Tuesday, August 2, 2016

Labor Mobility in the United States

The United States has always been regarded as a highly mobile society. Previous work has left the impression that when adverse economic shocks hit their cities or regions, Americans are quickly able to move and find jobs elsewhere within the country. In a new paper, Mai Dao, Davide Furceri and I provide new evidence that questions this view. Our evidence shows that the ability to migrate is not as immediate as previously supposed; in the first year or two after an adverse shock to a state, the bulk of the burden is borne by an increase in the state unemployment and a decline in its labor force participation rate. We also find that while net mobility across states picks up during national recessions, this increase is driven more by a stronger population inflow into states that are doing better rather than stronger population outflow from states that are doing worse; the outflow occurs only toward the end of the recession. Overall, therefore, our results offer a less sanguine view of the ability of U.S. workers to shield themselves from the consequences of adverse shocks than is available in the literature. Here is a link to the paper and to an online appendix which is a wonk’s delight.

The United States has always been regarded as a highly mobile society. Previous work has left the impression that when adverse economic shocks hit their cities or regions, Americans are quickly able to move and find jobs elsewhere within the country. In a new paper, Mai Dao, Davide Furceri and I provide new evidence that questions this view. Our evidence shows that the ability to migrate is not as immediate as previously supposed; in the first year or two after an adverse shock to a state,

Posted by at 4:40 PM

Labels: Inclusive Growth

Okun’s Law: Fit at 55?

In a revised version of our 2013 paper, Larry Ball, Daniel Leigh and I still conclude: “It is rare to call a macroeconomic relationship a “law.” Yet we believe that Okun’s Law has earned its name. It is not as universal as the law of gravity (which has the same parameters in all advanced economies), but it is strong and stable by the standards of macroeconomics. Reports of deviations from the Law are often exaggerated. Okun’s Law is certainly more reliable than a typical macro relationship like the Phillips curve, which is constantly under repair as new anomalies arise in the data.” The paper provides estimates of Okun’s Law for 20 advanced economies, including the United States.

In a revised version of our 2013 paper, Larry Ball, Daniel Leigh and I still conclude: “It is rare to call a macroeconomic relationship a “law.” Yet we believe that Okun’s Law has earned its name. It is not as universal as the law of gravity (which has the same parameters in all advanced economies), but it is strong and stable by the standards of macroeconomics. Reports of deviations from the Law are often exaggerated.

