Monday, August 15, 2016

Workshop on Global Labor Markets

IMF-OCP Policy Center-Brunel University

Workshop on Global Labor Markets

September 1-2, 2016, Paris

![]()

Thursday, September 1

9-9.15 Opening remarks:

Tao Zhang, Deputy Managing Director, IMF

Karim El Aynaoui, Managing Director, OCP Policy Center

Session 1: Does Growth Create Jobs? Global and Regional Evidence

Chair: Prakash Loungani (IMF)

Background paper on Okun’s Law

9.15-10.30 Laurence Ball (Johns Hopkins University)

Does One Law Fit All? Okun’s Law in Advanced & Developing Economies (Draft Paper and Presentation)

Tayeb Ghazi (OCP Policy Center)

Okun’s Law: (Un)fit for Low-Income Countries?

Nathalie Gonzalez-Prieto (IMF)

What Lies Beneath: Okun’s Law in U.S. States (Draft and Presentation)

10.30-10.45 Coffee break

10.45-12 Discussants: Willi Semmler (New School for Social Research)

Ekkehard Ernst (ILO)

Francois Facchini (University of Paris 1)

Mai Dao (IMF)

12-1.30 Lunch

1.30-2 Karim El Aynaoui and Aomar Ibourk (OCP Policy Center)

Policy Lessons from Okun’s Law for Developing Countries

Session 2: Jobs and Growth: The Role of Policies and Institutions

Chair: Jean-Bernard Chatelain (Paris School of Economics)

2-3 Haje Schutte and Karen Wilson (OECD)

The Sustainable Development Goals as Business Opportunities

Aurelio Parisotto (ILO)

Decent Work for All: Parsing Goal 8 of the SDGs

3-3.15 Coffee break

3.15-4 Romain Duval (IMF)

Can Reform Waves Turn the Tide? Some Case Studies Using the Synthetic Control Method

Discussant: Nauro Campos (Brunel University)

4-4.45 Sebastian Weber (ECB)

Reassessing the Role of Labor Market Institutions for the Business Cycle

Discussant: Mai Dao (IMF)

4.45-5.30 Giovanni Melina (IMF)

Sectoral Labor Mobility and Optimal Monetary Policy

Discussant: Manasa Patnam (CREST-ENSAE)

Friday, September 2

Session 3: Labor Flows: Mobility, Migration, Displacement

Chair: Nauro Campos (Brunel University)

9-9.45 Amine Ouazad (Ecole Polytechnique)

Job Displacement and Crime: Evidence from Danish Microdata

Discussant: Ahmed Tritah (Universite du Maine)

9.45-10.45 Alessandro Turrini (European Commission)

Labor Mobility and Labor Market Adjustment in the EU

Anda David (Agence Française de Développement)

Migration and Employment Interactions in a Crisis Context: The Case of Tunisia

10.45-11 Coffee break

11-11.30 Discussants: Davide Furceri (IMF)

Nawal Zaaj (Higher Council of Scientific Research, Morocco)

11.30-12.15 Martin Kahanec (Central European University)

Free Movement of Workers within the EU

12.15-1.30 Lunch

Session 4: Policy Priorities and Prospects for the EU

Chair: Nauro Campos (Brunel University)

1.30-2 Rodolphe Blavy (IMF, Europe Office)

An Overview of Developments and Policy Debates

2-2.30 Francesco Saraceno (OFCE-Sciences Po)

An Assessment of EU Fiscal Policy

2.30-3.15 Panel: Alessandro Turrini (European Commission)

Willi Semmler (New School for Social Research)

3.15-3.30 Coffee break

Session 5: The Design of Labor Market Institutions

Chair: Ahmed Tritah (Universite du Maine)

Active Labor Market Policies

3.30-4.30 Bruno Crepon (ENSAE-CREST)

Active Labor Market Policies: A Review

Veronica Escudero (ILO)

Cross-Country Evidence of Active Labor Market Policies

Minimum Wages, Unemployment Insurance and Employment Protection Legislation

4.30-5.15 Sabina Dewan (JustJobs Network)

Ekkehard Ernst (ILO)

Romain Duval (IMF)

Summing-up

5.15-5.30 Laurence Ball (Johns Hopkins University)

IMF-OCP Policy Center-Brunel University

Workshop on Global Labor Markets

September 1-2, 2016, Paris

![]()

Thursday, September 1

9-9.15 Opening remarks:

Tao Zhang, Deputy Managing Director, IMF

Karim El Aynaoui, Managing Director, OCP Policy Center

Session 1: Does Growth Create Jobs? Global and Regional Evidence

Chair: Prakash Loungani (IMF)

