Wednesday, February 7, 2018

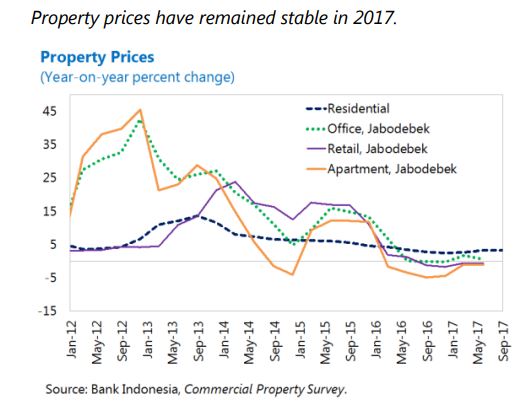

House Prices in Indonesia

From the IMF’s latest report on Indonesia:

Posted by at 10:23 AM

Labels: Global Housing Watch

Friday, February 2, 2018

Country Experiences With Macroprudential Policies

Below is a list of papers put together by the Bank for International Settlements. The list shows the experience of emerging market economies with designing macroprudential frameworks and implementing macroprudential instruments.

- [Brazil] Macroprudential policy in Brazil

- [Chile] Macroeconomic and financial volatility and macroprudential policies in Chile

- [Colombia] The macroprudential policy framework in Colombia

- [Czech Republic] Should monetary policy pay attention to house prices? The Czech National Bank’s approach

- [Hong Kong] Hong Kong’s property market and macroprudential measures

- [Hungary] Regionally-differentiated debt cap rules: a Hungarian perspective

- [India] Macroprudential frameworks, implementation, and relationship with other policies

- [Indonesia] Indonesia: the macroprudential framework and the central bank’s policy mix

- [Israel] Assessing the impact of macroprudential tools: the case of Israel

- [Korea] Macroprudential frameworks, implementation and relationship with other policies in Korea

- [Malaysia] Macroprudential frameworks: Implementation, and relationship with other policies – Malaysia

- [Peru] Implementation of macroprudential policy in Peru

- [Philippines] Macroprudential frameworks, implementation, and communication strategies – The Philippines

- [Russia] The macroprudential policy framework in Russia

- [Singapore] Macroprudential policies: A Singapore case study

- [Thailand] Macroprudential framework – the case of Thailand

- [Turkey] Financial stability and macroprudential policy in Turkey

Below is a list of papers put together by the Bank for International Settlements. The list shows the experience of emerging market economies with designing macroprudential frameworks and implementing macroprudential instruments.

Posted by at 10:02 AM

Labels: Global Housing Watch

Housing View – February 2, 2018

On cross-country:

- Friend or Foe? Cross-Border Linkages, Contagious Banking Crises, and “Coordinated” Macroprudential Policies – IMF

- Quarterly Review of European Mortgage Markets – European Mortgage Federation

- More Mortgages, More Homes? The Effect of Housing Financialization on Homeownership in Historical Perspective – Sage Journals

On the US:

- Mayors Take the Fight for Affordable Housing to Capitol Hill – Citylab, Seattle Times

- Eliminating the mortgage tax deduction could boost homeownership – Marginal Revolution

- National Mortgage Risk Index (NMRI) and Other Risk Measures – American Enterprise Institute

- Rent Control: A Reckoning – Citylab

- My 10-Year Odyssey Through America’s Housing Crisis – Wall Street Journal

- Real House Prices and Price-to-Rent Ratio in November – Calculated Risk

- Can Small Housing Units Help Meet the Need for Affordable Housing in New York City? – NYU Furman Center

- Infrastructure Plans Should Invest in Affordable Housing – Center on Budget and Policy Priorities

On other countries:

- [Canada] Canada’s housing markets remain highly vulnerable overall – Canada Mortgage and Housing Corporation

- [Canada] 5 Predictions for Canada’s Housing Market in 2018 – Dundurn

- [Denmark] Housing Market Analysis for the Capital Region of Denmark: Housing Shortage, Urban Development Potentials, and Strategies – Copenhagen Economics

- [Ireland] Tight property supply constrains Dublin’s Brexit appeal – Financial Times

- [Malta] Housing Market in Malta – IMF

- [Netherlands] Spatial Planning and Segmentation of the Land Market: The Case of the Netherlands – Land Economics

- [Netherlands] Strong correlation between consumption and house prices in the Netherlands – De Nederlandsche Bank

