Thursday, October 18, 2018

Highlights of the Economic Outlook for the Euro Area

From the Economic Outlook for the Euro Area in 2018 and 2019:

“Signs of a slowing world economy are piling up: Since the beginning of the year purchasing manager indices have been declining globally, in summer higher US interest rates led investors to withdraw capital from emerging markets, and as a consequence, capital costs rose and currencies depreciated in many emerging markets economies. In October stock prices decreased markedly worldwide including the US, despite the strong upswing in this country.

As a consequence of the turmoil on financial markets, monetary conditions in many emerging economies are no longer favorable. What ultimately counts for the prospects of the global economy, is, however, the performance of the US, the Euro area, China and Japan. The upswing in the US appears stable enough to continue well into 2019. While at present the rest of the group appears to lose momentum, there is a good chance that production in each of these economies will still expand at rates that are close to their potential growth. Further protectionist rounds are the most important risk to this scenario.”

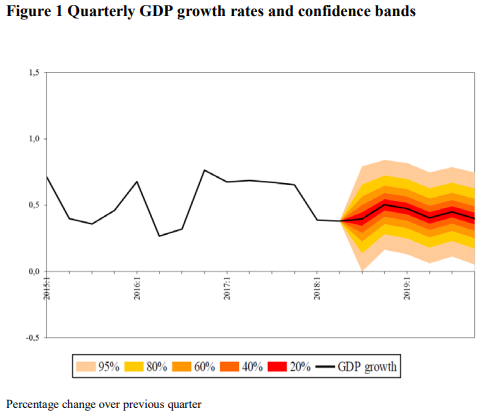

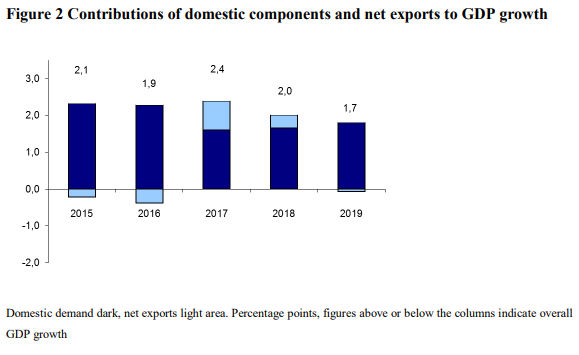

“In the first half of the current year the euro area economy expanded at a markedly slower rate than in 2017, about 0.4% per quarter, but still substantial. Rising risk premia on Italian assets will probably force banks in this large country to tighten credit conditions, and a slowing world trade will dent export growth. All in all, we expect GDP growth in the euro area to go down from 2.4% in 2017 to 2.0% in 2018 and to 1.7% in 2019.”

“Employment continues to expand and vacancy rates are at present higher than in 2017. As a consequence, wages rise more quickly: nominal compensations per employee started accelerating early in 2017, and negotiated wages followed at the beginning of 2018. Wage inflation of slightly below 2.5% and healthy growth in employment raise real labor incomes markedly.

Our forecasts are based on the assumption that rating agencies will continue as-signing investment grade to the Italian government debt, and that the Italian government and the European Commission will find a compromise about the draft budget of the country in the coming weeks. Another assumption is that the UK will not exit the EU in an unorderly way in March 2019”

From the Economic Outlook for the Euro Area in 2018 and 2019:

“Signs of a slowing world economy are piling up: Since the beginning of the year purchasing manager indices have been declining globally, in summer higher US interest rates led investors to withdraw capital from emerging markets, and as a consequence, capital costs rose and currencies depreciated in many emerging markets economies. In October stock prices decreased markedly worldwide including the US,

Posted by at 5:32 PM

Labels: Forecasting Forum

Assessing Housing Risk

From Money and Banking:

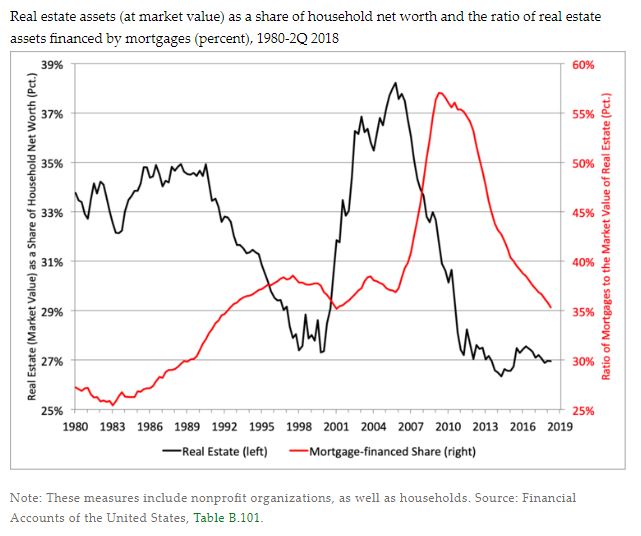

“Housing debt typically is on the short list of key sources of risk in modern financial systems and economies. The reasons are simple: there is plenty of it; it often sits on the balance sheets of leveraged intermediaries, creating a large common exposure; as collateralized debt, its value is sensitive to the fluctuations of housing prices (which are volatile and correlated with the business cycle), resulting in a large undiversifiable risk; and, changes in housing leverage (based on market value) influence the economy through their impact on both household spending and the financial system (see, for example, Mian and Sufi).

