Monday, December 12, 2016

The IMF is Not Asking Greece for More Austerity

Greece is once again in the headlines as discussions for the second review of its European Stability Mechanism (ESM) program are gaining pace. Unfortunately, the discussions have also spurred some misinformation about the role and the views of the IMF. Above all, the IMF is being criticized for demanding more fiscal austerity, in particular for making this a condition for urgently needed debt relief. This is not true, and clarifications are in order.

The IMF is not demanding more austerity. On the contrary, when the Greek Government agreed with its European partners in the context of the ESM program to push the Greek economy to a primary fiscal surplus of 3.5 percent by 2018, we warned that this would generate a degree of austerity that could prevent the nascent recovery from taking hold. We projected that the measures in the ESM program will deliver a surplus of only 1.5 percent of GDP, and said this would be enough for us to support a program. We did not call for additional measures to achieve a higher surplus. But contrary to our advice, the Greek Government agreed with the European institutions to temporarily compress spending further if needed to ensure that the surplus would reach 3.5 percent of GDP.

We have not changed our view that Greece does not need more austerity at this time. Claiming that it is the IMF who is calling for this turns the truth upside down.

Continue reading here.

Greece is once again in the headlines as discussions for the second review of its European Stability Mechanism (ESM) program are gaining pace. Unfortunately, the discussions have also spurred some misinformation about the role and the views of the IMF. Above all, the IMF is being criticized for demanding more fiscal austerity, in particular for making this a condition for urgently needed debt relief. This is not true,

Posted by at 5:07 PM

Labels: Inclusive Growth

Friday, December 9, 2016

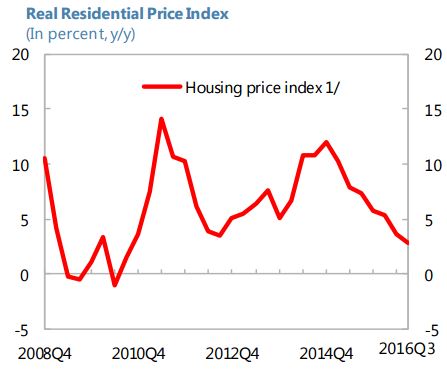

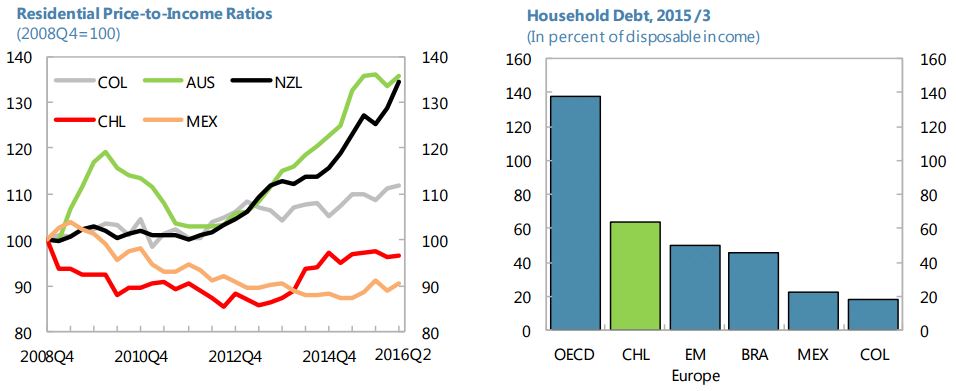

Housing Market in Chile

“Housing prices have grown at a relatively fast pace in Chile, prior to an impending VAT increase in 2016. Residential property sales have fallen sharply since early 2016. Housing prices are cooling down rapidly. Household debt has increased, driven by mortgage loans. Still, the price-to-income ratio has stabilized recently (…) and, the debt-to-income ratio in Chile remains low relative to advanced economies”, according to IMF’s latest report on Chile.