Posted by at 4:13 PM

Labels: Inclusive Growth

Monday, August 1, 2016

Real Estate Market in Ireland

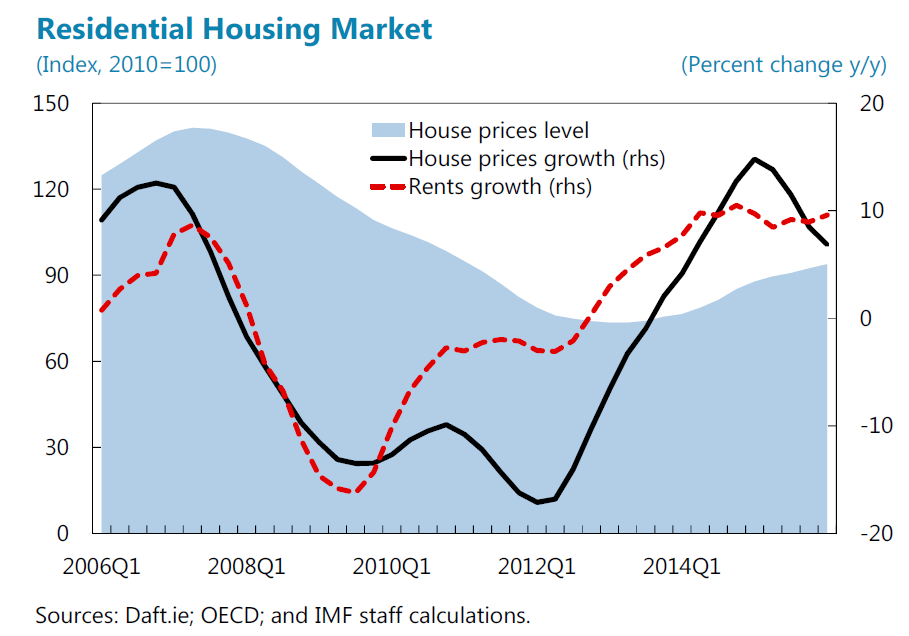

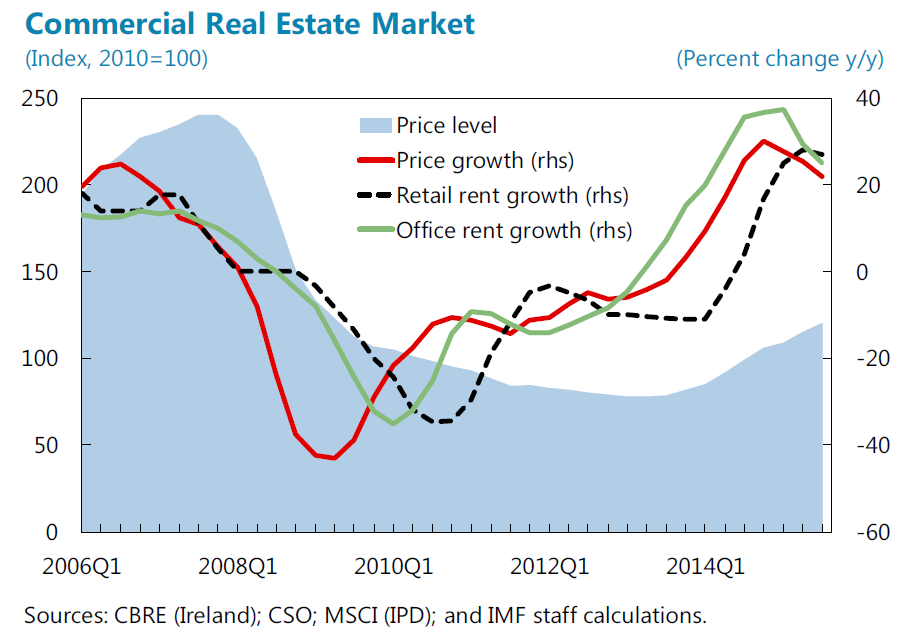

“Residential real estate (RRE) prices and rents continued to increase. Nevertheless, following the abolishment of tax exemptions on capital gains in December 2014 and the introduction of new macroprudential loan-to-value (LTV) and loan-to-income (LTI) limits in February 2015 (…), the market somewhat cooled off: RRE price growth decelerated in late 2015 and the number of mortgage approvals temporarily declined (…). [Meanwhile,] Commercial real estate (CRE) prices rose even more rapidly. Total returns of the Irish CRE sector outstripped those of other European countries, reflecting the confluence of strong equity investment largely financed by foreigners in search for high yield, and still limited new construction”, says IMF’s report on Ireland.

