Monday, August 15, 2016

Housing Market in China

The latest IMF’s annual report on China points out the following:

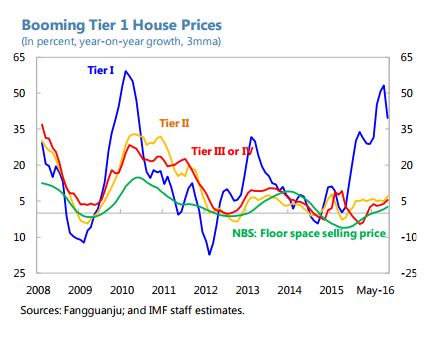

- “China has recently experienced a sequence of booms in various asset prices—property, equity and bonds. This propensity is a symptom of a large stock of savings searching for yield, rising leverage, and a belief that the web of implicit guarantees will limit losses. This distorts the pricing of risk and facilitates bouts of speculative excess. Most recently, Tier-1 cities such as Shenzhen, Shanghai, and Beijing, are seeing large housing price increases as bank lending for home purchases increased strongly.”

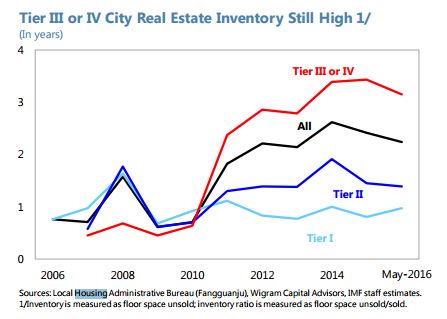

- “Residential investment is reviving again in several parts of the country, even as excess inventory remains high, and region-specific policies could be appropriate. Specifically, tighter macroprudential measures in Tier 1 cities seem warranted (for example reducing loan-to-value ratios on mortgages for second homes). For lower-tier cities, where multi-year excess inventory levels are particularly acute, restricting new starts seems warranted, for example by tightening prudential measures on credit to property developers.”

- “The authorities observed that property prices were beginning to show signs of moderation in Tier 1 cities, while equity prices were more in line with fundamentals after the substantial correction over the last 12 months. They recognized that there were some financial sector risks, but that these were limited and the supervisors were responding proactively.”

Posted by at 10:41 AM

Labels: Global Housing Watch

Subscribe to: Posts