Background paper on Okun’s Law

Posted by at 10:42 AM

Labels: Inclusive Growth

Housing Market in China

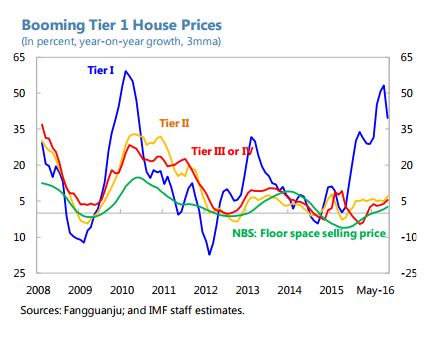

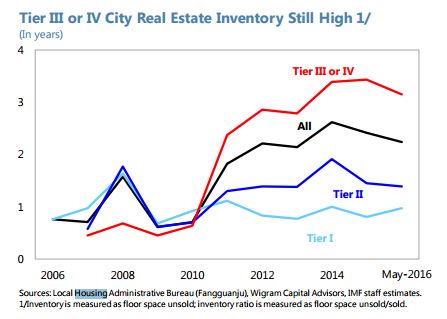

The latest IMF’s annual report on China points out the following:

- “China has recently experienced a sequence of booms in various asset prices—property, equity and bonds. This propensity is a symptom of a large stock of savings searching for yield, rising leverage, and a belief that the web of implicit guarantees will limit losses. This distorts the pricing of risk and facilitates bouts of speculative excess. Most recently, Tier-1 cities such as Shenzhen, Shanghai, and Beijing, are seeing large housing price increases as bank lending for home purchases increased strongly.”

- “Residential investment is reviving again in several parts of the country, even as excess inventory remains high, and region-specific policies could be appropriate. Specifically, tighter macroprudential measures in Tier 1 cities seem warranted (for example reducing loan-to-value ratios on mortgages for second homes). For lower-tier cities, where multi-year excess inventory levels are particularly acute, restricting new starts seems warranted, for example by tightening prudential measures on credit to property developers.”

- “The authorities observed that property prices were beginning to show signs of moderation in Tier 1 cities, while equity prices were more in line with fundamentals after the substantial correction over the last 12 months. They recognized that there were some financial sector risks, but that these were limited and the supervisors were responding proactively.”

The latest IMF’s annual report on China points out the following:

- “China has recently experienced a sequence of booms in various asset prices—property, equity and bonds. This propensity is a symptom of a large stock of savings searching for yield, rising leverage, and a belief that the web of implicit guarantees will limit losses. This distorts the pricing of risk and facilitates bouts of speculative excess. Most recently, Tier-1 cities such as Shenzhen,

Posted by at 10:41 AM

Labels: Global Housing Watch

Friday, August 12, 2016

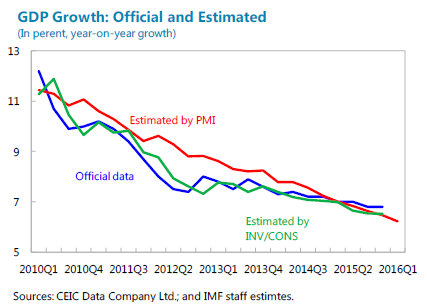

How Reliable is China’s Output Data?

“There is some evidence pointing to possible overstatement of growth recently, but the overstatement is likely moderate and the official national accounts data—while there is much room for improvement—likely provide a broadly reliable picture,” according to an IMF report.

China’s nominal GDP is probably larger than the official estimate. This could reflect flaws in measuring service consumption, including the inability to fully capture the switch from state-owned industrial firms to market-based (and often smaller) service firms. A study by the Rhodium Group, which duplicates the authorities’ statistical methodology, but addresses some key weaknesses, suggests nominal GDP is underestimated by, for example, 13–16 percent in 2008, and some other studies, while using different approaches, show similar results.

But growth may be smoothed since the smallest and most volatile firms may not be adequately captured in the statistical methodology. Indeed, skepticism that growth is overstated has grown recently, arising largely from the more pronounced weakening in some hard indicators compared to official growth data, including consumption of energy, industrial value added, and commodity imports. A few studies indicate that growth is not overstated over a long time horizon, but that the volatility is understated. Some further argue that the official nominal GDP data are reliable, but the weaknesses in deflators cause real growth to be smoothed. For example, the single deflation approach, which deflates input and output using the same deflator, tends to overstate growth when commodity prices decline sharply. But a counterargument is that the dynamism in the service sector is robust and not well reflected in the hard indicators mentioned above. For example, private consumption is buoyant, with retail sales growing by around 10 percent y/y in real terms.