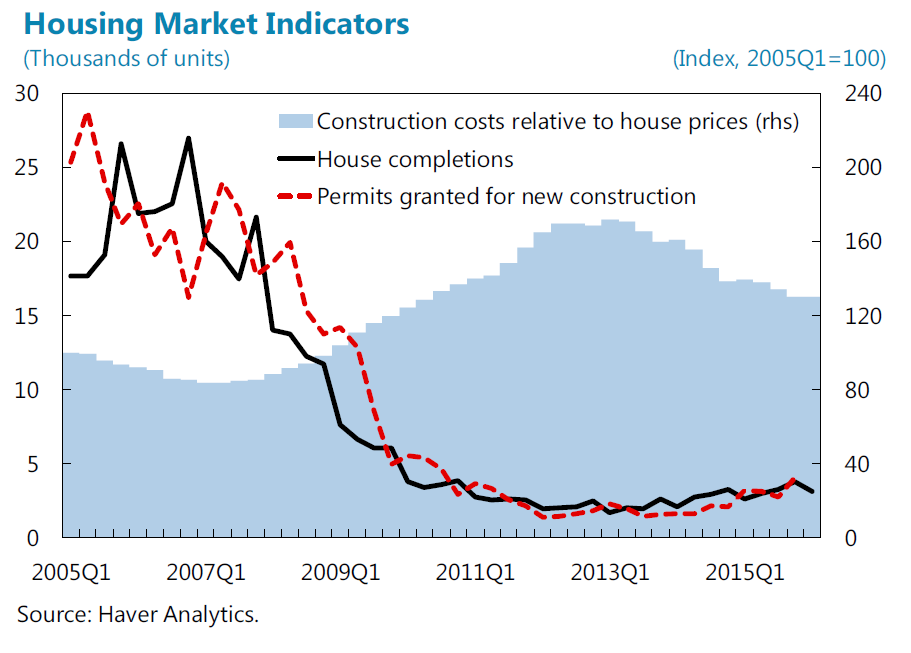

On housing supply, the report says that “Boosting the housing supply would help mitigate property price and rent pressures. The sluggish construction activity in recent years reflects the sector’s downsizing after the bursting of the property market bubble in 2008-09 and the ensuing limited access to finance for companies. High construction costs due to strict planning requirements have also been a factor. In response to mounting pressures in the housing market, the government introduced a package of measures in November 2015, including rebates for housing construction schemes that meet certain criteria, and new planning guidelines, which seek to reduce the building costs.16 Additionally, the National Asset Management Agency (NAMA), within its mandate, is to fund the delivery of 20,000 residential units by 2020. Staff stressed that additional policy actions should help expedite new construction, and welcomed the authorities’ intent to publish an Action Plan for Housing over the summer.”

There is also a separate report on commercial real estate.

“Residential real estate (RRE) prices and rents continued to increase. Nevertheless, following the abolishment of tax exemptions on capital gains in December 2014 and the introduction of new macroprudential loan-to-value (LTV) and loan-to-income (LTI) limits in February 2015 (…), the market somewhat cooled off: RRE price growth decelerated in late 2015 and the number of mortgage approvals temporarily declined (…). [Meanwhile,] Commercial real estate (CRE) prices rose even more rapidly. Total returns of the Irish CRE sector outstripped those of other European countries,

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, July 28, 2016

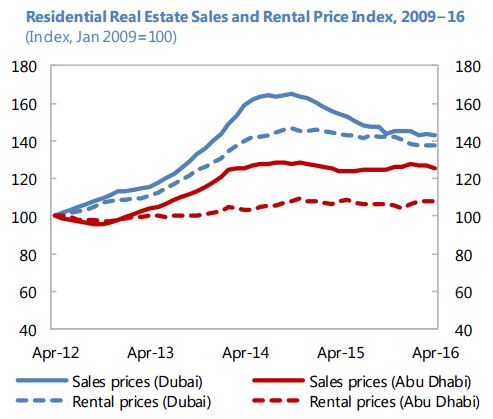

Housing Market in United Arab Emirates

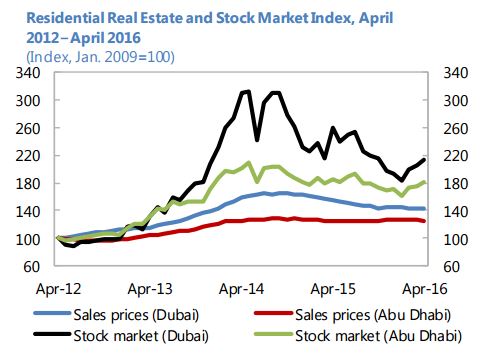

“Real estate prices have continued to decline, but the quality of the real estate loan portfolio has remained resilient. Structural measures taken in 2014, such as the tightening of industry self-regulation, higher real estate fees, and tighter macroprudential regulation for mortgage lending, have helped contain speculative demand for real estate and led to declining prices. This trend has continued with Dubai’s real estate average residential prices falling by 11 percent in 2015, also reflecting oversupply and strong headwinds on demand. In Abu Dhabi where the supply growth slowed, they fell by 0.8 percent. However, these developments do not appear to pose systemic risks for the financial sector, as the nonperforming loans for construction and real estate development declined from 12.3 percent in 2013 to 7.5 percent by end-March 2016. Similar improvements have been experienced for loans to households with NPLs ratio down from 10 to 4.9 percent over the same period”, according to the IMF’s report on United Arab Emirates.