In this post, we discuss ways to assess housing risk—that is, the risk that house price declines could result (as they did in the financial crisis) in negative equity for many homeowners. Absent an income shock—say, from illness or job loss—negative equity need not lead to delinquency (let alone default), but it sharply raises that likelihood at the same time that it can depress spending. As it turns out, housing leverage by itself is not a terribly useful leading indicator: it can appear low merely because housing prices are unsustainably high, or high because housing prices are temporarily low. That alone provides a powerful argument for regular stress-testing of housing leverage. And, because housing markets tend to be highly localized—with substantial geographic differences in both the level and the volatility of prices—it is essential that testing be at the local level.”

Continue reading here.

From Money and Banking:

“Housing debt typically is on the short list of key sources of risk in modern financial systems and economies. The reasons are simple: there is plenty of it; it often sits on the balance sheets of leveraged intermediaries, creating a large common exposure; as collateralized debt, its value is sensitive to the fluctuations of housing prices (which are volatile and correlated with the business cycle),

Posted by at 8:19 AM

Labels: Global Housing Watch

Common factors of commodity prices

From ECB’s Research Bulletin:

“Looking at the co-movement in a broad group of commodity prices is key to identifying the nature of commodity price fluctuations. In conclusion, this Research Bulletin article highlights a very simple strategy that central bankers can use to understand the drivers behind commodity price fluctuations. If commodity prices in all markets tend to move in the same direction and by a similar magnitude, then the global demand for commodities is largely responsible for those movements. If commodity price variations are instead localised to a few markets and/or there are important changes in relative prices, then other specific factors related to supply and demand in individual markets are likely to be at play.”

From ECB’s Research Bulletin:

“Looking at the co-movement in a broad group of commodity prices is key to identifying the nature of commodity price fluctuations. In conclusion, this Research Bulletin article highlights a very simple strategy that central bankers can use to understand the drivers behind commodity price fluctuations. If commodity prices in all markets tend to move in the same direction and by a similar magnitude, then the global demand for commodities is largely responsible for those movements.

Posted by at 8:14 AM

Labels: Energy & Climate Change

Wednesday, October 17, 2018

The economics of artificial intelligence: Implications for the future of work

From a new ILO working paper:

“The current wave of technological change based on advancements in artificial intelligence (AI) has created widespread fear of job losses and further rises in inequality. This paper discusses the rationale for these fears, highlighting the specific nature of AI and comparing previous waves of automation and robotization with the current advancements made possible by a wide-spread adoption of AI. It argues that large opportunities in terms of increases in productivity can ensue, including for developing countries, given the vastly reduced costs of capital that some applications have demonstrated and the potential for productivity increases, especially among the low-skilled. At the same time, risks in the form of further increases in inequality need to be addressed if the benefits from AI-based technological progress are to be broadly shared. For this, skills policy are necessary but not sufficient. In addition, new forms of regulating the digital economy are called for that prevent further rises in market concentration, ensure proper data protection and privacy and help share the benefits of productivity growth through a combination of profit sharing, (digital) capital taxation and a reduction in working time. The paper calls for a moderately optimistic outlook on the opportunities and risks from artificial intelligence, provided policy-makers and social partners take the particular characteristics of these new technologies into account.”

From a new ILO working paper:

“The current wave of technological change based on advancements in artificial intelligence (AI) has created widespread fear of job losses and further rises in inequality. This paper discusses the rationale for these fears, highlighting the specific nature of AI and comparing previous waves of automation and robotization with the current advancements made possible by a wide-spread adoption of AI. It argues that large opportunities in terms of increases in productivity can ensue,

Posted by at 3:21 PM

Labels: Inclusive Growth

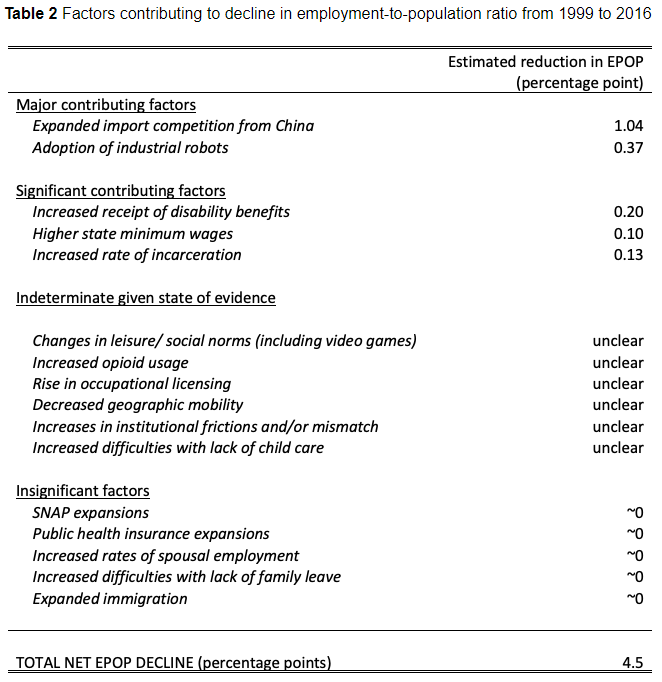

The secular decline in US employment over the past two decades

A new VOX post “reviews the evidence on the main causes of the secular decline in employment since the turn of the century. Labour demand factors – notably import competition from China and the rise of industrial robots – emerge as the key drivers. Some labour supply and institutional factors also have contributed to the decline, but to a lesser extent.”