- [New Zealand] Housing Quarterly Report – New Zealand Government

- [United Kingdom] Housing Market Renewal revisited: a defence of place based policy in austere times – Sheffield Hallam University

- [United Kingdom] Sleep tight: can the ‘tiny homes’ movement redefine holidays? – Financial Times

- [United Kingdom] London developers face growing activism over affordable housing – Financial Times

- [United Arab Emirates] Dubai: Survival of the Fittest – REIDIN

- [United Arab Emirates] UAE Residential Market Overview – December Results – REIDIN

Photo by Aliis Sinisalu

On cross-country:

- Friend or Foe? Cross-Border Linkages, Contagious Banking Crises, and “Coordinated” Macroprudential Policies – IMF

- Quarterly Review of European Mortgage Markets – European Mortgage Federation

- More Mortgages, More Homes? The Effect of Housing Financialization on Homeownership in Historical Perspective – Sage Journals

On the US:

- Mayors Take the Fight for Affordable Housing to Capitol Hill – Citylab,

Posted by at 5:00 AM

Labels: Global Housing Watch

Adapting to Climate Change: Pricing Right, Taxing Smart, and Acting Now

From a speech by IMF Deputy Managing Director Zhang Tao at the United Nations Investor Summit on Climate Risk

“We recently have seen the IMF appearing to step up its work on climate change. Why now?

The Short Answer: This is our response to the threat climate change poses to our planet—and the growing demand from our membership and the international community to respond.

The IMF has been involved in the climate change work for several years. Our recent work reflects compelling evidence that adapting to climate change is one of the most important challenges facing economic policy makers worldwide. The IMF also has an obligation as a member of international community to address the doubts about climate change with fact-based analysis.

The Long Answer: the Fund’s core mandate is to ensure economic stability and resilience. Climate change could prove to be a destabilizing force for the global economy if it is not addressed.

The macroeconomic impact of climate change was illustrated by the especially damaging hurricane season last year in the Caribbean and the U.S. We certainly will see more frequent and more damaging such natural disasters in the future.

So, the key question is what we can do—and do better—in helping policymakers confront the challenges of climate change?

Two key areas of work are: mitigation, which includes helping countries meet their commitments under the Paris Agreement to reduce emissions; and adaptation, which focuses on building resilience to climate change. Our general message to our membership with regard to meeting the goals of the Paris agreement to contain emissions is to “price it right; tax it smart; and do it now.” ”

Continue reading here.

From a speech by IMF Deputy Managing Director Zhang Tao at the United Nations Investor Summit on Climate Risk

“We recently have seen the IMF appearing to step up its work on climate change. Why now?

The Short Answer: This is our response to the threat climate change poses to our planet—and the growing demand from our membership and the international community to respond.

The IMF has been involved in the climate change work for several years.

Posted by at 1:30 AM

Labels: Energy & Climate Change

Thursday, February 1, 2018

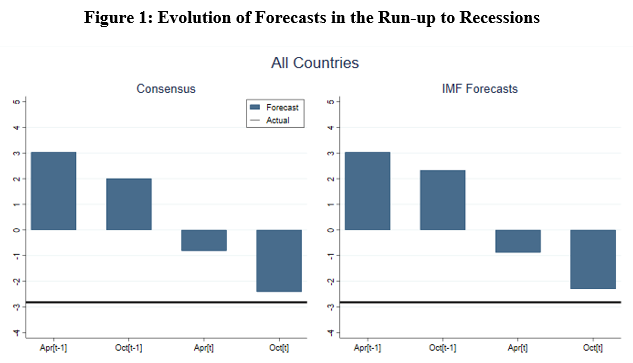

How Well Do Economists Forecast Recessions? A Groundhog Day Update

In 2000, I wrote in the Financial Times that “the record of failure to predict recessions is virtually unblemished.” In time for Groundhog Day, my colleague Zidong An, Joao Jalles and I have updated my analysis so that it now covers the years 1992 to 2014 and 63 countries. We find that there is little reason to change my assessment. Like Bill Murray, I am reliving the same moment.

In 2000, I wrote in the Financial Times that “the record of failure to predict recessions is virtually unblemished.” In time for Groundhog Day, my colleague Zidong An, Joao Jalles and I have updated my analysis so that it now covers the years 1992 to 2014 and 63 countries. We find that there is little reason to change my assessment. Like Bill Murray, I am reliving the same moment.

Posted by at 10:53 AM

Labels: Forecasting Forum

Subscribe to: Posts