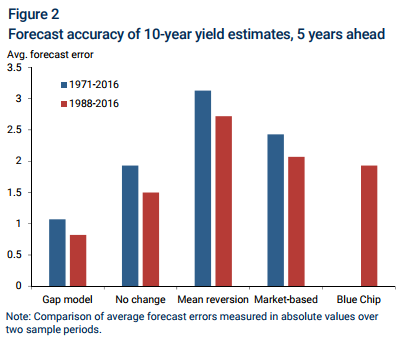

A new economic letter by Michael Bauer says that “Interest rates are inherently difficult to predict, and the simple random walk benchmark has proven hard to beat. But macroeconomics can help, because the long-run trend in interest rates is driven by the trend in inflation and the equilibrium real interest rate. When forecasting rates several years into the future, substantial gains are possible by predicting that the gap between current interest rates and this long-run trend will close with increasing forecast horizon. This evidence suggests that accounting for macroeconomic trends is important for understanding, modeling, and forecasting interest rates.”

Continue reading here.

Posted by at 9:49 AM

Labels: Forecasting Forum

Subscribe to: Posts