Wednesday, April 4, 2018

Housing Market in Luxembourg: Assessment and Policy Recommendations

From the IMF’s latest report on Luxembourg:

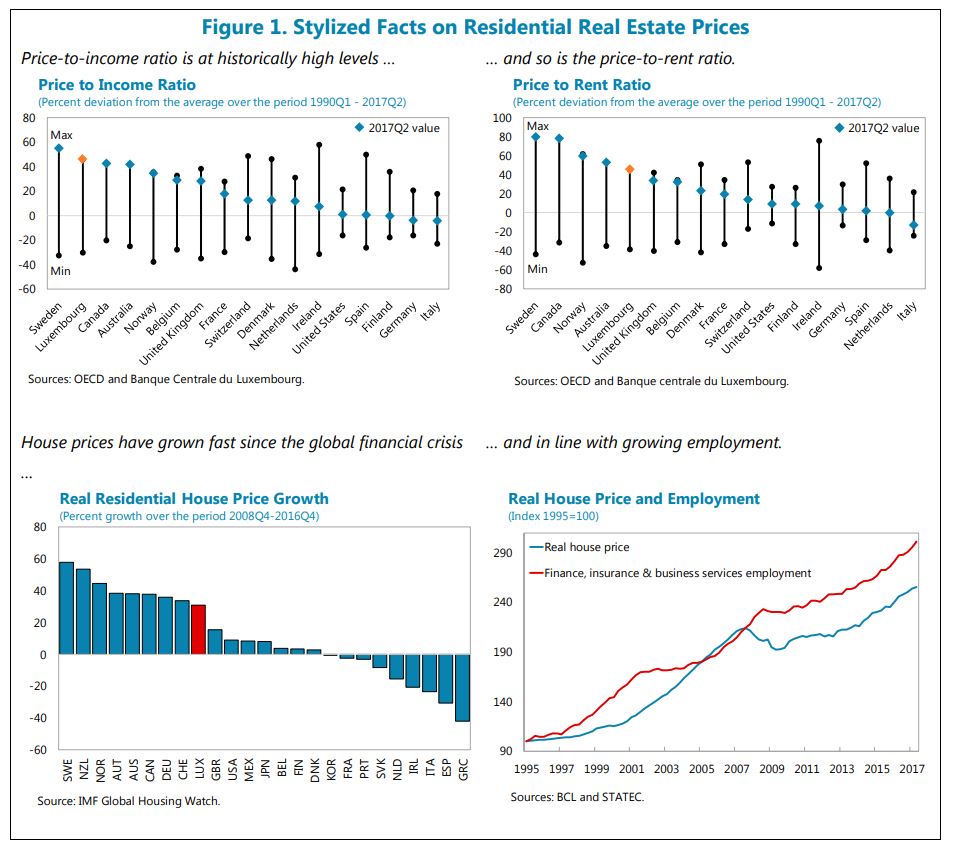

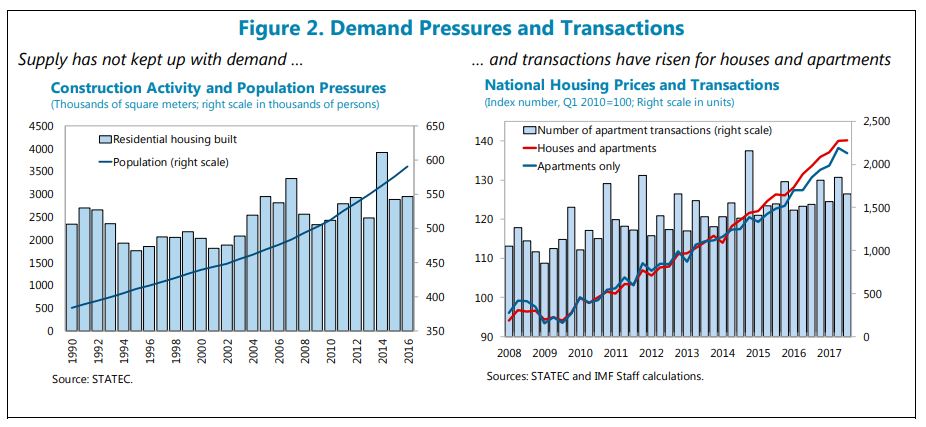

“Demand for housing has exceeded supply for many years. While house prices are in line with fundamentals, they have risen faster than disposable income for years, largely because of structural supply constraints in the context of strong demand, in part reflecting net demographic growth. The dynamics of house prices is also somewhat affected by cyclical factors such as the cost of construction and to some extent the low interest rate environment. Rigid zoning and administrative rules together with land hoarding prevent sufficient construction, while tax incentives and subsidies fuel demand. Reduced affordability has driven up household indebtedness, in particular among younger households.

Risks in the real estate market should continue to be closely monitored, and further actions taken as needed. Recent measures have appropriately built capital buffers in the banking system while discouraging riskier lending. However, household debt is relatively high and limits to debt-service-to-income ratios should be set if house prices continue to outpace disposable incomes. Going forward, the normalization of interest rates could add to the debt service of some households (who borrowed at variable rates) while banks’ margins on their stock of fixed rate mortgages would shrink.

Containing house price pressures and alleviating bottlenecks of housing require a strong effort to expand the stock of housing:

- Excessive red tape in bringing additional land to construction should be pruned, and incentives strengthened. The initiatives of Baulücken for new construction are a step in the right direction;

- Local zoning decisions should be better coordinated with a national spatial development plan and cooperation among municipalities should be encouraged;

- Existing tools to mobilize vacant land and unoccupied dwellings could be strengthened. This includes implementing taxation on vacant lots. In this respect, the initiative of Baulandvertrag goes in the right direction;

- In the PDAT and the municipal implementation, assigning “mixed construction” land in priority to residential real estate would widen the share of land eligible for housing development;