“Housing prices have grown at a relatively fast pace in Chile, prior to an impending VAT increase in 2016. Residential property sales have fallen sharply since early 2016. Housing prices are cooling down rapidly. Household debt has increased, driven by mortgage loans. Still, the price-to-income ratio has stabilized recently (…) and, the debt-to-income ratio in Chile remains low relative to advanced economies”, according to IMF’s latest report on Chile.

Posted by at 3:27 PM

Labels: Global Housing Watch

Thursday, December 8, 2016

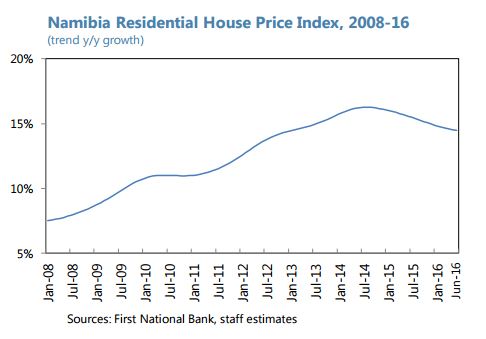

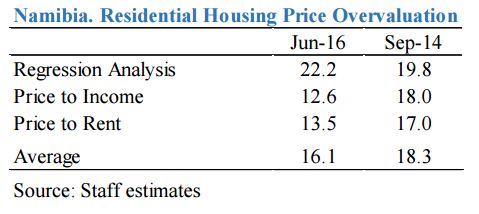

Housing Market in Namibia

“While decelerating, residential real estate prices continue their fast growing trend. (…) On average, house prices remain overvalued, raising risks of possible price corrections. Using common housing ratios and regression analysis from a cross country sample of house price reversal as in the 2015 Article IV staff report, staff estimates that in June 2016 the house price overvaluation at national level was on average around 16 percent, slightly lower than estimated in the 2015 Article IV. The reduction is attributable both to the recent slowdown in price growth and to revisions to the historical values of the housing index. (…) Despite their large exposure to mortgage loans, banks remain resilient to large house price corrections with pressures arising only under tail risk scenarios”, says IMF’s report on Namibia.

“While decelerating, residential real estate prices continue their fast growing trend. (…) On average, house prices remain overvalued, raising risks of possible price corrections. Using common housing ratios and regression analysis from a cross country sample of house price reversal as in the 2015 Article IV staff report, staff estimates that in June 2016 the house price overvaluation at national level was on average around 16 percent,

Posted by at 3:11 PM

Labels: Global Housing Watch

Tuesday, December 6, 2016

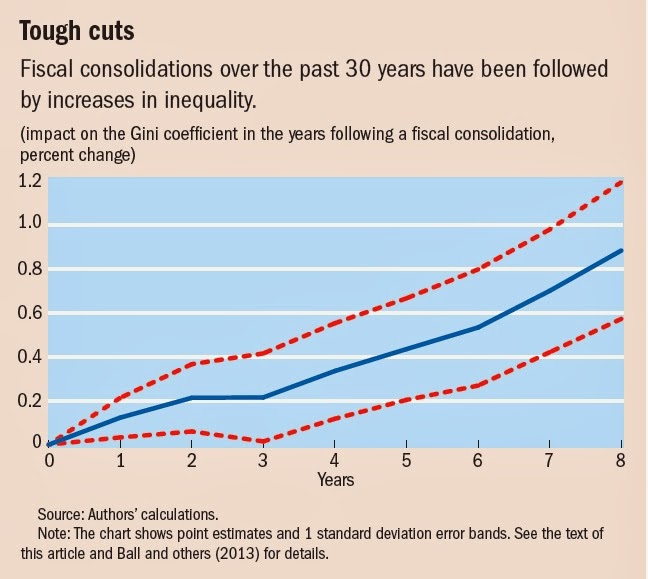

Austerity and Inequality: New Evidence from the IMF

The IMF Economic Review just published a paper that looks into the “distributional consequences of fiscal austerity measures” for 17 OECD countries over the last 30 years. This new paper adds to the stock of IMF papers on the impacts of fiscal consolidation of inequality. Here are links and a cheat sheet to the key papers:

1) Painful Medicine: This (non-wonkish) paper documented that fiscal consolidations not only lower aggregate incomes but have distributional consequences—wage incomes fall more than profits; and the long-term unemployed are affected more than short-term unemployed.

