Thursday, October 18, 2018

Assessing Housing Risk

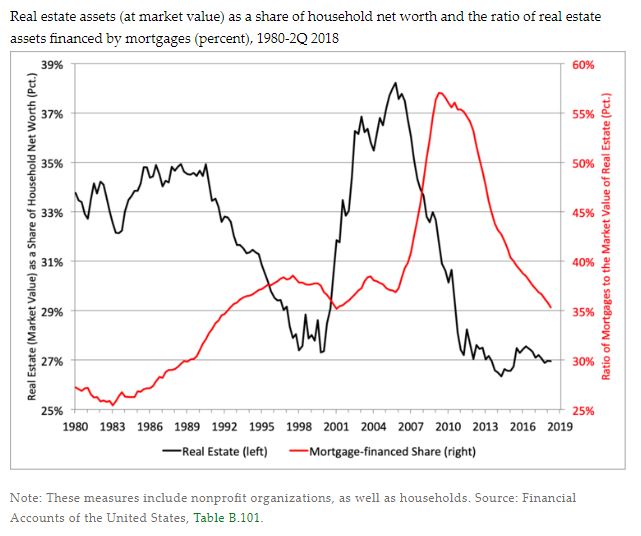

From Money and Banking:

“Housing debt typically is on the short list of key sources of risk in modern financial systems and economies. The reasons are simple: there is plenty of it; it often sits on the balance sheets of leveraged intermediaries, creating a large common exposure; as collateralized debt, its value is sensitive to the fluctuations of housing prices (which are volatile and correlated with the business cycle), resulting in a large undiversifiable risk; and, changes in housing leverage (based on market value) influence the economy through their impact on both household spending and the financial system (see, for example, Mian and Sufi).

In this post, we discuss ways to assess housing risk—that is, the risk that house price declines could result (as they did in the financial crisis) in negative equity for many homeowners. Absent an income shock—say, from illness or job loss—negative equity need not lead to delinquency (let alone default), but it sharply raises that likelihood at the same time that it can depress spending. As it turns out, housing leverage by itself is not a terribly useful leading indicator: it can appear low merely because housing prices are unsustainably high, or high because housing prices are temporarily low. That alone provides a powerful argument for regular stress-testing of housing leverage. And, because housing markets tend to be highly localized—with substantial geographic differences in both the level and the volatility of prices—it is essential that testing be at the local level.”

Continue reading here.

Posted by at 8:19 AM

Labels: Global Housing Watch

Subscribe to: Posts