Thursday, October 18, 2018

Highlights of the Economic Outlook for the Euro Area

From the Economic Outlook for the Euro Area in 2018 and 2019:

“Signs of a slowing world economy are piling up: Since the beginning of the year purchasing manager indices have been declining globally, in summer higher US interest rates led investors to withdraw capital from emerging markets, and as a consequence, capital costs rose and currencies depreciated in many emerging markets economies. In October stock prices decreased markedly worldwide including the US, despite the strong upswing in this country.

As a consequence of the turmoil on financial markets, monetary conditions in many emerging economies are no longer favorable. What ultimately counts for the prospects of the global economy, is, however, the performance of the US, the Euro area, China and Japan. The upswing in the US appears stable enough to continue well into 2019. While at present the rest of the group appears to lose momentum, there is a good chance that production in each of these economies will still expand at rates that are close to their potential growth. Further protectionist rounds are the most important risk to this scenario.”

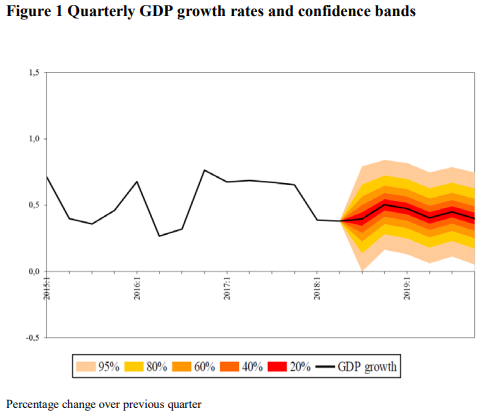

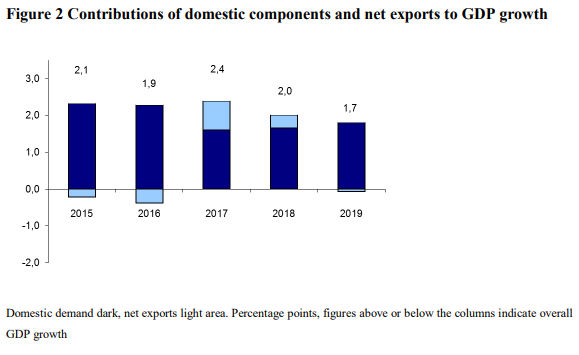

“In the first half of the current year the euro area economy expanded at a markedly slower rate than in 2017, about 0.4% per quarter, but still substantial. Rising risk premia on Italian assets will probably force banks in this large country to tighten credit conditions, and a slowing world trade will dent export growth. All in all, we expect GDP growth in the euro area to go down from 2.4% in 2017 to 2.0% in 2018 and to 1.7% in 2019.”

“Employment continues to expand and vacancy rates are at present higher than in 2017. As a consequence, wages rise more quickly: nominal compensations per employee started accelerating early in 2017, and negotiated wages followed at the beginning of 2018. Wage inflation of slightly below 2.5% and healthy growth in employment raise real labor incomes markedly.

Our forecasts are based on the assumption that rating agencies will continue as-signing investment grade to the Italian government debt, and that the Italian government and the European Commission will find a compromise about the draft budget of the country in the coming weeks. Another assumption is that the UK will not exit the EU in an unorderly way in March 2019”

Posted by at 5:32 PM

Labels: Forecasting Forum

Subscribe to: Posts