- Tax biases at the municipality level against residential real estate should be reduced further. The reform of the distribution of municipal business taxes among municipalities is a step in the right direction as it reduces incentives favoring commercial over residential real estate zoning decisions. Going forward, policies should increase the share of the ICC redistributed in the equalization fund;

- Increasing property taxes and revising cadastral values would help municipalities increase own resources.

The share of social and affordable housing in total housing could be increased:

- To encourage social housing in the rental segment, public developers in the social sector (FSH, SNCHM, and municipalities) should be gradually steered only towards the development and management of social rentals. This would help clarify management roles and separate more clearly the rental activity from the construction-for-sale business.”

From the IMF’s latest report on Luxembourg:

“Demand for housing has exceeded supply for many years. While house prices are in line with fundamentals, they have risen faster than disposable income for years, largely because of structural supply constraints in the context of strong demand, in part reflecting net demographic growth. The dynamics of house prices is also somewhat affected by cyclical factors such as the cost of construction and to some extent the low interest rate environment.

Posted by at 4:33 PM

Labels: Global Housing Watch

Tuesday, April 3, 2018

What Lies beneath? A Sub-National Look at Okun’s Law in the United States

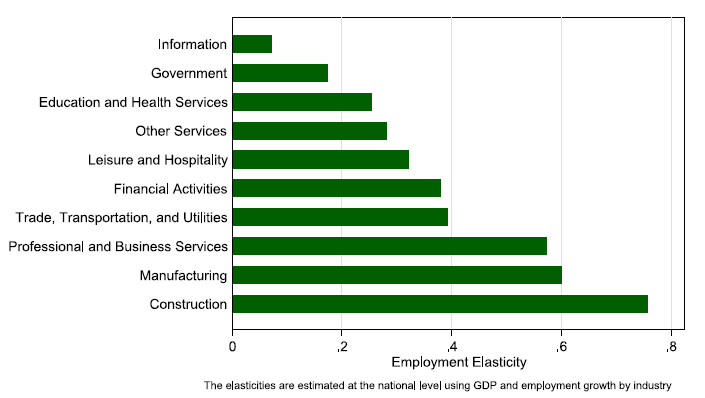

In my new paper with Nathalie Gonzalez Prieto and Saurabh Mishra, “We find that Okun’s Law holds quite well for most U.S. states but the Okun coefficient—the responsiveness of unemployment to output—varies substantially across states. We are able to explain a significant part of this cross-state heterogeneity on the basis of the state’s industrial structure. Our results have implications for the design of state and federal policies and may also be able to explain why Okun’s Lawat the national level has remained quite stable over time despite an enormous shift in the structure of the U.S. economy from manufacturing to services.”

Fig. 3 National-level employment elasticities

Continue reading here.

In my new paper with Nathalie Gonzalez Prieto and Saurabh Mishra, “We find that Okun’s Law holds quite well for most U.S. states but the Okun coefficient—the responsiveness of unemployment to output—varies substantially across states. We are able to explain a significant part of this cross-state heterogeneity on the basis of the state’s industrial structure. Our results have implications for the design of state and federal policies and may also be able to explain why Okun’s Lawat the national level has remained quite stable over time despite an enormous shift in the structure of the U.S.

Posted by at 10:40 AM

Labels: Inclusive Growth

The IMF and Fragile States

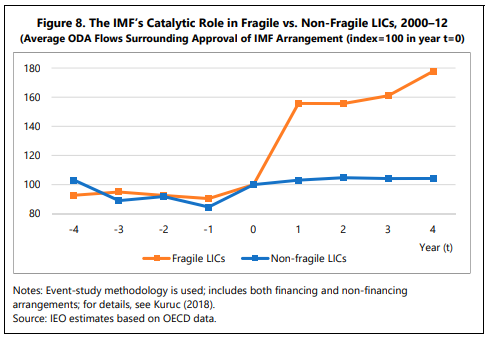

From the Independent Evaluation Office report on the IMF and Fragile States:

Executive Summary

“This evaluation assesses the IMF’s engagement with countries in fragile and conflict-affected situations (FCS). Helping these countries has been deemed an international priority because of their own great needs and the dangerous implications of persistent fragility for regional and global stability. With its crisis response and prevention mandate, the IMF has a key role to play in these international efforts. In practice, its contribution has been subject to considerable debate, and critics have called on the Fund to increase its engagement.”

Key Findings

“The evaluation recognizes the important contributions that the IMF has made in fragile states, including helping to restore macroeconomic stability, build core macroeconomic policy institutions, and catalyze donor support. In these areas, the IMF has provided unique and essential services, playing a critical role in which no other institution can take its place. Though the progress made by many FCS to escape fragility has been disappointingly slow and subject to reversal, it must be recognized that work on fragile states is inherently challenging, given their generally limited capacity, weak governance, and often unstable political and security environment. Moreover, the outcome of any IMF intervention is critically influenced by political, military, and security decisions including by international actors outside the Fund’s control. Against these challenges, the IMF on balance has performed its various roles quite effectively, particularly in years soon after countries first emerged from periods of violence and isolation.”

“Despite this overall positive assessment, the IMF’s approach to fragile member states seems conflicted and its impact falls short of what could be achieved. Even though the IMF has declared in several pronouncements that work on FCS would receive priority, it has not consistently made the hard choices necessary to achieve full impact from its engagement. FCS typically require long-term, patient modes of engagement that do not fit well with the IMF’s standard business model. Efforts have been made in the past to adapt IMF policies and practices to FCS needs, but initiatives have not been sufficiently bold or adequately sustained, leaving questions about the credibility of the Fund’s commitment in this area.”

Continue reading here.

From the Independent Evaluation Office report on the IMF and Fragile States:

Executive Summary

“This evaluation assesses the IMF’s engagement with countries in fragile and conflict-affected situations (FCS). Helping these countries has been deemed an international priority because of their own great needs and the dangerous implications of persistent fragility for regional and global stability. With its crisis response and prevention mandate, the IMF has a key role to play in these international efforts.

Posted by at 9:47 AM

Labels: Inclusive Growth

Saturday, March 31, 2018

Dani Rodrik on Globalization and its Discontents

From Pro-Market:

In an interview with ProMarket, Harvard economist Dani Rodrik explained where globalization went wrong, how trade agreements serve rent-seeking by politically well-connected firms, and why the only solution to the rise of political populism is an economic populism that reimagines the institutions of capitalism.

Q: A recent report by the United Nations Conference on Trade and Development argued that the hyperglobalization of the past 30 years has led to a sharp increase in market concentration, which in turn led to a proliferation of rent-seeking. Do you agree with the assessment that globalization has increased rent-seeking?

I’m not saying that it has increased rent-seeking. I’m agnostic on that. I think it’s changed the relative power of different groups of rent-seekers and that the terrain over which the rent-seeking is taking place is different. I don’t want to make a blanket statement that we’re in a world where rent-seeking has increased. I think it’s always been there. I think what has happened is a combination of changes in our ideas and changes in the financial power and other powers of different groups, and this combination is reflected in the various parts of our global economy.

I think that by fetishizing globalization and exaggerating its benefits and understating its downsides, we have essentially privileged and prioritized a set of powerful interests. The fact that pharmaceutical companies or foreign investors find it so easy to get what they want is in part because of our existing narratives, or existing ideas, about how the world does or should work.

Q: You differentiate between two kinds of populism—political populism, the kind of autocratic populism we see from the likes of Putin in Russia and Erdoğan in Turkey—and economic populism, which you write is “occasionally necessary” and which you seem to suggest as a potential remedy to our current predicament. What is economic populism, and how is it different from political populism?

I think economic populism is a populism that takes aim at the sources of economic inequality and at concentrations of economic power. Today in the US, economic populism would take the form of bringing the financial sector down to size, reducing the influence of Wall Street in political institutions, and having much greater regulation of the financial sector. It would mean taking aim at concentrations of power in high-tech and digital industries. It would mean taking aim at our current pattern of trade agreements, which often privilege particular corporate interests and investors. All of that would be economic populism that tries to reshape the distribution of economic power and tries to reduce the concentration of economic power but does not try to turn the political system into an authoritarian one, does not necessarily concentrate political power or undermine liberal norms of pluralism and tolerance.

See my profile of Dani Rodrik here.

From Pro-Market:

In an interview with ProMarket, Harvard economist Dani Rodrik explained where globalization went wrong, how trade agreements serve rent-seeking by politically well-connected firms, and why the only solution to the rise of political populism is an economic populism that reimagines the institutions of capitalism.

Q: A recent report by the United Nations Conference on Trade and Development argued that the hyperglobalization of the past 30 years has led to a sharp increase in market concentration,

Posted by at 7:55 AM

Labels: Profiles of Economists

Friday, March 30, 2018

Forecasting Forum – March 2018

R package for M4 Forecasting Competition – Hyndsight (Rob Hyndman’s Blog)

2018 & 2019 Economic Outlook for the Top Oil Producing Countries – Focus Economics

Big Data and Economic Nowcasting – No Hesitations (Frank Diebold’s Blog)

The Poorest Countries in the World – Focus Economics

STILL MORE on NN’s and ML – No Hesitations (Frank Diebold’s Blog)

Use and misuse of information in supply chain forecasting of promotion effects – IIF Blog

ML, Forecasting, and Market Design – No Hesitations (Frank Diebold’s Blog)

Emerging Markets 2018 Economic Outlook – Focus Economics

Averaging for Prediction in Econometrics and ML – No Hesitations (Frank Diebold’s Blog)

Economic Goodness-of-Fit – Dave Giles’ Blog

Forecasting global economic growth in 2018 – Brookings

Comparing Interval Forecasts – No Hesitations (Frank Diebold’s Blog)

How do you forecast? Practitioners’ insights needed – IIF Blog

R package for M4 Forecasting Competition – Hyndsight (Rob Hyndman’s Blog)

2018 & 2019 Economic Outlook for the Top Oil Producing Countries – Focus Economics

Big Data and Economic Nowcasting – No Hesitations (Frank Diebold’s Blog)

The Poorest Countries in the World – Focus Economics

STILL MORE on NN’s and ML – No Hesitations (Frank Diebold’s Blog)

Use and misuse of information in supply chain forecasting of promotion effects – IIF Blog

Posted by at 1:26 PM

Labels: Forecasting Forum

Subscribe to: Posts