Tuesday, October 30, 2018

Remembering Albert Hirschman’s Tunnel Effect

From a new post by Timothy Taylor:

“Writing back in 1973, Hirschman offers examples of “development disasters,” in which those stuck in the left lane have come to strongly suspect that economic development will not benefit them, and thus a high degree of social unrest emerges. and he cites Nigeria, Pakistan, Brazil and Mexico as facing these issues in various ways.

I find myself thinking about the tunnel effect and expectations about future social mobility in the current context of the United States. Rising economic inequality in the United States goes back to the 1970s, and the single biggest jump in inequality at the very top of the income distribution happened in the 1990s when stock options and executive compensation took off. But my unscientific sense is that at that time, during the dot-com boom of the 1990s, many people who were either pleased, or not that unhappy, with the rise in inequality of that time. There seemed to be new economic opportunities opening up, new businesses were starting, unemployment rates were low, cool new products and services were becoming available. Even if you were for the time stuck in the left lane, all that movement in the right lane seemed to offer opportunities.

But that optimistic view of high and rising inequality came apart in the 2000s, under pressure from a from a number of factors: the sharp rise in imports from China in the early 2000s that hit a number of local areas so hard; the rise of the opioid epidemic, with its dramatically rising death toll exceeding 40,000 in 2016; and the carnage in employment and housing markets in the aftermath of the Great Recession. In Hirschman’s words, it seems to me that many politicians were “lulled into complacency by the easy early stage when everybody seems to be enjoying the very process that will later be vehemently denounced and damned as one consisting essentially in `the rich becoming richer.'”

Of course, no country is really one big tunnel. When people look at high or rising inequality, their views will often depend on the extent to which they feel some commonality–Hirschman calls it “shared historical experience”–with those who are moving ahead more briskly. In turn, this feeling may depend on the extent to which those who are moving ahead more briskly segment themselves off as a special and separate guild, with an implicit claim that they are just more worthy, or the extent to which they act in ways that embody broader and more inclusive outcomes.”

From a new post by Timothy Taylor:

“Writing back in 1973, Hirschman offers examples of “development disasters,” in which those stuck in the left lane have come to strongly suspect that economic development will not benefit them, and thus a high degree of social unrest emerges. and he cites Nigeria, Pakistan, Brazil and Mexico as facing these issues in various ways.

I find myself thinking about the tunnel effect and expectations about future social mobility in the current context of the United States.

Posted by at 10:16 AM

Labels: Inclusive Growth

Monday, October 29, 2018

Older Americans would work longer if jobs were flexible

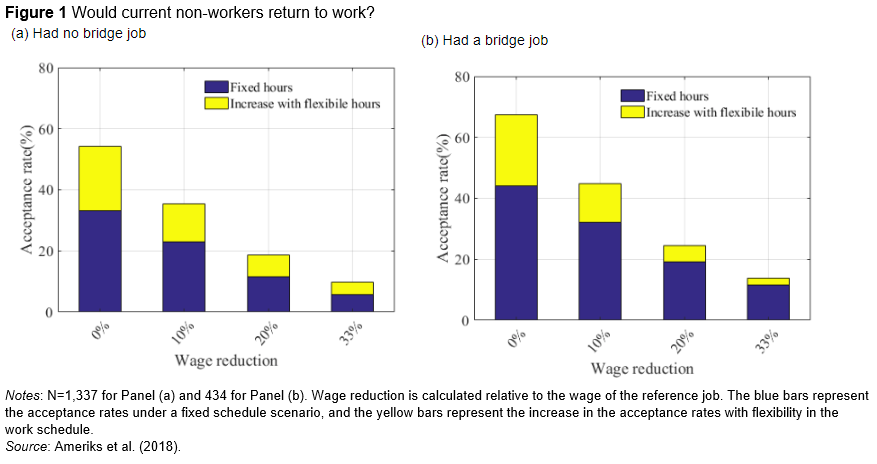

From a new VOX post:

“As countries such as the US face increasingly ageing populations, policymakers face the question of whether to encourage workers to work beyond historical retirement age. Using strategic survey questions, this column gauges whether older Americans stop working due to their lack of interest in working longer or due to lack of opportunity, and finds that it may be the latter. The revealed strong willingness to work implies that job opportunities with flexible schedules are hard for older Americans to find. ”

“The survey responses reveal a strong willingness to work among older Americans who are currently not working. Even when the hypothetical job opportunity requires them to work exactly the same number of hours as in their previously-held reference job, about 40% of the VRI sample that are current not working report that they would accept the offer (Figure 1, blue bars). The acceptance rate is slightly higher for those who had a bridge job after leaving the career job.4 Some of them are even willing to accept a significant wage reduction to go back to work. More than 20% of non-workers are willing to take a 10% reduction in wages and more than 10% are willing to take 20% reduction in wages.”