2) The Distributional Effects of Fiscal Consolidation: A wonkish version of the “Painful Medicine” article, with the additional result that, between 1978 and 2009, fiscal consolidations in advanced economies increased the Gini measure on income inequality.

3) Distributional Consequences of Fiscal Consolidation and the Role of Fiscal Policy: In addition to confirming the results in the previous papers, this paper brings in evidence from emerging markets. It also discusses how policies can be designed to mitigate the impacts of fiscal policy on inequality.

4) Who Let the Gini Out?: A (non-wonkish) summary of some of the previous papers.

5) Fiscal Policy and Inequality: A key finding of the paper is that fiscal consolidations during the Great Recession did not lead to increases in inequality.

6) Distributional Consequences of Fiscal Adjustments: What Do the Data Say?: “The paper shows that fiscal adjustments are likely to raise inequality through various channels including their effects on unemployment. Spending-based adjustments tend to worsen inequality more significantly, relative to tax-based adjustments. The composition of austerity measures also matters: progressive taxation and targeted social benefits and subsidies introduced in the context of a broader decline in spending can help offset some of the adverse distributional impact of fiscal adjustments.”

The IMF Economic Review just published a paper that looks into the “distributional consequences of fiscal austerity measures” for 17 OECD countries over the last 30 years. This new paper adds to the stock of IMF papers on the impacts of fiscal consolidation of inequality. Here are links and a cheat sheet to the key papers:

1) Painful Medicine: This (non-wonkish) paper documented that fiscal consolidations not only lower aggregate incomes but have distributional consequences—wage incomes fall more than profits;

Posted by at 10:22 AM

Labels: Inclusive Growth

Sunday, December 4, 2016

European Unemployment: Deja Vu All Over Again?

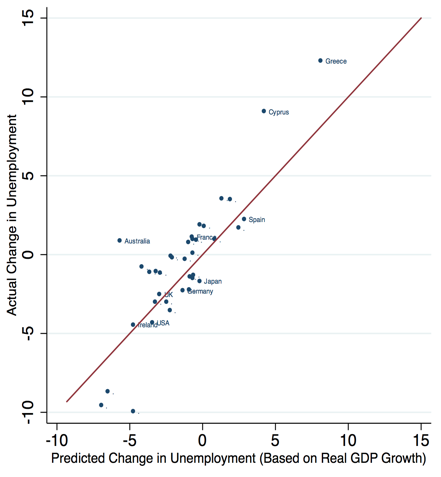

Thirty years ago, a distinguished group of economists advocated a ‘two-handed’ approach to unemployment that targeted supply as much as demand. This column examines recent work on the effectiveness of cyclical and structural policies – the two ‘hands’ – targeting unemployment in Europe. It further considers the pressures from greater integration of capital and labour markets on the success of these reforms. Cyclical measures, particularly the easing of monetary policy, have been successful, but further structural reforms are still needed in many countries where average unemployment remains too high.

Read the rest at Vox.

Figure 1. Actual and predicted changes in unemployment, advanced economies, 2010 to 2015

Notes: The chart compares the actual change in unemployment in each country with what could have been predicted on the basis of the hisotrical relationship between unemployment and output (Okun’s Law).

Thirty years ago, a distinguished group of economists advocated a ‘two-handed’ approach to unemployment that targeted supply as much as demand. This column examines recent work on the effectiveness of cyclical and structural policies – the two ‘hands’ – targeting unemployment in Europe. It further considers the pressures from greater integration of capital and labour markets on the success of these reforms. Cyclical measures, particularly the easing of monetary policy, have been successful, but further structural reforms are still needed in many countries where average unemployment remains too high.

Posted by at 10:45 PM

Labels: Inclusive Growth

Subscribe to: Posts