“Underlying” growth may be weaker than officially reported, but only somewhat.

- Correlation. A sudden decline in the correlation between overall growth data and individual hard indicators could signal that the official data might overstate growth. However, looking at 12-month rolling correlations for real GDP growth versus electricity production, cement, crude steel and freight, does not suggest a recent significant decline (though the series are noisy).

- High frequency-based estimates. Out-of-sample estimates of growth from high-frequency PMIs and consumption/investment indicators are about ¼‒ ½ percent lower than official growth data in 2015.

These results, however, are only indicative of possible slower underlying growth. While providing some cross checks, they are not based on comprehensive datasets and cannot substitute for national account statistics. These approaches focus on underlying growth by analyzing variables traditionally shaping economic fundamentals, while actual growth also includes transitory factors not captured (e.g., the current strength of financial services).”

“There is some evidence pointing to possible overstatement of growth recently, but the overstatement is likely moderate and the official national accounts data—while there is much room for improvement—likely provide a broadly reliable picture,” according to an IMF report.

China’s nominal GDP is probably larger than the official estimate. This could reflect flaws in measuring service consumption, including the inability to fully capture the switch from state-owned industrial firms to market-based (and often smaller) service firms.

Posted by at 9:41 AM

Labels: Inclusive Growth

Climate Mitigation Policy in China: The Many Attractions of Carbon or Coal Taxes

“A carbon or coal tax can effectively address domestic China’s environmental challenges,” according to an IMF report. “Given that sectors most dependent on coal and energy are heavy industries associated with the ‘old growth’ model, these taxes will support China’s effort to rebalance its economy towards high value-added services and consumption-led growth. Moreover, by contributing to coordinated efforts from the international community to slow global warming, these taxes will also reduce the negative impacts climate change will have in China, such as higher occurrence of natural disasters to which coastal areas are particularly vulnerable. Although the government is committed to introducing an Emissions Trading System in 2017, this should not preclude the simultaneous introduction of an upstream carbon or coal tax. This could be facilitated by providing some tax rebates for firms required to obtain emissions allowances to ensure all emitters pay the same unit price of carbon. Given the very large domestic benefits from these policies, China can move ahead unilaterally on its pledges for Paris and make itself better off, without waiting for others to act.”

“A carbon or coal tax can effectively address domestic China’s environmental challenges,” according to an IMF report. “Given that sectors most dependent on coal and energy are heavy industries associated with the ‘old growth’ model, these taxes will support China’s effort to rebalance its economy towards high value-added services and consumption-led growth. Moreover, by contributing to coordinated efforts from the international community to slow global warming, these taxes will also reduce the negative impacts climate change will have in China,

Posted by at 9:33 AM

Labels: Energy & Climate Change

Wednesday, August 10, 2016

How Accurate Are Private Sector Fiscal Forecasts? Evidence from the Great Recession

Government fiscal forecasts invoke considerable skepticism: Frankel (2012), for instance, calls them “wishful thinking” and advocates the use of private forecasts as a reality check. This recommendation leads to an obvious question: how good are the private sector’s fiscal forecasts? We assess the quality of forecasts of the government budget balance made by the private sector for nine advanced economies between 1993 and 2013, with a special focus on the Great Recession period. Our main findings can be summarized as follows. First, we show that private sector budget balance forecasts typically display bias towards ‘optimism’ but the extent of the bias differs across countries. Second, we find that budget balance forecasts exhibit ‘information rigidity’; that is, revisions to forecasts tend to be smooth. This tendency proves costly around turning points in the economy, which we illustrate here using the forecast errors made during the Great Recession. To conclude, while it is a good idea to complement government fiscal forecasts with those from the private sector, there are steps that the private sector could also take to improve the quality of its own forecasts.

For details, see my paper published in the 21st Federal Forecasters Conference Proceedings.

Government fiscal forecasts invoke considerable skepticism: Frankel (2012), for instance, calls them “wishful thinking” and advocates the use of private forecasts as a reality check. This recommendation leads to an obvious question: how good are the private sector’s fiscal forecasts? We assess the quality of forecasts of the government budget balance made by the private sector for nine advanced economies between 1993 and 2013, with a special focus on the Great Recession period. Our main findings can be summarized as follows.

Posted by at 5:27 PM

Labels: Forecasting Forum

Subscribe to: Posts