“Motivated by the recent evidence that part-time options are relatively more common among post-career bridge jobs (Maestas 2010, Rupert and Zanella 2015, and Ramnath et al. 2017), the strategic survey questions also included a scenario where the job opportunity allows respondents to choose the number of hours worked. The survey responses reveal strong preferences for a flexible work schedule among older Americans. The acceptance rate for the hypothetical job opportunity is substantially higher under a flexible work schedule than a fixed work schedule (yellow bars in Figure 1 indicate the increases in the acceptance rate in the flexible schedule compared to the fixed schedule). Perhaps the most striking finding, more than half of the current non-workers would be willing to work again if they could choose the number of hours worked and earned the same hourly wage as in their most recent job. About 40% of them would be willing to take a 10% reduction in hourly wage, and about 20% would be willing to take a 20% reduction in hourly wage, to work under a flexible schedule if other conditions were similar to their most recent job. “

From a new VOX post:

“As countries such as the US face increasingly ageing populations, policymakers face the question of whether to encourage workers to work beyond historical retirement age. Using strategic survey questions, this column gauges whether older Americans stop working due to their lack of interest in working longer or due to lack of opportunity, and finds that it may be the latter. The revealed strong willingness to work implies that job opportunities with flexible schedules are hard for older Americans to find.

Posted by at 5:48 PM

Labels: Inclusive Growth

Expansions Don’t Die of Old Age

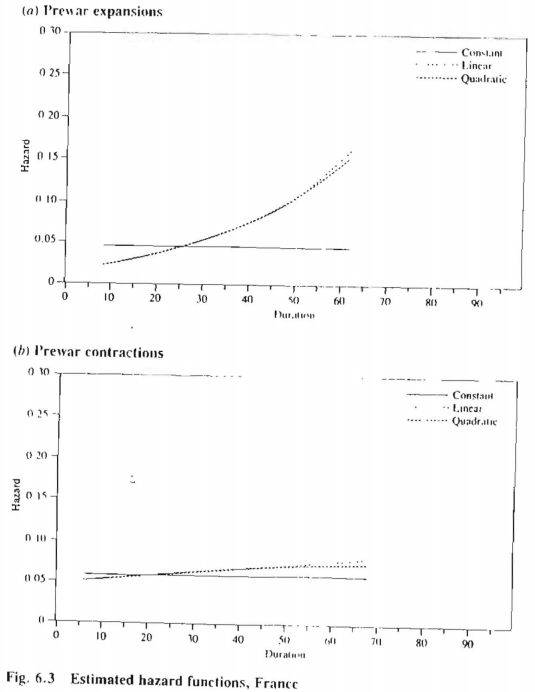

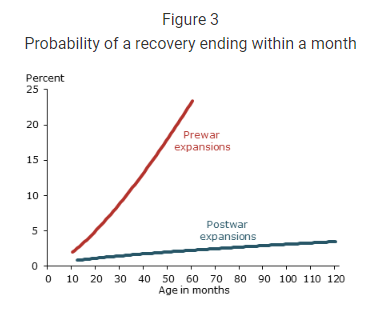

From a new post by Francis Diebold:

“As the expansion ages, there’s progressively more discussion of whether its advanced age makes it more likely to end. The answer is no. More formally, postwar U.S. expansion hazards are basically flat, in contrast to contraction hazards, which are sharply increasing. Of course the present expansion will eventually end, and it may even end soon, but its age it unrelated to its probability of ending.

All of this is very clear in Diebold, Rudebusch and Sichel (1992). See Figure 6.2 on p. 271. (Sorry for the poor photocopy quality.) ”

“The flat expansion hazard result has held up well (e.g., Rudebusch (2016)), and moreover it would only be strengthened by the current long expansion.”

From a new post by Francis Diebold:

“As the expansion ages, there’s progressively more discussion of whether its advanced age makes it more likely to end. The answer is no. More formally, postwar U.S. expansion hazards are basically flat, in contrast to contraction hazards, which are sharply increasing. Of course the present expansion will eventually end, and it may even end soon, but its age it unrelated to its probability of ending.

Posted by at 9:49 AM

Labels: Macro Demystified

Saturday, October 27, 2018

Timothy Taylor on Rent Control Returns

A new post by Timothy Taylor shares some thoughts on rent control returns:

“1) Rent control is typically justified by pointing to low-income people who have difficulty paying the market rents. I’m sympathetic to this groups, and favor various policies like income support and rent vouchers to help them. But as I have argued in other contexts, invoking poverty and necessity as the basis for rent control is a ruse. The poor are not helped in any direct way by controlling rental prices for all income groups, including the rich and the the middle-class.