“Among the effects for which we were able to construct an estimate, increased import competition from China is the single largest contributing factor to the decline in employment. A great deal of empirical evidence links import competition from China to the decline in manufacturing employment. These import pressures also had negative employment effects on ‘upstream’ intermediate goods industries, as well as other non-manufacturing industries (Acemoglu et al. 2016, Autor et al. 2015). Estimates from Acemoglu et al. (2016) are the basis for our estimate that the 302% increase in Chinese imports (measured in 2007 US dollars) from 1999 to 2016 led to displacement of approximately 2.65 million workers, a 1.04 percentage point shift in the employment-population ratio.”

“The employment effects from industrial robots are most clearly documented by Acemoglu and Restrepo (2017), who find that each additional robot per thousand workers between 1993 and 2007 reduced employment by 5.6 workers. This estimate implies that the rise in the stock of robots between 2007 and 2016 displaced 0.95 million workers, equivalent to a 0.37 percentage point decline in the employment-to-population ratio.Although improvements in computing technology have been if anything even more ubiquitous, Autor et al. (2015) find that competition from computing technology affects only routine task-intensive occupations, and that any employment losses in those occupations were offset by employment gains in abstract and manual task-intensive occupations.”

Labour supply factors as a group have been considerably less important than labour demand factors in driving the decline in employment.The claim that expanded safety net support through SNAP (food stamps) or Medicaid led to sizable decreases in employment is hard to square with either the institutional features of these programmes or the evidence on causal linkages. Careful work finds little to no labour supply effects of these programmes, and as a practical matter, they offer very little by way of income support to able-bodied childless adults (see, for example, Hoynes and Schanzenbach 2016 on SNAP, and Leung and Mas 2016 on Medicaid.)

That said, the availability of lifelong disability insurance benefits through the Social Security Disability Insurance (SSDI) programme and the Veterans Affairs Disability Compensation (VADC) programme has contributed modestly to falling employment rates. Applying age-group specific causal labour supply estimates from Maestes et al. (2013) to the growth in the SSDI caseload over and above that due to the population becoming older yields an estimated 0.14 percentage point decline in the e/pop ratio over our time period owing to growth in this programme. Applying the labour supply elasticity from a recent study of an exogenous policy change to VADC program eligibility (Autor et al. 2016) to an estimate of the excess VADC caseload implies that programme’s growth led to an e/pop decline of perhaps 0.06 percentage points.

One might expect the tremendous rise in incarceration in the US to have been a significant driver of declining employment, but because so many incarcerated individuals had low levels of labour force attachment even before their prison term, we estimate only a modest aggregate effect. Applying the causal estimates from Mueller-Smith (2015) to rough estimates of the number of former prisoners by length of time served and prior earnings history, our very rough estimate is that perhaps 0.13 percentage points of the decline in e/pop between 1999 and 2016 can be attributed to policy-induced increases in incarceration. Minimum wage increases probably also had a small but non-negligible impact, especially among younger, less-skilled workers. Taking account of the range of estimates produced by credible study designs, we estimate that increases in state and local minimum wages might have contributed 0.10 percentage points to the e/pop decline.

Other plausible factors driving the decline in employment are the sharp rise in occupational licensing (Kleiner and Krueger 2013), the decline in geographic mobility (Molloy et al. 2011), and increased difficulties securing affordable, high-quality child care. We do not attempt to assign a magnitude to these factors because we lack sufficient evidence to establish the causal impact of these factors or, in the case of child care, to assess how much the factor itself has changed. Another open question is to what extent anecdotes about worsening mismatch between the skills workers possess and those that employers need are borne out in the data.

Scholars have noted the connection of both increased leisure time (including time playing video games) (Aguiar et al. 2017) and increased opioid use (Krueger 2017, Currie et al. 2018) with non-employment, but whether one is causing the other or vice versa, or they are all manifestations of other societal changes, is not easy to disentangle.”

A new VOX post “reviews the evidence on the main causes of the secular decline in employment since the turn of the century. Labour demand factors – notably import competition from China and the rise of industrial robots – emerge as the key drivers. Some labour supply and institutional factors also have contributed to the decline, but to a lesser extent.”

“Among the effects for which we were able to construct an estimate,

Posted by at 1:14 PM

Labels: Inclusive Growth

Subscribe to: Posts