“Real estate prices have continued to decline, but the quality of the real estate loan portfolio has remained resilient. Structural measures taken in 2014, such as the tightening of industry self-regulation, higher real estate fees, and tighter macroprudential regulation for mortgage lending, have helped contain speculative demand for real estate and led to declining prices. This trend has continued with Dubai’s real estate average residential prices falling by 11 percent in 2015, also reflecting oversupply and strong headwinds on demand.

Posted by at 5:00 AM

Labels: Global Housing Watch

Tuesday, July 26, 2016

Issi Romem on BuildZoom and the U.S. Housing Market

From Global Housing Watch Newsletter: July 2016

Issi Romem is the Chief Economist at BuildZoom—a start-up in San Francisco. For this issue of the Global Housing Watch newsletter, he talked to Hites Ahir about BuildZoom and what it offers, whether the expansion of American cities has slowed down, and what BuildZoom’s data tell us about the current state and the short term outlook for the U.S. housing market.

Hites Ahir: Tell us a bit about your background and what sparked your interest in housing markets.

Issi Romem: In pursuit of my life long passion for observing and understanding cities, I earned a PhD in economics at the University of California at Berkeley. Economics offers a particular lens with which to analyze cities and contains several fields that relate to them. I chose to focus on labor and housing markets. As the Chief Economist at BuildZoom, I leverage my role to continue studying cities in alignment with the company’s needs.

Hites Ahir: Tell us about BuildZoom and your role in the company?

Issi Romem: BuildZoom actively helps people find good, reliable and communicative contractors, and helps see the projects through to completion. In order to inform the matching of people and contractors, BuildZoom collects data on contractor licensing as well as a growing national repository of building permit data. BuildZoom makes the data easy and free for the public to view on the web, which is particularly valuable because – unlike customer recommendations or photos – a paper trail of building permits shows a contractor’s professional experience in a way that cannot be falsified.

My role at BuildZoom includes the production of data-driven content for the website, as well as oversight of data science and the company’s data collection efforts. The data-driven content includes the production of economic indices of remodeling and new construction activity, as well as one-off economic analyses. It also includes trawling new building permits for newsworthy information, such as projects undertaken by companies that are particularly interesting to the public.

Hites Ahir: In the United States, there are a lot of companies that provide data and analysis on the U.S. housing market. So what is unique about BuildZoom?

Issi Romem: BuildZoom’s data sheds light on all types of new construction and remodeling activity. Remodeling, in particular, is an otherwise hidden aspect of the nation’s real estate stock, on which there are very few sources of information. Moreover, as some of the greatest metro areas in the nation restrict their supply of new housing, more and more of the action in these cities’ real estate markets involves the renovation and/or repurposing of the existing stock of structures, into which BuildZoom’s data sheds light.