One response I have heard to this argument is that if rent control only applied to those with low-incomes, there would be an incentive to avoid renting to those with low incomes and not to build any more low-income housing. Of course, this argument is of course an admission that rent control discourages the growth and maintenance of rental properties. Expanding rent control to cover all income groups will expand those negative incentives to the entire rental housing stock, rather than just part of it.

2) Many of those who favor rent control also favor higher minimum wages. Thus, it is useful to remember that rent control is fundamentally different from minimum wage rules, because prices for physical objects like buildings are fundamentally different from wages paid to workers. When the price of an hour of work changes, workers can have higher or lower incentives, or higher or lower morale, or can search more or less for jobs, or consider different kinds of jobs, or look for jobs in other jurisdictions or in the underground economy, or even withdraw from the labor market. Buildings are not flexible in these ways, and so the implications of rent control are easier to predict with confidence than the implications of minimum wage laws.

3) Before you own a house, there can be a tendency (which I certainly had) to think of the housing stock as immutable, rather like the pyramids. When you own a house, you instead come to think of it as a large machine that requires continual maintenance on all its separate parts. Many arguments in favor of rent control implicitly view the housing stock like the pyramids, and underestimate both the short-run costs of maintenance and repair and the longer-run costs of property upgrades and new construction.

4) Rent control offers a tradeoff between present benefits for one group and future costs for another. The present benefits go to those already living in apartments that are rent-controlled–whether they are low-income or not. Rent control benefits the well-settled. The future costs are imposed on those who are unable to find a place. In addition, rent control discourages building additional rental housing, which means that the possibility of mutual gains for future builders and future renters are foreclosed.

5) In any local housing market, the price of owned housing and rental housing is going to be closely linked, because one can be converted with relative ease into the other. If the price of housing is high, the price of rentals is also going to be high. The notion that a local housing market can make all the existing homeowners happy, with high and rising resale prices, but also make all the renters happy, with low and stable rents, is a delusion.

With rent control, as with so many other subjects, it can be tricky to sort out cause and effect. For example, say that we observe that cities which have rent control are more likely to have high housing prices. This of course would not prove whether rent control leads to high housing prices, or high housing prices make rent control more likely to be enacted, or whether some additional factors are influencing both housing prices and the political prospects for rent control. Thus, researchers often try to seek out a “natural experiment,” meaning a situation in which some change in law or circumstance affects part of a market at a certain time and place, but not another part. Then one can compare the more-affected and less-affected parts of the market.”

A new post by Timothy Taylor shares some thoughts on rent control returns:

“1) Rent control is typically justified by pointing to low-income people who have difficulty paying the market rents. I’m sympathetic to this groups, and favor various policies like income support and rent vouchers to help them. But as I have argued in other contexts, invoking poverty and necessity as the basis for rent control is a ruse. The poor are not helped in any direct way by controlling rental prices for all income groups,

Posted by at 11:00 AM

Labels: Macro Demystified

Friday, October 26, 2018

Housing View – October 26, 2018

On cross-country:

- Housing expenditures and income inequality: Shifts in housing costs exacerbated the rise in income inequality – VOX

- Cost of greener homes too high, Europe tells ING survey – ING

- Report on UN Special Rapporteur on the Right to Housing – National Economics & Social Rights Initiative

On the US:

- What does economic evidence tell us about the effects of rent control? – Brookings

- Star Tribune Op-Ed: Affordable housing crisis demands more supply – Federal Reserve Bank of Minneapolis

- Computer Vision and Real Estate: Do Looks Matter and Do Incentives Determine Looks – NBER

- New Book Asks: What It Would Take to Foster Communities of Inclusion in an Era of Inequality? – Harvard Joint Center for Housing Studies

- California has a housing crisis, and Californians seem confused about how to solve it – American Enterprise Institute

- Home Sales Are Dropping — Could The Housing Market Finally Be Cooling Off? – NPR

- Tax practices that amplify racial inequities: Property tax treatment of owner-occupied housing – D.C. Policy Center

On other countries:

- [Brazil] Brazil’s home buyers bet on the ballot – Financial Times

- [Germany] Germany’s housing crisis fuels black market for refugees – Reuters

- [Ireland] Is Dublin’s property market heading for a soft landing? – Financial Times

- [New Zealand] Ban on foreign buyers seen poor answer to New Zealand’s housing shortage – Reuters

- [Spain] Spanish banks hit by supreme court ruling on mortgage fees – Financial Times

Photo by Aliis Sinisalu

On cross-country:

- Housing expenditures and income inequality: Shifts in housing costs exacerbated the rise in income inequality – VOX

- Cost of greener homes too high, Europe tells ING survey – ING

- Report on UN Special Rapporteur on the Right to Housing – National Economics & Social Rights Initiative

On the US:

- What does economic evidence tell us about the effects of rent control?

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts