Monday, July 31, 2017

Housing Market in Singapore

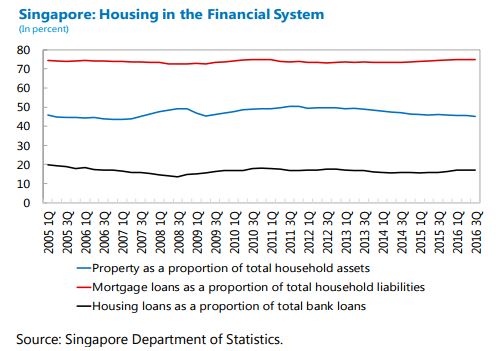

A new IMF report on Singapore says that: “In Singapore, property market stability is closely linked to macroeconomic and financial stability. Property is the largest component of household wealth, representing about half of total household assets. Mortgage loans account for some three-quarters of total household liabilities, and property-related loans form a substantial portion of banks’ loan books. In addition, housing affordability is a key concern for the Singapore public (Lum, 1996 and 2011; Phang, 2015; Phang and others, 2013). Therefore, when property prices rose rapidly shortly after the Global Financial Crisis (GFC), the Singapore authorities responded with a series of macroprudential measures, including fiscal-based measures, to promote a more stable and sustainable property market. ”

The report also says that: “Finally, Singapore’s banks are well-positioned to withstand shocks from the property market, partly as a result of macro-prudential tightening. Average loan-to-value ratios are low, loan-loss coverage is adequate, and capital and liquidity buffers are strong. Households also have healthy balance sheets and well-diversified assets. ”

On international comparison, the report says that “In Hong Kong SAR, Singapore, and Taiwan Province of China, property tightening measures in recent years have achieved different results. Since peaking in 2013, house prices in Singapore have declined gradually to 2010 levels. The impact contrasts with Hong Kong SAR, where prices have continued to rise and mortgage growth has shown no clear downward trend. House price growth has also remained rapid in New Zealand and Australia where tightening began in 2013 and 2014 respectively. Hence, there is significant liquidity in the regional markets calling for continued vigilance and careful calibration of the measures to guard against speculative capital inflows that can hamper financial stability.”

Posted by at 11:41 AM

Labels: Global Housing Watch

Subscribe to: Posts