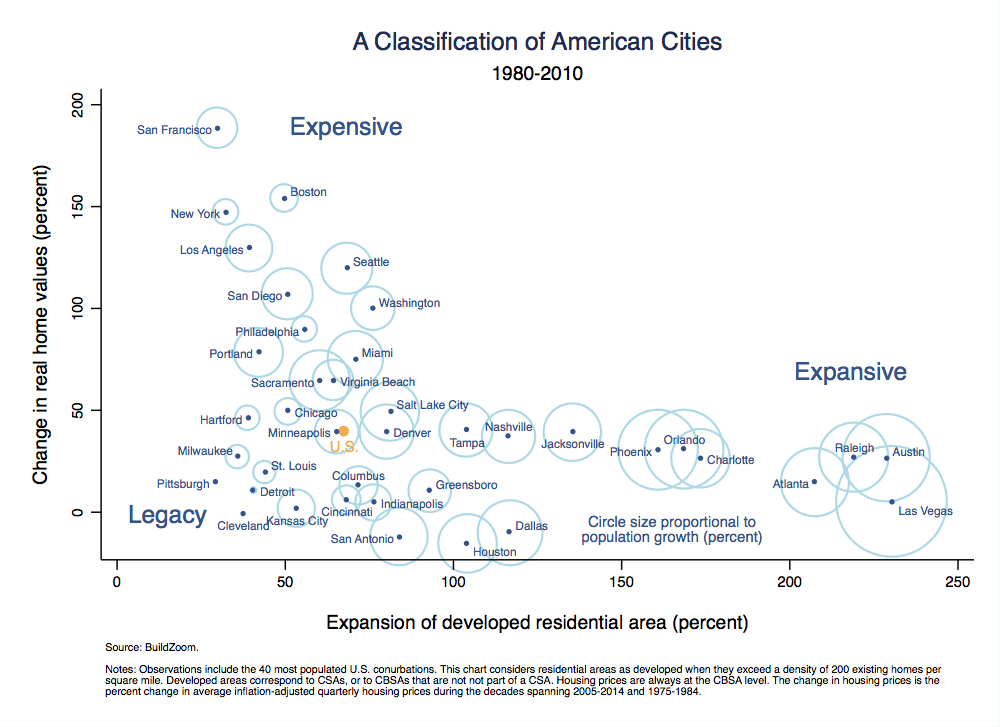

Hites Ahir: You recently wrote on whether the expansion of American cities has slowed down. What is the verdict?

Issi Romem: The expansion of American Cities as a whole has not slowed down. It has kept progressing at a more or less steady pace each decade since World War II. However, there are important differences between cities. One group of cities, consisting mostly of large coastal cities, have indeed slowed down their expansion, and in so doing have channeled their economic strength away from population growth and into housing price growth. I refer to these as expensive cities. Another group of cities, mostly in the south, have continued to expand with gusto, and as a result have experienced tremendous population growth while maintaining housing prices at affordable levels. I refer to these as the expansive cities, with an a. Finally, a third group of cities mostly in the rust belt had thriving economies in the past, but have lost much of their economic base, and experienced neither housing price growth nor population growth. I refer to this last group as legacy cities. See the full report here.

Hites Ahir: Based on BuildZoom’s building permits and remodeling data, what can you tells us about the current state of the U.S. housing market?

Issi Romem: The index tells us that, during the last decade’s boom and bust cycle, residential remodeling peaked and plummeted in sync with residential new construction. However, it also tells us that during the bust, new residential construction suffered much more than residential remodeling, and that residential remodeling is currently much closer to its pre-bust level than new construction. During downturns, new construction essentially grinds to a halt, but remodeling combines procyclical elements, like renovations preceding or following a home sale, with elements that are acyclical, like maintenance. The latter keep fluctuations in remodeling less pronounced than those of new construction.

Hites Ahir: What is your view on the short term outlook for the U.S. housing market?

Issi Romem: Predicting where the housing market is going in the short term is tricky business. I suspect that a downward correction in housing prices is possible, but far from certain, and that if it occurs it will be very minor compared to the previous decade’s bust, and will be concentrated in the expensive coastal cities. If and until such a correction occurs, we are likely to see particularly robust housing price increases in places that receive the greatest influx of homeowners migrating out of the expensive coastal cities. Portland (Oregon), Seattle and Denver, for example, draw particularly large inflows of former residents priced out of California. Such places are also susceptible to experiencing a price correction if the influx of homeowners migrating out of the expensive coastal cities were to ease, following a price correction there.

From Global Housing Watch Newsletter: July 2016

Issi Romem is the Chief Economist at BuildZoom—a start-up in San Francisco. For this issue of the Global Housing Watch newsletter, he talked to Hites Ahir about BuildZoom and what it offers, whether the expansion of American cities has slowed down, and what BuildZoom’s data tell us about the current state and the short term outlook for the U.S.

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts